Progressive Corp.’s 3Q EPS jumped 82% to $2.59 year-over-year, mainly driven by double-digit growth in net premiums. The insurance company’s quarterly earnings also came way higher than analysts’ expectations of $1.72.

Maximize Your Portfolio with Data Driven Insights:

- Leverage the power of TipRanks' Smart Score, a data-driven tool to help you uncover top performing stocks and make informed investment decisions.

- Monitor your stock picks and compare them to top Wall Street Analysts' recommendations with Your Smart Portfolio

Progressive’s (PGR) net premiums written grew 14% to $11 billion in the third quarter year-on-year. During the same period, net premiums earned increased 11% to approximately $10 billion but fell short of the Street consensus of $10.9 billion.

Progressive recorded a nearly eight-fold increase in its 3Q net realized gains on securities, which reached $532.6 million. The combined ratio, which reflects the percentage of premiums paid out as claims and expenses, contracted 410 basis points from the prior-year quarter to 87.8. (See PGR stock analysis on TipRanks).

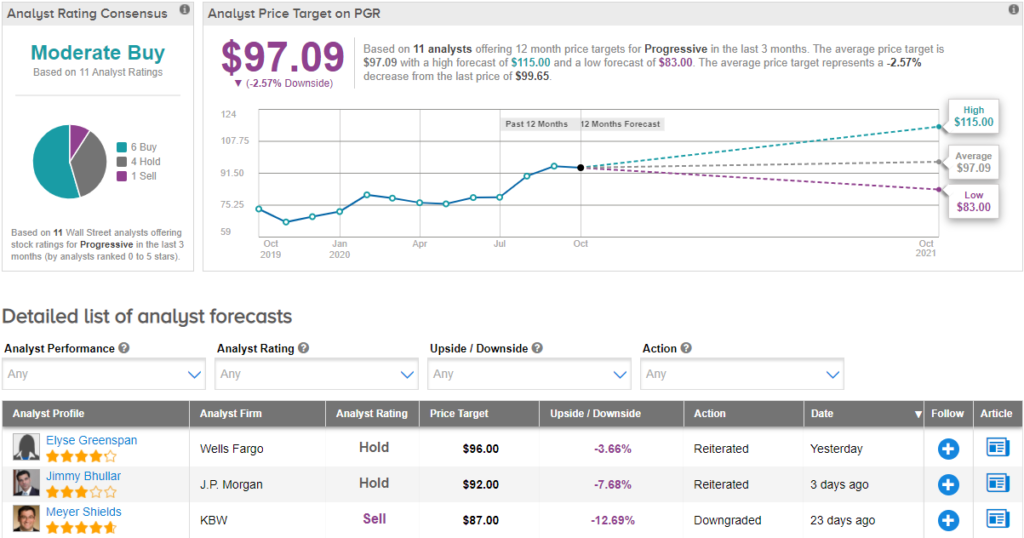

Following quarterly results, Wells Fargo analyst Elyse Greenspan said that the upside in Progressive’s 3Q EPS “reflects a better underlying loss ratio, which more than offset lower investment income and higher catastrophe losses than we had expected.” However, Greenspan reiterated a Hold rating and a price target of $96 (3.7% downside potential), saying that the stock is “fairly valued at current levels.”

Currently, the Street has a cautiously optimistic outlook on the stock. The Moderate Buy analyst consensus is based on 6 Buys, 4 Holds and 1 Sell. With shares up nearly 38% year-to-date, the average price target of $97.09 implies downside potential of 2.6% to current level.

Related News:

Citigroup Tops 3Q Profit; Oppenheimer Sees 129% Upside

Bank of America Slips After 3Q Revenue Miss; Analyst Sticks To Buy

Goldman Crushes 3Q Estimates As EPS Jumps 102%