Peloton (PTON) skyrocketed 25% during regular trading hours after ending its Fiscal year with a strong showing. Peloton reported Q4 revenue of $644 million, reflecting a modest year-over-year growth of 0.2%—its first revenue increase since Q2 2022—beating analysts’ forecast of $573 million.

According to CEO John Foley, the results reflect “continued progress on a number of financial goals,” alongside a stable financial foundation that allows for renewed focus on innovation. Notably, Peloton’s subscription segment, a key area of strength, brought in $431 million, representing a 2.3% increase over last year and delivering a robust gross margin of 68.2%.

PTON’s EPS Improvement Shows Progress Toward Profitability

The company’s earnings per share (EPS) still reported a net loss at negative $0.08, but showed notable improvement. In fact, Peloton’s EPS fared better than the analysts’ consensus estimate of negative $0.15. Peloton reduced its net loss to $30 million in Q4, an improvement of $211 million year-over-year. The company’s GAAP net income loss also saw a quarter-over-quarter increase, indicating that Peloton’s restructuring efforts are yielding results. With Adjusted EBITDA coming in at $70 million—an impressive $105 million increase year-over-year—Peloton posted positive free cash flow for the second consecutive quarter.

Peloton’s Subscription Segment Proves Resilient

Peloton’s Subscription segment, a standout performer, made a solid contribution to the bottom line. CEO John Foley highlighted the subscription base as a low-churn segment with promising gross margins. The average monthly paid subscription churn was stable at 1.9%, benefiting from low turnover in subscribers who remained committed to the platform despite cost adjustments.

PTON Share Repurchases Add Value

Peloton’s capital allocation strategy included significant share repurchases this quarter. The company executed stock buybacks to reinforce its commitment to shareholder value, as part of a broader strategy to manage its financial outlook and improve returns. “We have a stable foundation that allows us to focus on capital returns and shareholder value,” noted CFO Jill Woodworth.

Peloton Expands its Offerings

Peloton introduced the Bike+ rental program in the UK, which saw strong uptake, contributing to the company’s subscriber growth. The secondary market for Peloton’s refurbished equipment also grew, with subscriber additions up 16% year-over-year. This development points to an increasing appetite among price-sensitive consumers.

Peloton’s Outlook Remains Cautious

Peloton’s outlook remains cautious, with predictions for hardware sales to slow in Q1 due to typical seasonality and a tightening of promotional strategies. However, CEO John Foley expressed optimism regarding Peloton’s growth trajectory, given its adjusted focus on efficient marketing spend and cost savings from the restructuring plan, which achieved $15 million in savings last quarter

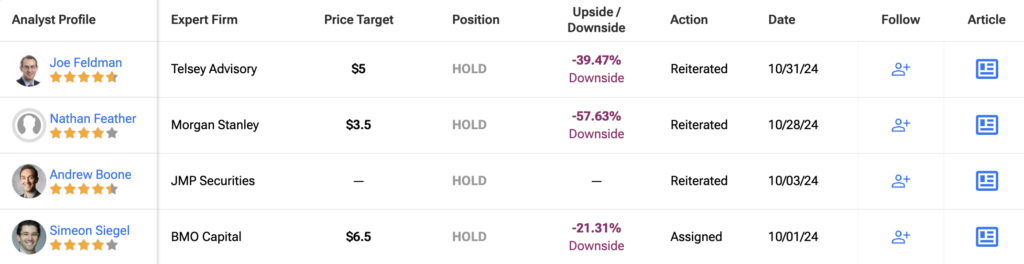

Is PTON Stock a Good Buy?

Turning to Wall Street, analysts have a Hold consensus rating on PTON stock based on two Buys, 13 Holds, and one Sell assigned in the past three months, as indicated by the graphic below. After more than an 80% increase in its share price over the past year, the average PTON price target of $5.19 per share implies 41.2% downside potential.