Shares of Poshmark, Inc. (POSH) plummeted 26.4% during the extended trading session on November 9 after the company reported weaker-than-expected third-quarter results and slashed its revenue guidance for the fourth quarter.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

POSH is an e-Commerce portal for buying and selling new or used clothing, shoes and accessories. Shares of the company have lost 75.8% year-to-date.

The disappointing performance can be attributed to Apple’s (AAPL) privacy changes introduced in April. These changes prohibited advertisers from tracking iPhone users without their approval, forcing POSH to spend more on advertising and marketing strategies to attract customers.

Disappointing Q3 Results

The company reported a quarterly loss of 9 cents per share, 2 cents higher than analysts’ estimated loss of 7 cents per share. In the year-ago period, POSH posted a quarterly profit of 44 cents per share.

Meanwhile, net revenue climbed 16% year-over-year to $79.7 million but missed the consensus estimate of $82.69 million.

During the third quarter, Gross Merchandise Value (GMV) grew 18% year-over-year to $442.5 million. Similarly, trailing 12 months Active Buyers grew 17% year-over-year to 7.3 million.

See Analysts’ Top Stocks on TipRanks >>

Management Comments

Commenting on the results, Manish Chandra, the Founder and CEO of Poshmark, said, “We delivered a solid quarter and our sixth consecutive quarter of operating profitability, despite difficult comparisons and the headwinds of Apple privacy changes, and our investments in marketing accelerated Trailing-Twelve-Months Active Buyer growth.”

Chandra added, “We have a long runway of growth ahead, driven by strategic investments in product innovation, opening our platform to larger brands with Brand Closets, and expanding authentication services to cement our marketplace as the trusted choice for buyers, all of which will help fuel long-term growth of our business.”

Guidance

Based on the current economic environment and business momentum, Poshmark forecasts fourth-quarter revenue to fall in the range of $80 million to $82 million, significantly lower than the consensus estimate of $85.1 million.

Analysts’ View

Responding to Poshmark’s poor performance, analyst Scott Devitt of Stifel Nicolaus maintained a Buy rating on the stock but lowered the price target to $28 from $48 (14.15% upside potential).

Noting that headwinds from Apple’s privacy changes have impacted the company to a greater degree than expected, the analyst said, “Poshmark increased marketing expenses to counter Apple privacy changes… In addition, the uncertainty stemming from COVID had led to a slower ramp in international markets, which will likely impact FY:22 growth relative to prior expectations.”

Devitt concluded, “POSH shares have been in free fall since shortly after the IPO. We think the company will eventually pull it together and that an investor can receive an above-average return from an after-hours price of $18-$19. The pain of the recommendation thus far has been intense but will hopefully subside with the benefit of time.”

Overall, the stock has a Moderate Buy consensus rating based on 5 Buys and 3 Holds. The average Poshmark price target of $40.86 implies 66.57% upside potential to current levels.

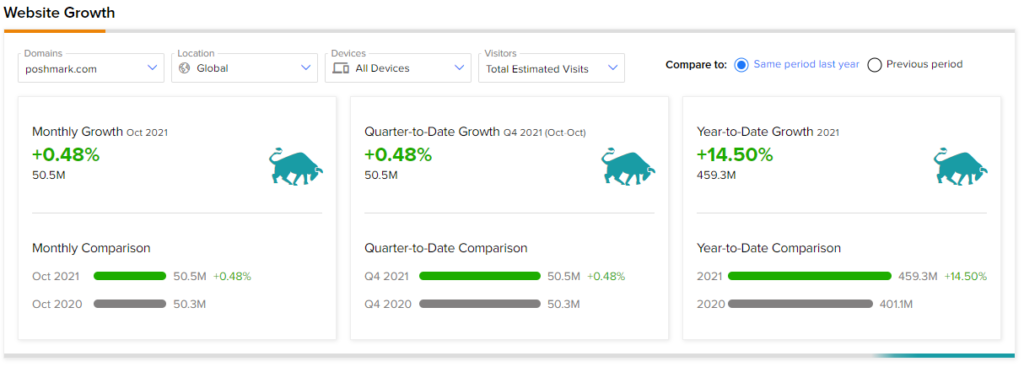

Website Traffic

TipRanks’ Website Traffic tool, which uses data from SEMrush Holdings (SEMR), the world’s biggest website usage monitoring service, offers insight into POSH’s performance.

The POSH website traffic record a modest 0.48% monthly increase in visits in October against the same quarter last year. Meanwhile, year-to-date website traffic grew 14.50% against the same period last year.

Related News:

Trade Desk Stock Up 29.5% on Stellar Q3 Results

Five9 Outperforms in Q3; Shares Up 7%

eHealth Plunges 25.6% After Disappointing Q3 Results