Royal Dutch Shell has agreed to buy ubitricity, the UK’s largest electric vehicle (EV) charging network provider, as the oil giant seeks to switch to lower-carbon transport.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

Financial terms of the transaction weren’t disclosed. For Shell (RDS.A), the acquisition is part of its expansion into the fast-growing on-street EV charging market, the company stated. Following the closure of the deal, which is expected later this year, pending regulatory approval, ubitricity would become a wholly owned subsidiary of Shell.

Founded in Berlin, ubitricity is the UK’s largest public EV charging network, with over 2,700 charge points and a 13% market share. The company has also emerging public charge points in Germany and France and has installed over 1,500 private charge points for fleet customers within Europe. ubitricity cooperates with local authorities to integrate EV charging into street infrastructure such as lamp posts and bollards, for convenient and affordable use.

“Working with local authorities, we want to support the growing number of Shell customers who want to switch to an EV by making it as convenient as possible for them,” Shell Global Mobility’s István Kapitány commented. “On-street options such as the lamp post charging offered by ubitricity will be key for those who live and work in cities or have limited access to off-street parking. Whether at home, at work or on-the-go, we want to provide our customers EV charging options so they can charge up no matter where they are.”

Shell already has over 1,000 ultra-fast and fast charging points at about 430 of its retail sites in addition to worldwide access to over 185,000 third party EV charging points located at forecourts and motorway service stations. Furthermore, the oil giant has a target to become a net-zero emissions energy business by 2050, or sooner.

Meanwhile, Shell shares have gained 58% over the past three months. However, the stock has lost around 30% in value over the past year as oil demand declined and energy prices slumped during the coronavirus pandemic. (See RDS.A stock analysis on TipRanks)

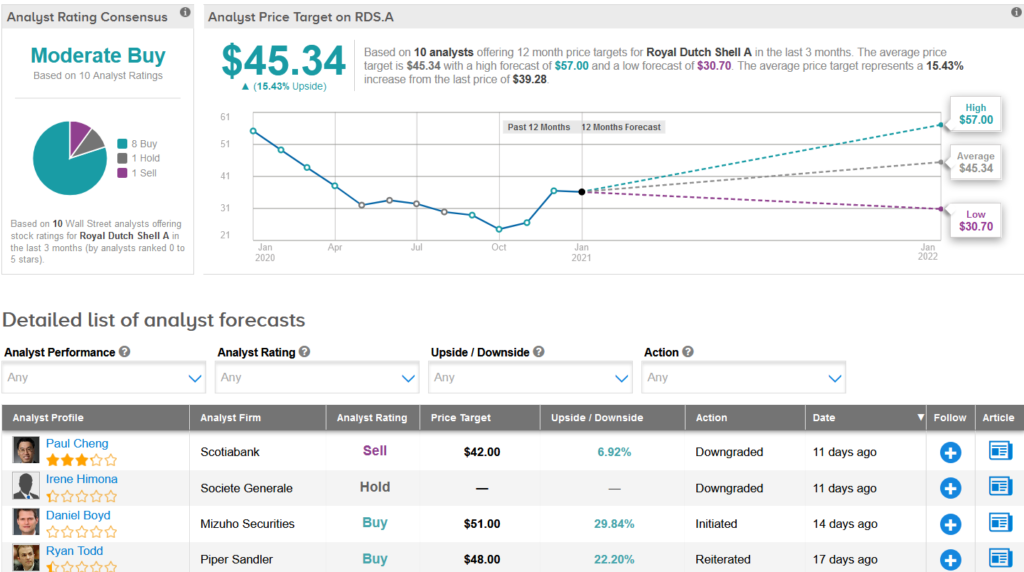

Following the recent share rally, Scotiabank analyst Paul Cheng this month cut the stock’s rating to Sell from Buy and lowered the price target to $42 from $45, as its valuation compared to peers is “no longer as attractive.”

Cheng sees downside risk from a potentially poor quarterly result given the stock’s “previous dramatic outperformance could trigger some mean reversion.”

In the run-up to Shell’s analyst day in February, the analyst believes that the company will be faced with high expectations.

Overall, Wall Street analysts are cautiously optimistic on the stock. The Moderate Buy analyst consensus shows 8 Buys, 1 Hold and 1 Sell. The average price target of $45.34 implies upside potential of about 15% over the next 12 months.

Related News:

Union Pacific Slips 5% On Weak 4Q Freight Revenues

Seagate Tops 2Q Estimates, 3Q Outlook Disappoints

IBM’s 4Q Revenues Of $20.4B Disappoint; Shares Fall 7.3% After Hours