The S&P 500 wrapped up the first full week of 2025 on a sour note, as December’s labor market data surprised to the upside. U.S. employers added 256,000 jobs last month, significantly outpacing economists’ forecast of 155,000. Meanwhile, the unemployment rate dropped to 4.1%, better than the anticipated 4.2%.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

This robust jobs report underscores the continued strength of the U.S. labor market and the broader economy. However, while this resilience is encouraging, it also raises concerns that the Federal Reserve may adopt a more cautious approach to interest rate cuts this year due to persistent inflationary pressures.

Looking ahead, Larry Adam, Chief Investment Officer at Raymond James, has taken a deep dive into current conditions, examining both the headwinds and tailwinds, and lays out a case for the bulls.

“For the second year in a row, equity markets demonstrated powerful though uneven growth and the U.S. economy remained resilient, despite some dents in the armor. The corporate earnings outlook remains healthy, and while still above target levels, inflation has declined – even if in fits and starts. There are clearly perceivable risks – inflation, consumer spending, investor confidence, international trade – but the outlook for 2025 is positive,” Adam opined.

Against this backdrop, Raymond James stock analysts have spotlighted two small-cap stocks with the potential to skyrocket by as much as 930% in the coming year.

Using the TipRanks database, we’ve looked at the big-picture view on both of these picks, and it seems the rest of the Street agrees with the Raymond James take – both are rated Strong Buys by the analyst consensus. Let’s dive into what makes these hidden gems stand out.

Black Diamond Therapeutics (BDTX)

Heading Raymond James’ picks is Black Diamond Therapeutics, a biopharmaceutical company operating at the clinical stage and taking a novel precision oncology approach to developing oncological treatments. While most cancer drugs target specific mutations that cause or are found in tumors, Black Diamond targets families of oncogenic mutations through its MasterKey approach. This strategy has the potential to broaden the patient base and develop drug candidates with wide applications.

At the core of this innovation is Black Diamond’s flagship drug candidate, BDTX-1535, a brain-penetrant MasterKey inhibitor targeting the epidermal growth factor receptor (EGFR). Currently undergoing human clinical trials, BDTX-1535 is being developed for three key indications: second- and third-line non-small cell lung cancer (2L/3L NSCLC), first-line NSCLC, and glioblastoma multiforme (GBM).

In its 2L/3L NSCLC trial, the company delivered positive initial Phase 2 results in September of last year. The data was based on two patient cohorts; one with relapsed/refractory patients harboring non-classical EGFR mutations, and the other with C797S resistance mutations. Across both groups, BDTX-1535 demonstrated robust anti-tumor activity. The company anticipates providing a clinical update and obtaining regulatory feedback in the first quarter of 2025.

Black Diamond is also testing BDTX-1535 as a first-line therapy for NSCLC patients with non-classical EGFR mutations. Initial results from this ongoing trial are expected in the first quarter of 2025, and the company is optimistic that the encouraging activity observed in recurrent settings will translate into significant clinical benefits for newly diagnosed patients.

The potential doesn’t end there. Black Diamond is exploring the potential of BDTX-1535 in battling glioblastoma (GBM), one of the most aggressive brain cancers. Phase 1 data, presented last June, came from a dose-escalation trial in recurrent GBM patients and revealed promising signs. The drug not only demonstrated a strong safety and tolerability profile but also achieved significant anti-tumor activity. The drug was able to pass through the blood/brain barrier, and reached clinically meaningful levels in brain tumor tissues.

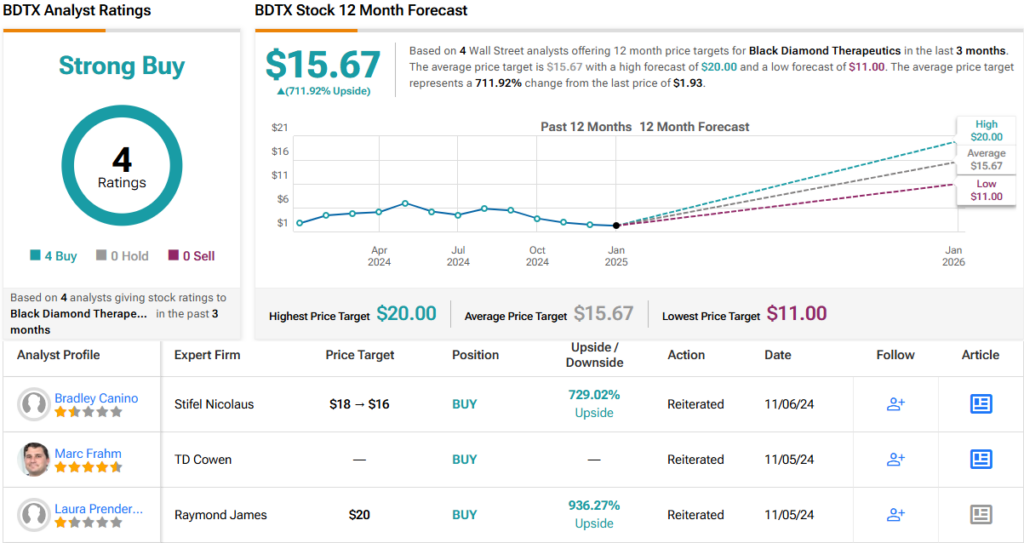

Considering the potential of BDTX-1535, the upcoming catalysts, and the company’s current share price of $1.93, Raymond James analyst Laura Prendergast views BDTX stock as deeply undervalued.

“We remain highly optimistic for 1Q25 clinical updates of BDTX-1535 in EGFRm NSCLC (2/3L updated data and first 1L data in patients with non-classical EGFR mutations)… [We] maintain our belief that numerous features of BDTX-1535 in NSCLC are being underappreciated by investors… We model BDTX-1535 hitting blockbuster status in FY31 and global peak sales of ~$1.8B in FY35. Based on our projections BDTX is significantly undervalued versus its smid-cap biotech peer group,” Prendergast opined.

Just how undervalued? Prendergast rates BDTX an Outperform (i.e., Buy), with a $20 price target implying a substantial one-year upside potential of ~930%. (To watch Prendergast’s track record, click here)

Overall, it’s clear that Wall Street agrees with Prendergast’s assessment. BDTX stock has 4 recent analyst reviews on record, all of which rate it as a Buy, resulting in a unanimous Strong Buy consensus rating. Adding to the optimism, the average price target of $15.67 implies a ~712% upside potential. (See BDTX stock forecast)

INmune Bio (INMB)

Next up is INmune Bio, a clinical-stage biotech company that adopts an innovative approach to drug development by leveraging the patient’s innate immune system to, as the company describes it, ‘fight disease and help the body heal itself.’ INmune focuses on prioritizing patient benefits and aligning the drug mechanism of action with the underlying biological metrics of the target patient population.

Following this approach, INmune has developed a clinical trial pipeline featuring XPro, the company’s leading drug candidate. XPro represents the next generation of precision-targeted therapeutic agents, designed to neutralize tumor necrosis factor (TNF), a driver of innate immune dysfunction and chronic inflammation. Importantly, the drug does not interfere with the normal functions of TNF, which are essential for tissue repair. This specificity enhances both the drug’s effectiveness and safety.

Currently, XPro is being studied as a treatment for Alzheimer’s disease, with enrollment in the Phase 2 clinical trial completed last November. The trial, dubbed AD02, is a global, blinded, randomized study involving 208 patients. The study focuses on patients with early Alzheimer’s as well as biomarkers of elevated neuroinflammation. The drug candidate targets glial cells, key drivers of neuroinflammation in the brain, aiming to reduce neurodegeneration and demyelination while improving synaptic function and remyelination. The study’s primary endpoint is an improvement in baseline cognitive function after 24 weeks of treatment. Topline results from this study are expected during 2Q25.

Meanwhile, XPro is also stepping into the challenging field of treatment-resistant depression. INmune is leading a Phase 2 NIH-backed trial involving 90 participants with inflammatory biomarkers. Over six weeks, patients will receive either XPro or a placebo as researchers track changes in brain activity using functional MRI, focusing on pathways linked to depression and inflammation.

XPro may take center stage as INmune’s most advanced program, but it’s not the company’s only asset. INKmune, an innovative therapy targeting metastatic castrate-resistant prostate cancer, is showing significant potential. In the ongoing Phase I/II trial, it has delivered strong safety results and increased NK-cell activity in the first dosing cohort. With Phase II enrollment projected to conclude by Q2 2025, the program continues to progress.

The optimism surrounding INmune’s Alzheimer’s program, in particular, has captured the attention of Raymond James analyst Gary Nachman, who writes: “With enrollment of the XPro Ph2 in early Alzheimer’s (AD) complete, key focus is on the topline data expected in 2Q25. Management remains optimistic in a positive outcome given several elements of the Ph2 design (inflammatory biomarker enrichment, EMACC primary endpoint, 24-week duration) and quality data collection that should help de-risk the trial. Positive Ph2 data in early AD would be the key value creating catalyst, validating INMB’s novel approach targeting neuroinflammation in AD and unlocking potential partnership opportunities for a larger Ph3 program.”

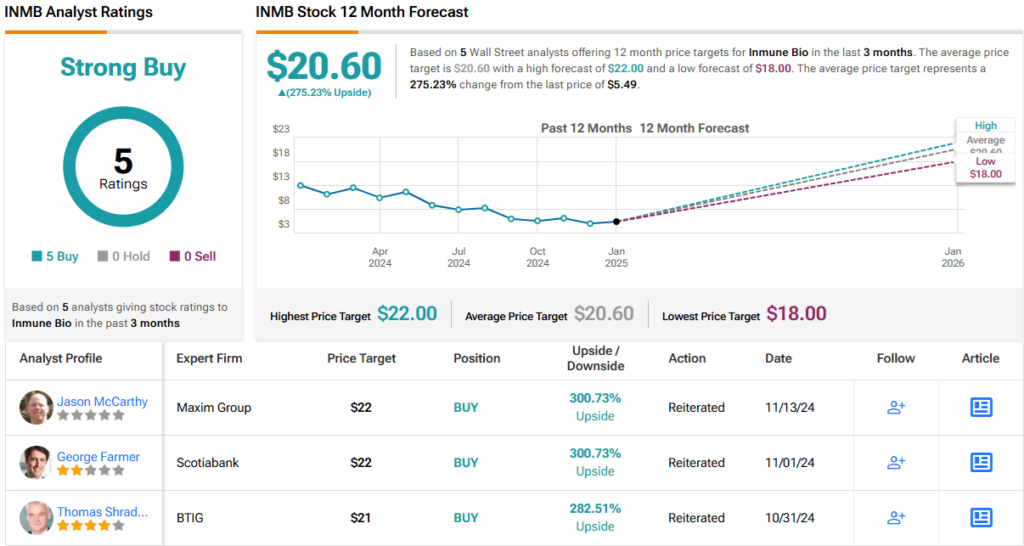

To this end, Nachman rates INMB an Outperform (i.e., Buy), along with an $18 price target that indicates his confidence in a 12-month gain of 228%. (To watch Nachman’s track record, click here)

The rest of the Street appears to echo Nachman’s sentiment. With 5 unanimous Buy recommendations, INMB earns a Strong Buy consensus rating. The average price target of $20.60 indicates an impressive upside potential of 275%. (See INMB stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.