As geopolitical tensions rise, defense spending is increasing globally, leading to growth opportunities for companies like Moog (MOG.A), a designer, manufacturer, and integrator of precision control components and systems. Moog’s high-performance systems are integral to military and commercial aircraft, satellites, space vehicles, and more. Recent successes, such as the Certification-2 Flight of the United Launch Alliance Vulcan Rocket and a $100 million subcontract for a liquid chemical propulsion system, highlight the company’s prowess.

Moreover, Moog’s stock is up 55% year-to-date, and consistent financial performance, including top-and-bottom-line beats in Q4 2024 and a year-over-year net sales increase of 9%, demonstrates its strong market positioning and potential for sustained growth in 2025. It is a solid option for investors interested in Aerospace & Defense industry exposure.

Moog Growing Sales While Trimming Costs

Moog is a company that specializes in precision control components and systems design, manufacturing, and integration. It caters to aerospace, defense, and industrial markets in the United States and internationally. Moog’s products and services range from flight and avionic controls, missile and defense system controls, industrial components and systems for use in injection and blow molding machinery, metal forming presses, and heavy industry steel and aluminum production. It also provides components for medical equipment and oil and gas exploration.

The company adopted an 80/20 strategy, and from FY ’22 to FY ’24, achieved a nearly 20% increase in sales while keeping headcount rises to 6% and decreasing factory space by over 10%. The company’s management anticipates further financial and operational enhancements in FY ’25 through ongoing simplification efforts. Under the strategy, an independent voice of customer analysis was completed, involving 120 in-depth interviews, giving the company valuable insights into themes, customer experiences, and net promoter scores needed to help drive further improvements and fortify relationships.

The successful Certification-2 Flight of the Vulcan Rocket by the United Launch Alliance has strengthened the company’s position as a leader in the industry. This flight utilized thrust vector controls provided by Moog, showcasing the advanced technology behind the rocket’s performance. Additionally, its space business has achieved a notable feat by securing a $100 million subcontract to design and produce a liquid chemical propulsion system for a specialized defense application with substantial production potential.

Meanwhile, the ground-based defense business has made significant headway in various U.S. and international pursuits, including securing additional orders for RCH 155 Howitzer, thereby increasing bookings to over $40 million on this program alone. The rise in European defense expenditure signifies promising future demand for this and other platforms.

Moog’s Recent Financial Results

The company recently announced results for Q4 2024. Net sales of $917 million, representing a 5% rise from Q4 2023 while beating analysts’ expectations by $34.65 million. The twelve-month backlog also grew by 3%, reaching a record $2.5 billion. Key contributors to this growth included the Military Aircraft and Space and Defense sectors, with a 17% and 9% increase in sales, respectively. Additional factors positively influenced operating margins in these sectors, including reduced research costs, an improved sales mix in Military Aircraft, and strong European defense demand in Space and Defense.

On the other hand, commercial aircraft and industrial segments recorded declining operating margins due to the absence of benefits from the previous year and increased charges related to simplification initiatives. Despite a 1% decrease in operating margin over the same period, the adjusted operating margin remained steady. The adjusted net earnings per share (EPS) of $2.16 beat consensus expectations by $0.39 while registering a 3% rise year-over-year.

Moog announced a quarterly dividend of $0.28 per share, representing a dividend yield of 0.57%, for both Class A and Class B stocks, payable on December 6, 2024, to shareholders on record as of November 21, 2024.

Following the third quarter’s positive report, MOG.A’s management has issued financial guidance for 2025. Net sales are projected at $3.7 billion, marking an increase from the previous year’s $3.609 billion. Operating margin is expected to expand to 13.0% compared to 11.0% in FY 2024, while the adjusted operating margin remains consistent at 13.0%. An impressive rise is forecasted for adjusted diluted net earnings per share at $7.80 to $8.20. Furthermore, free cash flow conversion is projected to improve significantly from 8% to between 50% and 75%.

Is MOG.A Stock a Buy?

The stock has increased upward by over 188% in the past three years. It trades at the high end of its 52-week price range of $126.65 – $226.95 and shows ongoing positive price momentum as it trades above the 20-day (198.22) and 50-day (195.11) moving averages. With a P/S ratio of 2.03x, the stock looks roughly in line with the Aerospace & Defense industry average of 2.2x.

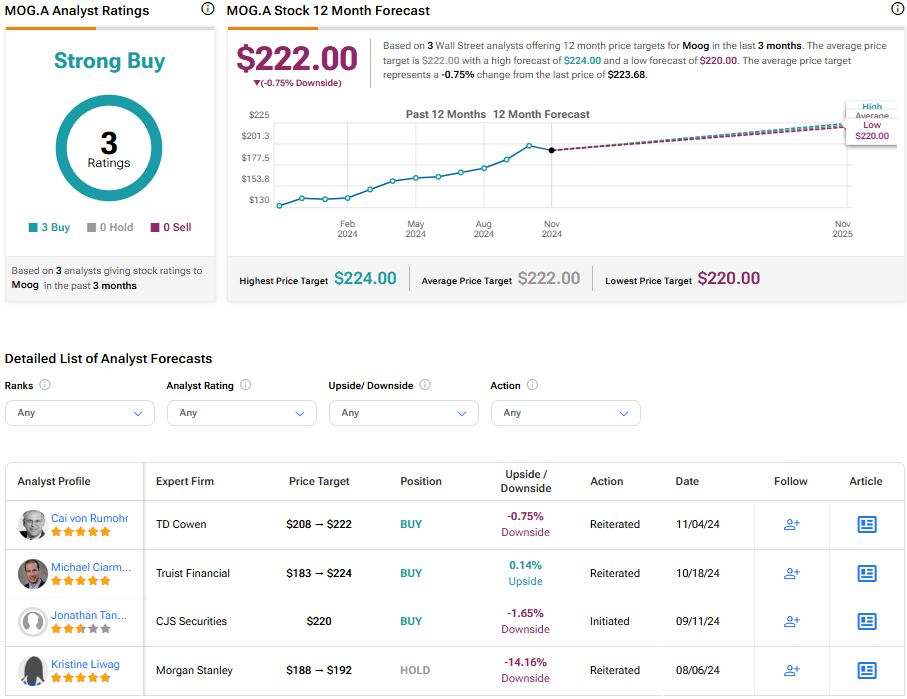

Analysts following the company have been bullish on MOG.A stock. Based on three analysts’ recent recommendations, Moog is rated a Strong Buy overall. The average price target for MOG. A stock is $222.00, representing a potential downside of -0.75%.

See more MOG.A analyst ratings

Final Thoughts on Moog

Moog is well-positioned to capitalize on the escalation of global defense spending. Moog continues to streamline operations, utilizing an 80/20 strategy that, over three financial years, led to a nearly 20% increase in sales. Growing sales have helped drive the stock’s extended uptrend, and the potential for continued growth in the coming year suggests more of the same. With the stock maintaining a strong upward trajectory, it appears to be an attractive investment option.