Simon Property Group (NYSE:SPG) stock is flirting with new 52-week highs. The rally is likely being powered by improving macro conditions and increased confidence in SPG’s prospects following its recent dividend hike streak. The retail property giant has raised its dividend 10 times over the past four years, having sustained a tremendous post-pandemic recovery. Further, Simon Property Group is expected to post record profits this year, which could sustain its momentum. Consequently, I remain bullish on the stock.

Stay Ahead of the Market:

- Discover outperforming stocks and invest smarter with Top Smart Score Stocks

- Filter, analyze, and streamline your search for investment opportunities using Tipranks' Stock Screener

Post-Pandemic Dividend Growth Streak Impresses

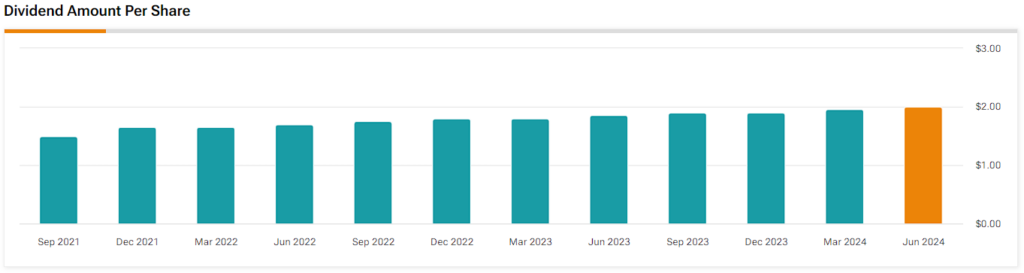

In my view, the most notable catalyst fueling SPG’s current rally is its excellent post-pandemic dividend growth trajectory. The company had to slash its dividend in Q2 2020 due to widespread panic in the retail REIT industry at the onset of the pandemic. The quarterly dividend rate was reduced from $2.10 to $1.30 at the time, and the company did indeed face significant challenges for a couple of years.

However, Simon Property Group’s portfolio has proven to be one of the most resilient in the sector, allowing the company to achieve a swift recovery in its financials, even in the face of rising interest rates. Despite elevated rates currently pressuring the company’s bottom line, as is the case with all of its sector peers, SPG is poised to post record profits this year.

This strong performance has enabled Simon to rapidly reinstate its dividend to pre-pandemic levels. The most recent dividend hike announced alongside its Q1 results was a 2.6% increase to $2.00, bringing the dividend very close to its pre-pandemic level. Interestingly, the current annualized rate of $8.00 implies a solid dividend yield of 5.4%, even with shares rallying recently. Combined with the potential for additional dividend growth, SPG remains a highly compelling dividend pick.

Record Profits Support More Dividend Increases

To assess SPG’s potential for further dividend increases, let’s examine its performance, which, so far, points toward record profits for this year. In Q1, the company recorded total revenues of $1.44 billion, 6.7% higher compared to last year. This was driven by improved occupancy rates and a higher base minimum rent (BMR). Specifically, at the end of March, Simon Property Group’s occupancy was 95.5%, up 110 basis points compared to last year, while its BMR was $57.53, up 3% compared to Q1 2023.

In the meantime, while interest expenses did rise to $230.6 million from $199.4 million last year, the 15.6% increase wasn’t all that bad and proved easily absorbable. The company boosted its bottom line through gains primarily from selling its remaining ownership interest in Authentic Brands Group. Thus, its funds from operations per share (FFO/share, a cash-flow metric used by REITs) still grew by 30% to $3.56.

Based on the company’s first-quarter results and current lease profile, management raised their FY2024 outlook. FFO/share for the full year is now expected to land between $12.75 and $12.90. This implies a year-over-year increase of 2.6% compared to last year and a new FFO/share all-time high. To my point, it also implies significant room for the dividend to grow from its current annualized rate of $8.00.

The Valuation Remains Reasonable

SPG’s recent share price gains have resulted in a valuation expansion. At the midpoint of management’s outlook, SPG stock is trading at a price/FFO of 11.6x. This is somewhat higher than the more depressed single-digit multiples seen in 2022 and 2023 during its earlier post-pandemic recovery phase.

That said, I believe the current valuation remains fair. At their current levels, shares offer a considerable yield, while the dividend has room to grow. Further, with inflation easing faster than expected in May, interest rates are likely to be cut sooner rather than later. This should assist all REIT valuations, including SPG’s, which is likely to see further multiple expansion.

Is SPG Stock a Buy, According to Analysts?

Wall Street’s sentiment on Simon Property remains relatively bullish. The retail real estate company now features a Moderate Buy consensus rating based on six Buys and five Holds assigned in the past three months. At $165.45, the average SPG stock price target implies 11% upside potential.

If you’re unsure which analyst to follow to navigate your decisions in buying and selling SPG stock, check Caitlin Burrows, who represents Goldman Sachs (NYSE:GS). Her track record over a one-year time frame has been excellent, boasting an average return of 33.05% per rating and a success rate of 100%. Click on the image below to learn more.

The Takeaway

Overall, I believe that Simon Property’s impressive post-pandemic recovery, robust dividend growth, and record profit projections position the stock as a compelling investment. Further, despite recent share price gains, the stock’s current valuation remains reasonable, presenting an attractive opportunity for dividend-oriented investors. If anything, the possibility of interest rate cuts in the near term further strengthens its investment case, which is likely to sustain the stock’s rally.