SolarEdge Technologies (SEDG) stock declined over 9% in the after-hours trading session on Wednesday. The downside can be attributed to weak second-quarter results due to ongoing softness in the retail solar market.

SEDG provides smart energy solutions, such as solar inverters, power optimizers, and monitoring systems for solar installations.

SEDG: Q2 Highlights

The company reported an adjusted loss of $1.79 per share, against earnings of $2.62 per share in the prior-year quarter. Also, the loss surpassed the consensus estimates of a loss of $1.52 per share. Furthermore, the company’s revenue declined 73.2% year-over-year to $265.4 million but marginally beat the analysts’ expectations of $265.2 million.

SolarEdge’s disappointing performance is due to weak demand for its products and supply chain disruptions during the quarter. The company witnessed a drop of 64% and 80% in shipments of optimizers and inverters, respectively.

For the third quarter, the company expects revenues to be in the range of $260 million to $290 million. Also, adjusted expenses are expected in the range of $111 million to $116 million.

TD Cowen Analyst Remains Bullish

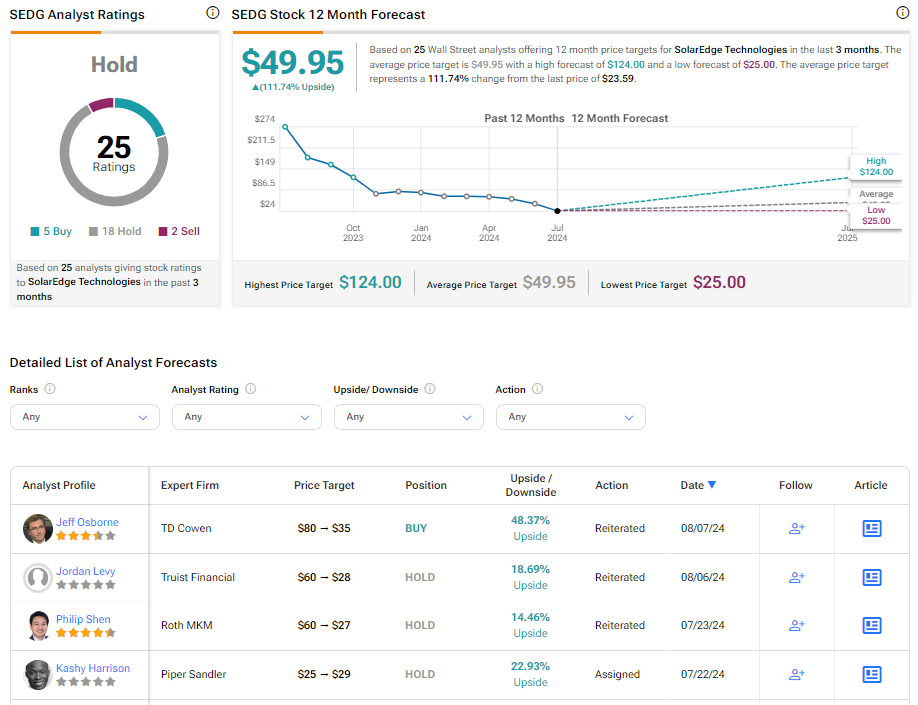

Despite the company’s weak Q2 report, TD Cowen analyst Jeff Osborne reiterated a Buy rating on SolarEdge stock. However, he slashed the price target to $35 (48.4% upside potential) from $80.

Osborne anticipates that channel inventory levels will normalize by the end of Q3, indicating a rise in demand. He also believes that SolarEdge’s emphasis on creating differentiated and cost-effective products may offer a competitive edge.

Importantly, the analyst has an average return of 55.03% and a success rate of 62% on SEDG (to watch Osborne’s track record, click here).

Is SEDG Stock a Good Buy?

On TipRanks, SolarEdge has a Hold consensus rating based on five Buy, 18 Hold, and two Sell ratings. The analysts’ average price target on SEDG stock of $49.95 implies a significant upside potential of 111.74%. Shares of the company have declined by 59% over the past three months.