Rocket Lab USA (RKLB) has soared 473% over the past year, fueled by strong revenue growth exceeding 50% in the last three quarters. I remain bullish despite its pricey valuation, significantly buoyed by future growth expectations. Rocket Lab has emerged as an important player in the commercial space sector through its Electron small-satellite launch vehicles and end-to-end space systems solutions. The company’s financial trajectory is undoubtedly impressive and demonstrates accelerating momentum.

RKLB is emerging as a serious contender in a rapidly expanding industry. While execution risks exist, the company’s market offering and timing have endowed it with sky-high potential that, despite the naysayers, justifies the hype.

Rocket Lab Revenue Signals Start of Space Boom

First things first, RKLB has added torque to its market performance in recent years. The space company’s quarterly revenues surged from $51.8 million in Q4 2022 to $104.8 million by Q3 2024, a 102% increase in two years. This growth reflects climbing demand for small-satellite deployment, driven by applications ranging from Earth observation to communications constellations. Rocket Lab executed 56 launches as of 2024.

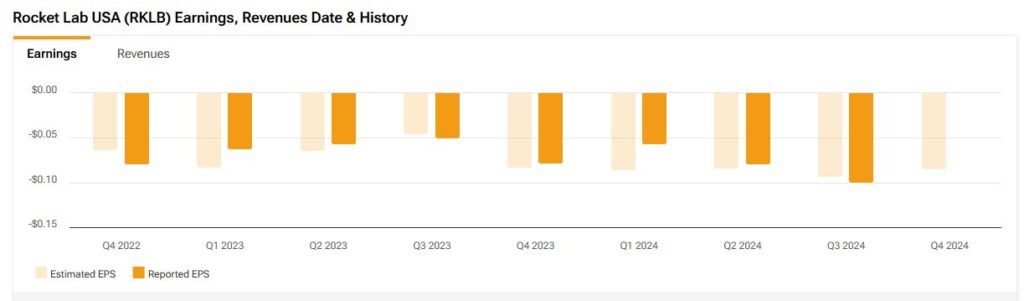

The revenue acceleration – evidenced by three consecutive quarters of >54% YoY growth in 2024 – reflects the company’s broader momentum and strategic expansions into spacecraft manufacturing and components. Rocket Lab now supports over 1,700 missions globally, supplying critical systems for projects like the James Webb Space Telescope while developing its reusable Neutron rocket for larger payloads. Though still unprofitable (-$188.3 million net income), the company’s consistent revenue beats (5 of 15 quarters) and impressive vertically integrated business — from launch pads to satellite radios — position it as a bellwether for the trillion-dollar space economy.

This performance mirrors broader industry shifts, where falling launch costs enable new entrants across the defense, climate monitoring, and broadband sectors. With plans to reuse Electron boosters and expand U.S. launch sites, Rocket Lab’s operational scale and technical milestones suggest the space sector is transitioning from experimental projects to industrialized infrastructure—a foundational shift akin to early automotive or aviation booms.

Rocket Lab’s Trumpian Tailwinds

My bullishness has been reinforced by policy shifts within the Trump Administration that prioritize private sector innovation and reduced regulatory barriers. While Elon Musk’s close alliance with President Trump could skew immediate government support toward SpaceX, the broader industry tailwinds remain favorable for competitors like Rocket Lab.

Trump’s emphasis on commercial space partnerships and streamlined bureaucracy could catalyze growth across the sector. The administration’s push to pivot NASA toward a Mars-first agenda and potential cuts to legacy programs like the Space Launch System (SLS) accelerates opportunities for agile firms specializing in satellite deployment and niche launch services.

While Rocket Lab’s expertise in smallsat launches positions it to capitalize on rising demand for near-Earth missions, it has also been very vocal about its capabilities to undertake Mars missions. The company believes that it has the best solution for returning rock and dust samples collected on the red planet by NASA over the past four years.

Increasingly Competitive in Cost-Sensitive Market

Rocket Lab’s competitive trajectory in the commercial space sector appears to be accelerating with the impending debut of its Neutron rocket, a medium-lift vehicle poised to challenge SpaceX’s Falcon 9 dominance. Targeting its first launch in mid-2025 and commercial missions by 2026, Neutron combines partial reusability, a lightweight carbon-composite airframe, and the methane-fueled Archimedes engine to slash costs while boosting reliability.

CEO Peter Beck’s strategy has highlighted balancing the market against SpaceX’s Falcon 9, particularly for customers seeking alternatives to SpaceX’s Starlink ecosystem. While Neutron’s payload capacity trails Falcon 9’s 22,800 kg to LEO, its projected $60-90 million launch cost undercuts SpaceX’s pricing, appealing to budget-conscious clients. Rocket Lab has already secured its first Neutron customer for 2026 launches, with plans to scale from three missions in 2026 to seven annually thereafter.

Moreover, as SpaceX focuses on deep-space ambitions, Rocket Lab’s niche in responsive, small-to-medium payloads and mega-constellation support could carve a durable market foothold, mainly as global demand for flexible launch solutions grows.

Rocket Lab Valuation Suggests Undervalued Conditions

Valuation data doesn’t immediately reflect an undervalued stock. At 32.3x forward sales, the stock trades at a 1,950% premium to the industrial sector. On a TTM basis, the price-to-sales (P/S) ratio of 37.5x is also a 175% premium to the company’s five-year average. Clearly, these figures don’t scream ‘Buy’.

However, the medium-term picture is much more attractive. On a P/S basis, Rocket Lab’s valuation becomes increasingly compelling as we look further into the future. The company is projected to experience substantial revenue growth over the next several years, with analysts forecasting a significant expansion in sales.

For the fiscal year ending December 2024, Rocket Lab is expected to generate revenue of $434.3 million, representing a robust 77.6% year-over-year growth. This impressive growth trajectory is anticipated to continue, with revenue estimates reaching $603.7 million in 2025, $925.7 million in 2026, and crossing the billion-dollar mark to hit $1.25 billion by 2027.

As revenue scales, the forward price-to-sales (P/S) ratio is expected to contract significantly. From a relatively high 32.3x for fiscal year 2024, it’s projected to decrease to 23.2x in 2025, 15.13x in 2026, and further down to 11.16x by 2027.

The earnings picture also shows promising improvements. While Rocket Lab is currently operating at a loss, with estimated earnings per share (EPS) of—$0.26 for fiscal year 2024, the company is projected to reach profitability within the forecasting period. It’s currently trading at 325.6x projected earnings for 2026 and 98x projected earnings for 2027.

Is Rocket Lab (RKLB) a Buy or Sell?

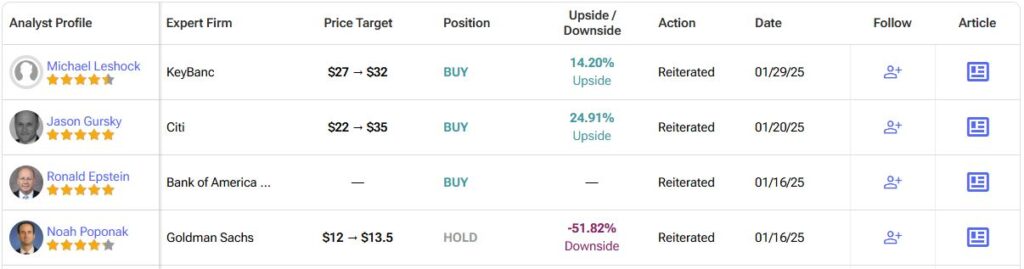

On Wall Street, RKLB stock carries a Moderate Buy consensus rating based on six Buy, three Hold, zero Sell ratings over the past three months. RKLB’s average price target of $26.31 per share implies approximately 6% downside potential over the next twelve months.

RKLB Powerhouse on Launch Pad for Space Disruption

I’m optimistic about Rocket Lab due to its strong revenue growth, expanding launch capabilities, and the anticipated debut of its Neutron rocket. While its valuation is high, the company’s projected revenue growth and improving profitability make for a compelling long-term investment. Favorable industry trends, including supportive policy shifts, further strengthen its outlook. With a growing market share and a clear path to profitability, Rocket Lab is positioning itself as a major force in the rapidly evolving commercial space industry.