Sea Limited (SE), a leading global consumer internet company, reported mixed results in its Q2 2024 earnings. Revenue surged 23% year-over-year to $3.8 billion, driven by its e-commerce giant Shopee, alongside contributions from Garena and SeaMoney. However, net income dropped sharply to $79.9 million from $331 million in the same quarter last year. Despite the hit to profits, Sea’s CEO Forrest Li remains confident in the company’s long-term growth trajectory.

Sea Reports Strong Revenue Growth, Despite a Dip in Profits.

Sea Limited’s total GAAP revenue for Q2 2024 hit an impressive $3.8 billion, marking a 23% year-over-year increase. The e-commerce segment, driven by Shopee, played a significant role in this growth, with a 33.7% year-on-year revenue increase, reaching $2.8 billion. Shopee continues to be a major player, especially in Southeast Asia and Taiwan, with gross orders surging by 40.3% year-on-year.

However, it wasn’t all smooth sailing. The company’s net income saw a significant decline, falling from $331 million in Q2 2023 to $79.9 million in Q2 2024. This drop is a notable shift, especially considering the positive momentum Sea experienced in previous quarters.

Shopee’s Sees a Bright Outlook

Shopee’s performance was a highlight in Sea Limited’s report. Forrest Li, Sea’s CEO, expressed optimism about the platform’s future, stating, “With the strong results delivered in the first half and our outlook for the rest of the year, we expect that Shopee will become adjusted EBITDA positive from the third quarter.” This is promising news for investors, as it suggests Shopee is moving towards sustained profitability, especially with its revised GMV growth guidance to mid-20% for the full year 2024.

Garena Maintains Steady Performance

On the digital entertainment front, Garena, the company’s gaming arm, also delivered solid results. Bookings increased by over 20% year-on-year, primarily driven by the continued success of Free Fire. Li proudly mentioned, “Every single day throughout Q2, Free Fire had more than 100 million daily active players.” This reinforces Garena’s position as a key revenue generator for Sea.

Sea Limited Expands Financial Services Growth

SeaMoney, Sea Limited’s digital financial services arm, also showed robust growth. Its GAAP revenue rose by 21.4% year-on-year, reaching $519.3 million. This growth was largely driven by the consumer and SME credit business, with loans outstanding increasing by nearly 40% compared to the same period last year.

SE Reports Decline in Earnings Per Share

When it comes to earnings per share (EPS), Sea reported a basic EPS of $0.14, down from $0.57 in Q2 2023, missing analysts’ consensus estimate of $0.31. While these figures might not be what investors were hoping for, the company’s focus on long-term growth and profitability across its business segments provides a reason for optimism.

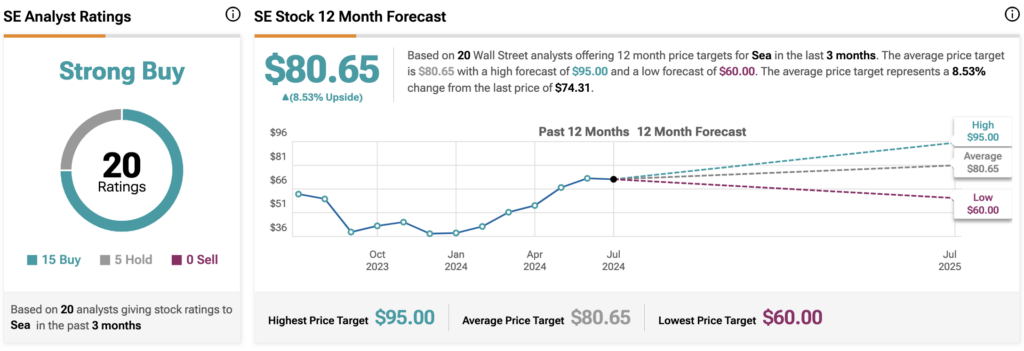

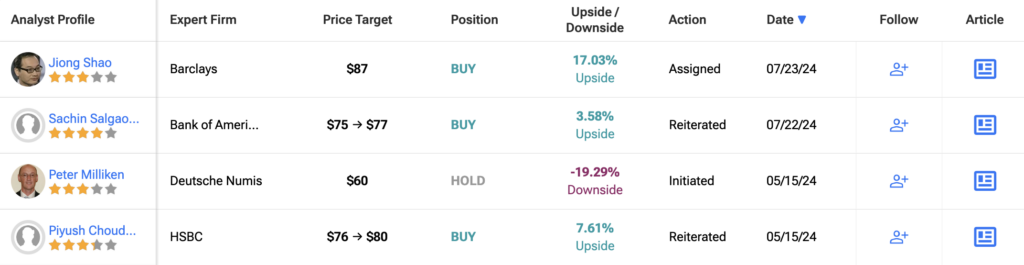

Is SE Ltd a Good Buy?

Analysts remain bullish about SE stock, with a Strong Buy consensus rating based on 15 Buys and five Holds. Over the past year, SE has increased by more than 30%, and the average SE price target of $80.65 implies an upside potential of 8.5% from current levels.