Carving out a niche is a challenging problem for social media companies these days, but one that stands out to me is Pinterest (PINS), with its unique blend of visual search and e-commerce.

To be sure, there’s plenty of competition with Meta (META) and Google (GOOGL) stomping in the marketplace and targeting consumers with enormous advertising budgets. There are plenty of questions about whether Pinterest can sustain growth amid this competitive landscape. Still, with consumer behavior constantly evolving, I think the platform has more than enough resilience and adaptability to warrant a Buy rating early in 2025.

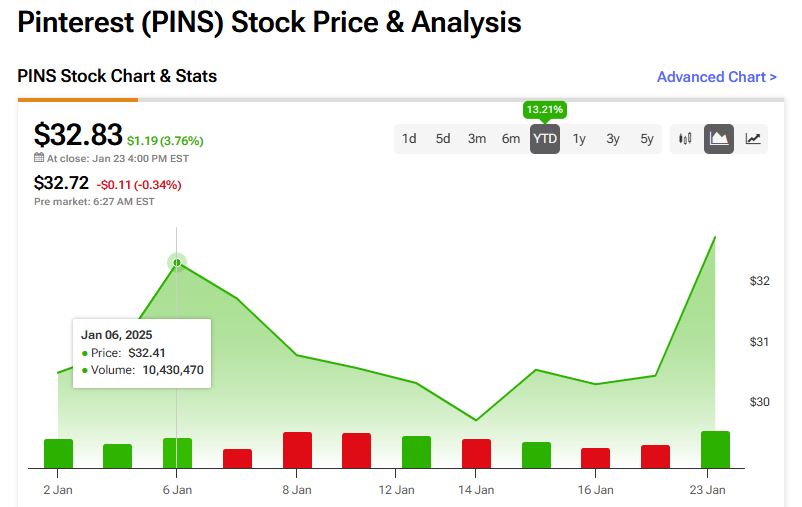

So far this year, the stock is up 13%.

Pinterest Growth Journey Points to Higher Share Price

In its latest earnings report published in November last year, PINS demonstrated how the company is moving in the right direction with a sturdy 18% rise in revenue, primarily driven by a thrifty 38% surge in international markets. Monthly active users (MAU), a key metric for all social media companies, rose to 537 million, although North American growth was sluggish. Despite this being a cause for concern since the U.S. remains a core market, I’m encouraged to see monetization improving globally at a solid 5% quarterly clip for average revenue per user (ARPU), again outshone by an 18% growth rate internationally within the same metric.

Market commentators generally agree that Pinterest’s platform is equal to TikTok in terms of advertising potential, with many users interested in finding interesting new products instead of being converted during casual scrolling. With TikTok now on shaky ground and embroiled in a squabble with U.S. authorities, the billions of advertising dollars flowing into TikTok could flow out to benefit well-positioned substitutes such as Pinterest.

Bullish Stance Backed by PINS Competitive Edge

Despite my bullish sentiment on PINS, continued growth in the sector isn’t easy. Although Pinterest has made great strides in recent years to refine its advertising model and build a viable e-commerce strategy, competition is fierce, with other players wielding greater resources and reach. In my view, Pinterest’s competitive edge is its ability to integrate direct checkout features — something other platforms have struggled with, leading to Pinterest’s ability to record rapid growth in partnerships and improvements in ad-targeting frameworks.

As with many other AI-sensitive companies, investment in AI remains a considerable risk and may not be commercially viable or not as feasible as first thought, proportional to the cost of doing so. AI-powered content discovery and advertising personalization are the next frontiers regarding user experience and advertising effectiveness. However, finding the right balance of authenticity and automation will be critical to avoid the platform losing user trust and engagement.

With impressive growth coming from international markets, I’d like to see Pinterest’s management continue to optimize the strategy to align with these key areas, namely in localizing content and tailoring advertising solutions to different regional behaviors and needs.

User Numbers and Conversion to Power Pinterest’s Climb

I’m optimistic that the firm’s high-intent user base will make it a strong contender for advertisers over the coming decades, unlike other platforms, where these are considered distractions. This typically leads to higher conversion rates and stronger advertiser retention. The opportunity to scale this within reason using AI presents further revenue potential, so I’m confident that PINS can monetize further innovations, especially with a healthy balance sheet and manageable debt levels.

That said, I do have some concerns about Pinterest’s market valuation. Many would consider a price-to-earnings (P/E) ratio of 98.7 indicative of PINS being overpriced and overburdened to deliver high expectations, given its company average being in the low 20s for the past four years.

Is PINS Stock a Good Buy?

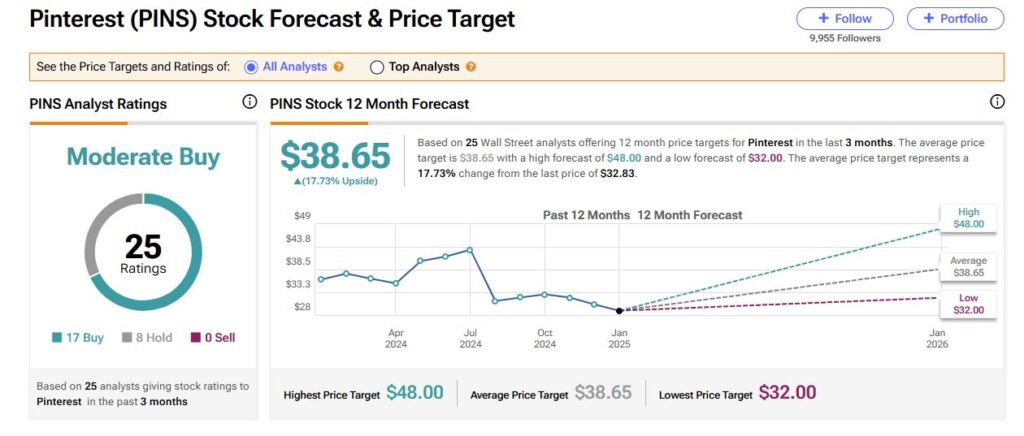

Wall Street analysts seem highly optimistic about Pinterest’s future prospects. The budding social media giant has gathered 17 Buy, eight Hold, and zero Sell ratings over the past three months, forming a Moderate Buy consensus. Moreover, PINS stock carries an average price target of $38.65 per share, which implies almost 18% upside potential from current price levels of ~$32 per share.

A bright future beckons if the company can continue to stand out in the social media crowd. Although competitors may be larger and have more users, Pinterest still holds its ground regarding marketing and advertising. PINS’ peers in the sector also have issues with regulatory headwinds, privacy concerns, and limited engagement, on which Pinterest seems relatively stronger.

Pinterest Management Inspires Confidence

On a broader basis, I forecast PINS to navigate the currently challenging time for the social media sector with resilience and, ultimately, commercial success. Despite the challenges, as much as there are plenty of risks, most notably in slowing U.S. growth, PINS has a clear path to maintain and boost revenues over time. Pinterest has a passionate and committed user base, and I expect management to keep a close eye on what their users want while sustainably scaling the business globally.

I’m also encouraged to see management investing heavily in share buybacks and continuing to push down debt levels, all helpful in attracting new investors and keeping those already at the table happy. Importantly, although we’ve seen some insiders selling the stock, it is not on a concerning scale.

Keeping costs and investments in R&D at a sensible level will also reassure investors that management is confident with, but not overly dependent on, new technology to build revenues.

PINS Resilence to Deliver Shareholder Returns

Pinterest is a unique company and compelling story that warrants an addition to my portfolio because of its unique blend of social engagement and e-commerce that keeps both end-users and advertisers happy — all while making substantial advertising revenues that can sustain market shocks and blistering competition. Over the coming years, as AI and further novelties become normalized, I expect to see PINS implementing efficiency savings and user experience improvements that will weather the changing environment while recording solid commercial performance that rewards shareholders.

Of course, there are risks related to valuation and competition. Still, with plenty of negativity already priced into the stock, I see PINS as an attractive balance of risk and reward.