Scorpio Tankers (NYSE:STNG) stock recently slipped on reports that a peace deal for the Israel-Hamas conflict was close. While the latest proposal has fallen through, both parties appear more willing to come to the negotiation table than they had been. The conflict and associated disruption in the Red Sea have pushed shipping rates sky-high, and a cessation of hostilities will likely see leasing rates fall.

However, I remain bullish on Scorpio Tankers. That’s because the conflict in the Middle East isn’t the only supportive trend positively impacting the business. Let’s explore.

Scorpio Tankers and Middle East Conflict

Israel’s war on Hamas and the subsequent attacks on vessels transiting the Bab-el-Mandeb Strait by Houthi forces have pushed leasing rates (time charter equivalent — TCE rates) upwards, but not universally.

Scorpio’s Q1-2024 report highlighted that LR2 (long-range oil tankers) rates rose considerably and showed higher volatility since the start of hostilities. Management highlighted that attacks by Houthi forces had reduced Red Sea traffic by 75% and increased volumes around the Cape of Good Hope by 400%. As this adds up to 70% to a journey between Asia and Europe, it’s perhaps understandable that LR2s and their long-term capabilities are in high demand.

The TCE rate for LR2s was $50,663 in Q1 2024, up from $43,292 a year earlier. Meanwhile, the TCE for MR (medium-range) tankers was almost flat over 12 months, and Handymax tankers — the smallest of the fleet — were down year-over-year.

Scorpio Tankers Has More Tailwinds

Analysts have been sounding alarms about persistent shortages in the oil and refined product shipping sector for some time. The industry faces a severe shortfall, with only two supertankers expected to come online this year. That’s the fewest in nearly four decades and is 90% below the yearly average since the millennium. These limited additions are too few to address the increasing demand, especially with additional disruptions to global supply.

A key factor contributing to these shortages is the time required to build new tankers. These are behemoths of the sea and can’t be built overnight. Constructing a supertanker typically takes several years, from initial design to the first voyage. This timeline has been further stretched due to the pandemic, which saw many shipyards shut down or operate at reduced capacity. As a result of this low replenishment, the global fleet is the oldest it’s been in modern history.

Moreover, the global realignment of trade flows, heavily influenced by Russia’s ongoing war in Ukraine, has disrupted traditional supply routes. The U.S. and Europe have closed 1.9 million barrels per day of refining capacity, with another one million barrels on the cards. The overall impact is that refined products are further away from their end markets than they once were. As such, tanker vessels are having to travel further to reach their destinations.

The Middle East conflict was an unforeseen factor that has driven leasing rates higher and exacerbated existing shortages in the industry, but it’s not a long-term supportive trend. Instead, it may be wise to see it as a windfall, with these bumper revenues contributing to Scorpio’s debt reduction and fleet optimization.

Scorpio Is In a Prime Position to Prosper

So, where does this leave Scorpio? Well, it’s in a prime position to prosper over the long run, with supply shortages likely to last a few more years at least. It has a sizeable and, importantly, young fleet, allowing it to take on prime contracts with big trading houses and refiners.

On 11 June, the company announced the sale of five MR product tankers (four 2012-built and one 2013-built), which will take place in Q2 and Q3. After the sale, all of the firm’s 100+ vessels will have been built after 2014.

Moreover, the company’s balance sheet looks incredibly strong. It recently paid down $223.6 million of debt early, reducing the breakeven point by $3,500 per vessel per day. The company said during its Q1 earnings call that it was looking to bring the breakeven point down, aiming for $12,500 per day. As management highlighted, this would be one of the lowest in the industry despite Scorpio having one of the most modern fleets.

Capping things off, the stock is trading at just 6.3x forward earnings. Analysts expect a moderate fall in earnings in 2025, but with limited debt and a modern fleet, I can’t think of a better-positioned tanker stock to prosper in the long run.

Is Scorpio Tankers Stock a Buy, According to Analysts?

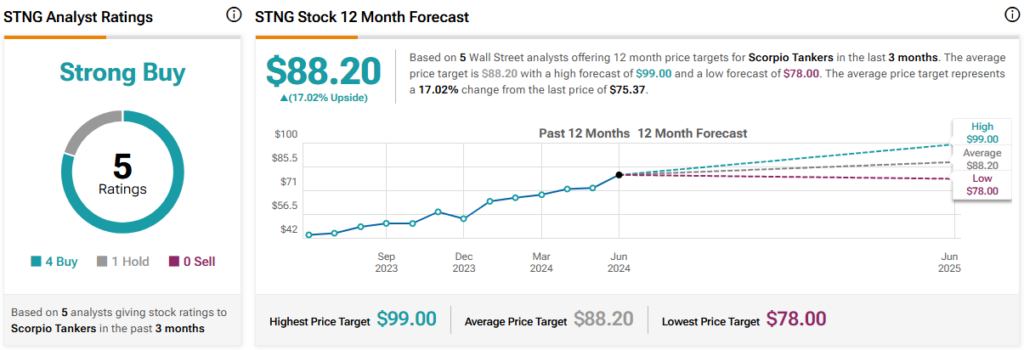

On TipRanks, STNG comes in as a Strong Buy based on four Buys, one Hold, and no Sell ratings assigned by analysts in the past three months. The average Scorpio Tankers stock price target is $88.20, implying 17% upside potential.

The Bottom Line on Scorpio Tankers

Scorpio Tankers boasts a strong balance sheet and a modern fleet and is likely to continue benefiting from tight supply throughout the medium term. I believe it’s one of the best businesses out there, and I remain bullish regardless of the events in the Middle East.