Qualcomm (QCOM) kicked off 2025 with a bang, reporting stellar earnings for its first 2025 quarter. The semiconductor giant posted revenues of $11.67 billion, marking an 18% jump from the previous year. Adjusted earnings per share (EPS) also saw a significant rise, hitting $3.41, up 24% year-over-year. This impressive performance was fueled mainly by a 20% surge in chip sales, with the smartphone sector alone experiencing a 13% boost. However, despite these substantial numbers, Qualcomm’s stock took a hit, dropping nearly 5% in after-hours trading.

QCOM Stock Takes a Hit

The culprit? Concerns over the company’s licensing business. While chip sales are thriving, the licensing segment faces uncertainty following the expiration of a lucrative agreement with Huawei. Even though Qualcomm’s Q2 forecast looks promising—with projected sales of $10.75 billion and an adjusted EPS of $2.80, both exceeding analysts’ expectations—investors are still cautious about the future of the licensing business.

Analysts have mixed reactions to the report. Some remain bullish, highlighting Qualcomm’s growing diversification into automotive and IoT chips. Others are more cautious, pointing to potential risks such as Apple’s move to develop its modems and the unpredictable dynamics of the Chinese market. The sentiment is cautiously optimistic, but the licensing concerns are hard to ignore.

Qualcomm and Arm Settle Legal Dispute

In other significant news, Qualcomm and Arm (ARM) have resolved their legal dispute. The conflict revolved around Qualcomm’s acquisition of Nuvia and its use of Arm’s chip designs, which had created uncertainty for both companies. Recently, Arm withdrew its threat to terminate Qualcomm’s license agreement, allowing their partnership to continue smoothly.

This resolution is a big win for Qualcomm, securing a crucial part of its long-term strategy. It also stabilizes Arm’s relationship with one of its major customers, which is vital as Arm continues expanding its semiconductor industry footprint. The settlement brings much-needed clarity and confidence to stakeholders in both companies and the broader tech sector. With these earnings and legal challenges behind it, Qualcomm now faces the task of maintaining its momentum in an increasingly competitive market.

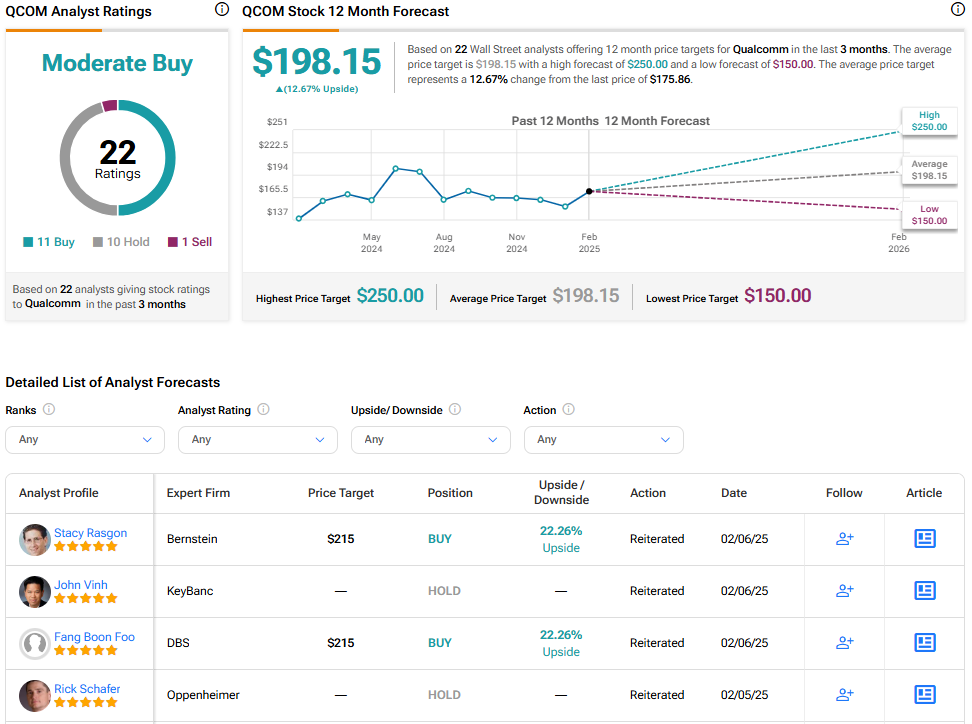

Is QCOM Stock a Buy?

On Wall Street, Qualcomm is considered a Moderate Buy. The price target for QCOM stock is $198.15, implying a 12.67% upside potential.