After an incredible run over the last six months, during which shares of online personal finance pioneer SoFi Technologies (SOFI) surged by triple digits to their peak at the end of January, the stock now seems to have hit a wall, losing almost 30% of its value since then. SOFI stock has risen 80% over the past six months but has fallen 17% over the last three. This spells a neat buy-the-dip opportunity for long-term SoFi bulls like me, especially since the company’s fundamentals are much stronger than they were a year ago. This is evident in the fact that SoFi’s forward earnings multiple is lower than it was before its substantial rally.

In other words, SoFi has boosted profitability, leading to a drop in the P/E ratio while its share price soared. At current multiples, SOFI stock isn’t exactly a bargain and remains a risky investment—highly correlated with broader market swings. However, there is room for a bullish case for SoFi, particularly for long-term investors.

Reasons Behind SoFi’s Underperformance

Since its peak at the end of January, SoFi’s stock has dropped nearly 30%, showing a much steeper decline than the broader market. This is partly because SoFi is a high-beta stock, averaging a beta of 1.80 per month over the last five years. That means it tends to be 80% more volatile than the S&P 500.

The broader market has also been highly volatile recently, with many mixed developments from Trump’s administration regarding new tariffs. Tariffs are typically bad news for the economy because they create uncertainty, and the market generally doesn’t respond well to protectionist measures. They increase costs for businesses importing products and make it harder for companies to plan for the year ahead.

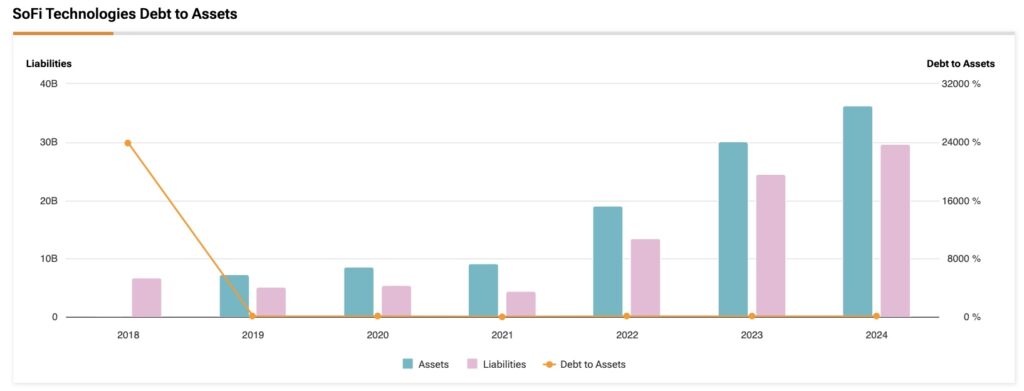

For SoFi specifically, the fintech company makes billions of dollars in outstanding loans. If there’s an economic slowdown, SoFi will be hit quickly because it lends in one of the riskiest segments—the personal loan market, where people tend to default first. SoFi is particularly exposed, with over $20 billion in liabilities on its balance sheet tied to personal loans.

Here’s a practical example of how the macroeconomic environment impacts SoFi. Looking back at Q1 last year, SoFi had already informed the market that its lending business would shrink by 5% compared to 2023. This wasn’t because of a lack of demand but because the company was more cautious about how much it was willing to lend. However, in 2024, CEO Anthony Noto announced a turnaround and updated SoFi’s annual guidance, saying that lending revenues would match or even outperform 2023 levels.

Much of this turnaround was tied to expectations around monetary policy, which plays a crucial role in a lending company’s projections, particularly with the Federal Reserve’s more dovish stance in 2024. In fact, this was one of the main reasons SoFi’s stock surged by around 140% from September 2024 to late January 2025.

SoFi’s De-Risked Business Plan

While SoFi’s performance might have lost momentum over the last month, this doesn’t reflect the company’s fundamentals, which are stronger than they were a year ago.

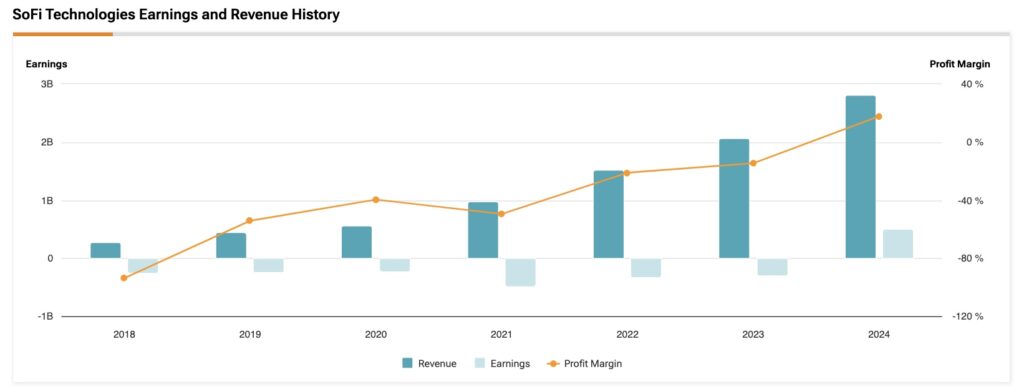

The fintech pioneer made progress across every key metric in its latest quarterly results. As just a few highlights from its stellar numbers: SoFi had its biggest quarter for member growth in Q4, adding 785,000 new members. Since Q2 2023, the company has added at least 500,000 new members each quarter. Moreover, the total capital deposited on SoFi’s platform exceeds $25 billion, which is a 39% increase compared to the end of 2023.

Looking at the bigger picture, SoFi saw a 21% jump in net revenue in 2024. But even more important is the company’s success in diversifying its revenue streams. For instance, from 2019 to 2020, over 90% of SoFi’s revenue came from lending, and by the second half of 2022, that number was still around 70%. But in Q2 2024, lending accounted for just over half of SoFi’s revenue, dropping to 56%. This shift was driven by strong growth in SoFi’s financial services segment, which reached $821.5 million in 2024, marking an annual increase of nearly 88%, and now represents 30% of the company’s revenues.

As SoFi’s business becomes more diversified and less reliant on loans, it naturally reduces the risks associated with its operations.

SoFi’s Underappreciated Valuation

At 50x its forward earnings, SoFi certainly isn’t a cheap stock, especially compared to the banking industry average of 11x. However, there’s an argument to be made that SoFi should be priced more like a tech stock in its early growth stages. That said, as SoFi’s business fundamentals continue to improve each quarter, investors buying SOFI shares at current prices are getting a much better deal than those who purchased a year ago when the forward price-to-earnings ratio was nearly 70x.

Needless to say, I find this multiple rather compelling, especially since SoFi’s business is derisked via product diversification, meaning it should start decoupling from broad market trends. However, one thing to watch is the high short interest in SoFi, which still stands at 12.7%. This suggests that the market isn’t fully pricing SoFi as a disruptive fintech but as just another tiny lender.

Is SoFi Technologies a Buy, Sell, or Hold?

On Wall Street, analysts have mixed opinions on SOFI stock. Based on 16 ratings over the last three months, six analysts rate SOFI stock as a Buy, six as Hold, and four rate it as a Sell. The average price target on SOFI is $14.31 per share, which suggests an upside potential of ~9% from the current share price.

SOFI Stock Fits Investors Who Can Afford to Ignore Volatility

I am bullish on SOFI stock and rate it as a Buy because I believe it wields everything it needs to outperform the market. This is driven by improving fundamentals and increasing revenue diversification, which has helped reduce its volatility. However, there are some potential risk factors worth considering.

Owning SoFi stock is not straightforward, with sharp volatility as part of the package, despite its avid diversification streak and solidifying fundamentals in 2024. Now could be a good opportunity for long-term investors to buy into SoFi at discounted levels even though further downward re-ratings may follow. The company’s fundamentals have improved over the past year while its valuation is lower than a year ago, before its year-end rally. When prices and fundamentals disconnect, the risk-reward opportunity becomes clear.

Given the confluence of current conditions, buying SOFI stock is a prudent trade, but not for everyone. Long-term investors who can afford to hold SOFI stock despite its gyrations may find that, ultimately, when broader economic conditions normalize, personal loans will continue to thrive, and SOFI’s business model will be well-positioned to capitalize in an advantageous interest rate environment while it stays resilient in a disadvantageous one.