Qorvo (QRVO) has updated its financial guidance for the fiscal 2021 second quarter, citing better-than-expected mobile demand for its advanced 4G and 5G mobile products.

The company is now forecasting Q2 revenue of $1-1.03B, easily topping the original $925-955M outlook. That’s with $2.14 EPS guidance at the revenue midpoint (vs its former midpoint guidance of $1.90). Meanwhile Qorvo has retained its prior gross margin forecast of 50%.

Shares are now rising 7% in Wednesday’s pre-market trading, with the stock down 2% on a year-to-date basis. (See QRVO stock analysis on TipRanks).

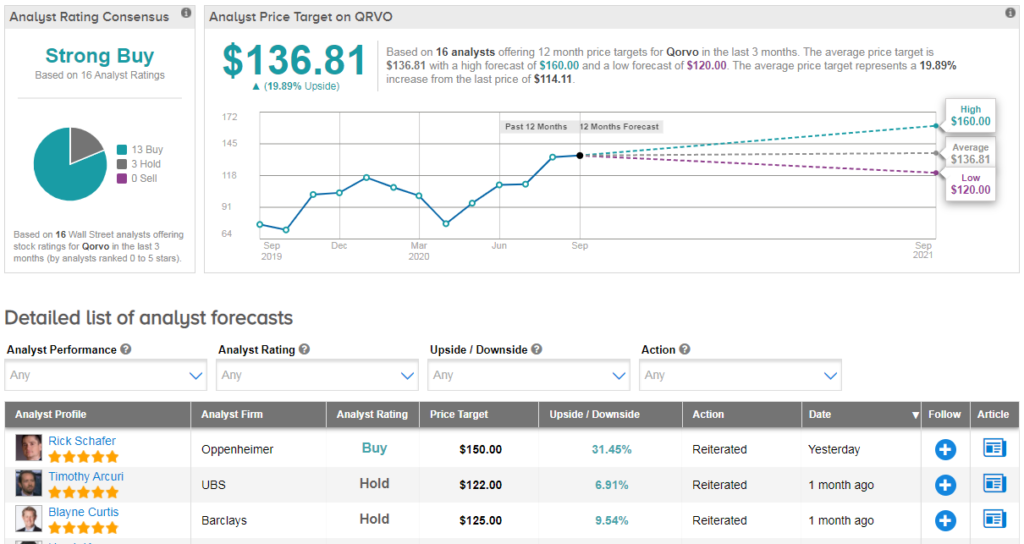

Based on the last three months of ratings, analysts have a bullish Strong Buy Street consensus on QRVO, with an average analyst price target of $137 (20% upside potential).

“We’re raising our QRVO estimates after mgmt. pre-announced solid F2Q (Sept.) upside, led by mobile” cheered Oppenheimer’s Rick Schafer following the announcement. He took his CY21/CY22 EPS from $7.63/$8.82 to $8.05/$9.20, while reiterating a buy rating and $150 price target.

“F2Q topline, better by 8%, reflects stronger 5G handset units led by Apple’s soon to launch iPhone 12” he commented. The analyst now estimates the mobile segment at $720M, up 54% Q/Q (+16% Y/Y), with QRVO’s RF content growing $5–7 across low/mid/high-tier smartphones sub-6GHz.

Schafer recently upgraded Qorvo to Outperform on a combination of improved mgmt. execution and Infrastructure and Defense Products (IDP) momentum. “We see IDP leading growth/upside in the years ahead, improving mix and helping GM expand into the mid-50%s over time” Schafer concluded.

Related News:

Microsoft Unveils Xbox Series S Gaming Console At $299

Google Scraps Plan To Rent Large Office Space In Dublin – Report

Disney’s Streaming App Downloads Jump 68% On ‘Mulan’ Debut – Report