Pinterest shares (PINS) tanked in after-hours trading after the social media company released its second-quarter earnings report, which was accompanied by a soft outlook. Revenue increased by 20.5% to $853.68 million, which beat the estimated $848.1 million. This growth was driven by strong performance across all regions. As a result, adjusted EPS of $0.29 beat estimates of $0.28.

In addition, global monthly active users climbed 12% to reach 522 million, while revenue per user globally rose 8% to $1.64. When breaking down the numbers further, the U.S. and Canada saw a 16% increase to $6.85, Europe saw a 14% rise to $1.03, and the rest of the world grew 13% to $0.13.

Looking forward, management now expects revenue and operating expenses for Q3 2024 to be in the ranges of $885 million to $900 million and $485 million to $500 million, respectively. For reference, analysts were expecting $909.5 million in revenue.

It’s also worth noting that this outlook states that the increase in operating expenses (17%-20%) will outpace revenue growth (16%-18%). This is an undesirable sign, as it suggests that the business is unable to achieve operating leverage. This essentially means that scaling the business higher will hurt profitability margins. This weak outlook is what caused shares to plunge.

Is PINS Stock a Buy?

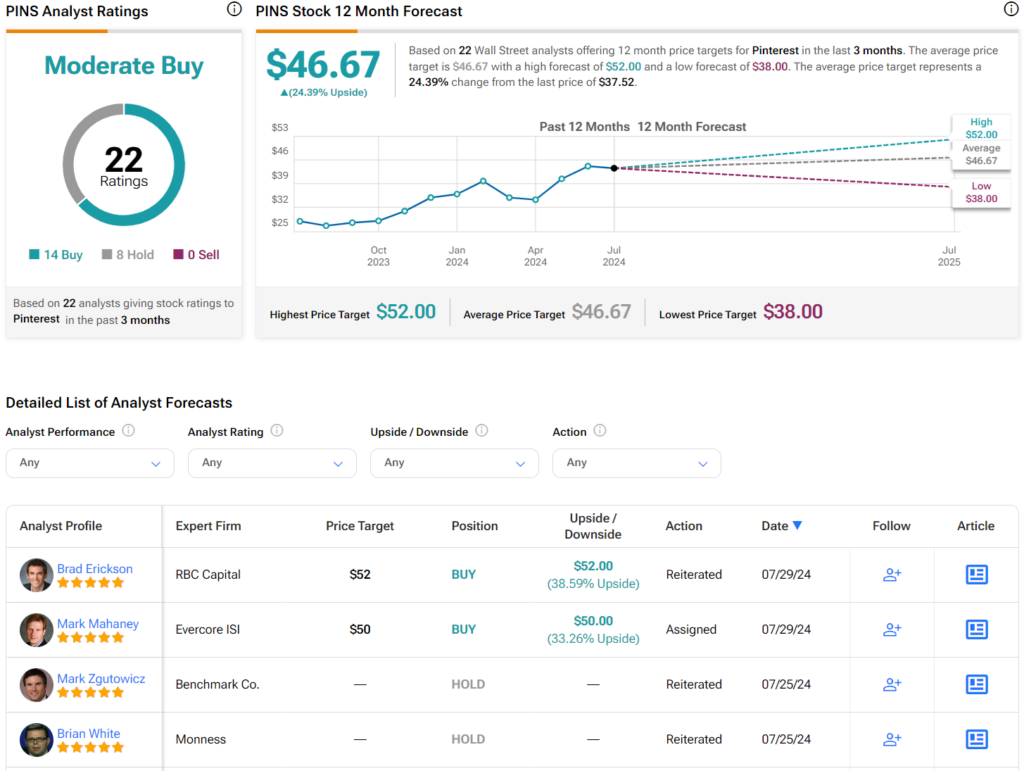

Turning to Wall Street, analysts have a Moderate Buy consensus rating on PINS stock based on 14 Buys, eight Holds, and zero Sells assigned with an average PINS price target of $46.67 per share. However, it’s worth noting that estimates will likely change following today’s earnings report.