Nvidia (NVDA) is expected to report 84.4% earnings growth when it delivers its Q3 results next week. The company has smashed expectations frequently over the past two years, but earnings season is typically the most volatile period for the stock. While there is potential for more upside if the tech giant continues to surprise, I don’t think it’s wise to buy before the results — it’s like betting. That’s simply my personal opinion despite being bullish on Nvidia over the long run, considering the supportive trends in artificial intelligence (AI) and the first deliveries of Blackwell servers.

Invest with Confidence:

- Follow TipRanks' Top Wall Street Analysts to uncover their success rate and average return.

- Join thousands of data-driven investors – Build your Smart Portfolio for personalized insights.

What are Analysts Expecting of Nvidia?

So, what exactly are analysts forecasting? Well, Nvidia is set to announce its Q3 Fiscal 2025 earnings on November 20, 2024, after market close. Analysts have forecasted EPS of $0.74, with an estimated revenue of $32.95 billion. The company has seen plenty of upward EPS revisions in the last 90 days, with 31 analysts raising estimates compared to 6 lowering them.

According to these forecasts, Nvidia’s projected year-over-year EPS growth is an outstanding 84.4%, reflecting continued strong performance in the AI chip and data center market. The company’s earnings outlook remains positive, with analysts forecasting steady EPS growth through fiscal 2026, albeit at a decelerating rate as the market matures.

Importantly, the recent history tells us to expect an outperformance from NVDA. Its performance has been exceptional in recent quarters, consistently beating earnings estimates. The company’s revenue has shown remarkable year-over-year growth, with triple double-digit increases in the last four quarters. Moreover, Nvidia’s EPS has also consistently exceeded expectations, beating in the last seven quarters. This outperformance is once again attributed to surging demand for AI chips over the past two years.

Robust Growth Justifies NVDA’s Premium Valuation

Unsurprisingly, investors are willing to pay a premium for access to this earnings growth and I’m with them. The forward P/E ratio of 52.3x is significantly higher than the sector median of 25.3x, confirming this substantial premium. However, the price-to-earnings-to-growth (PEG) ratio of 1.47 is more favorable, indicating that Nvidia’s valuation may be justified when considering its high growth rate. This PEG ratio is lower than the sector median of 1.98.

Moreover, while I accept that Nvidia might be trading relatively close to the fair value that it has been, I’d suggest these figures infer that there is room for further share price expansion. Of course, this would be partially dependent on the company continuing to exceed its earning expectations.

Looking at EBITDA, the Santa Clara firm’s forward EV/EBITDA ratio sits at 44.4x, and that’s considerably higher than the sector median of 15.5x. However, this metric is more favorable than the stock’s 5-year average, potentially indicating better relative value despite the high multiple.

Nvidia’s Blackwell Fuels Stock Surge Potential

Nvidia stock is up 2702% over five years, and of course, a lot of AI and data center tailwinds are already priced in. However, that doesn’t mean that supportive trends aren’t being underestimated. I believe there are plenty of things that can take Nvidia stock higher, and Blackwell is the main proponent.

The anticipated first delivery of its Blackwell GPU servers has generated considerable excitement, with industry analysts drawing parallels to the early days of the iPhone and its sales potential. This new platform is expected to drive substantial demand as major cloud providers plan to significantly increase capital expenditures in 2025.

Recent reports indicate that AI server cabinets featuring Blackwell GPUs could be priced between $2 million and $3 million, potentially driving annual revenues exceeding $200 billion. Morgan Stanley (MS) has forecasted Q4 of 2024 Blackwell sales of up to $10 billion.

Nvidia’s Ecosystem Powers Blackwell’s Success

Another reason I’m bullish on Nvidia and Blackwell is the company’s developed ecosystem. The expected success of Blackwell is not only due to its inference capabilities but also Nvidia’s comprehensive approach, which combines hardware, software, and developer tools, creating a strong competitive moat that’s hard for rivals to overcome.

Moreover, collaborations with companies like Tesla (TSLA) and SoftBank highlight the company’s leadership. NVDA CEO Jensen Huang emphasized the rapid deployment capabilities of xAI’s supercomputer cluster, which utilized 100,000 H200 Blackwell GPUs in just 19 days. This reflects both the strong demand for the company’s products and the rapid growth of AI infrastructure across various sectors.

Is Nvidia a Good Stock to Buy Now?

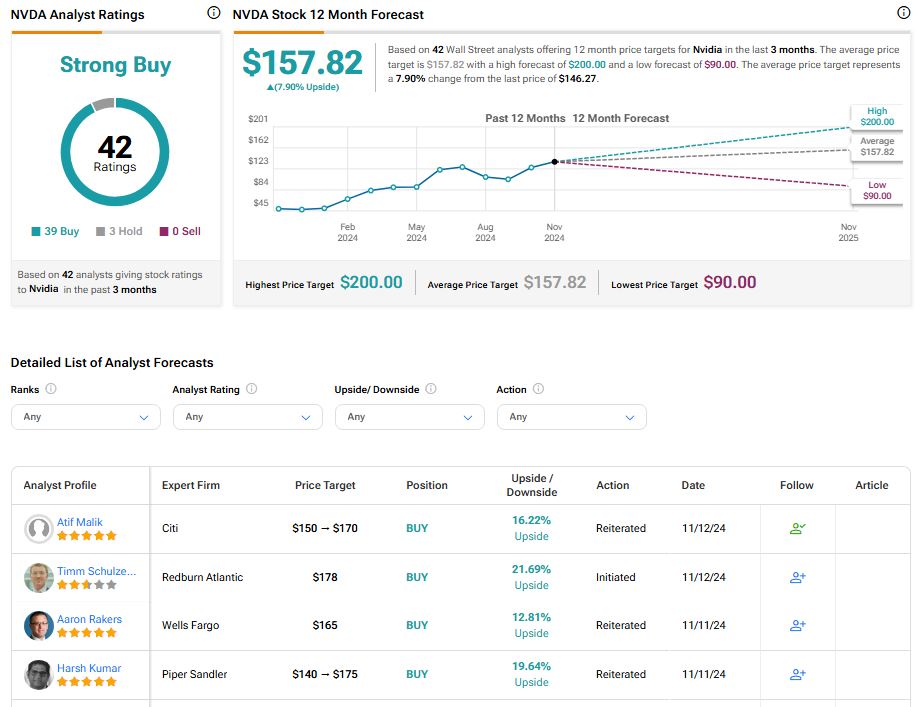

On TipRanks, NVDA comes in as a Strong Buy based on 39 Buys, three Holds, and zero Sell ratings assigned by analysts in the past three months. The average NVDA stock price target is $157.82, implying about 8% upside potential.

The Bottom Line on Nvidia

While Nvidia’s impressive growth and AI-driven momentum make it a strong long-term bet, I don’t think it’s wise to buy it ahead of its Q3 results as earnings season is often a volatile period for any stock.

Despite this caution, I remain bullish on Nvidia’s long-term prospects, especially with the Blackwell GPUs and the continued strength of the AI sector. Also, while the company’s near-term valuation multiples look a little stretched, Nvidia is expected to deliver more groundbreaking earnings growth over the coming years. Additionally, with over 90% of analysts rating the stock as a ‘Buy,’ investor confidence remains high.