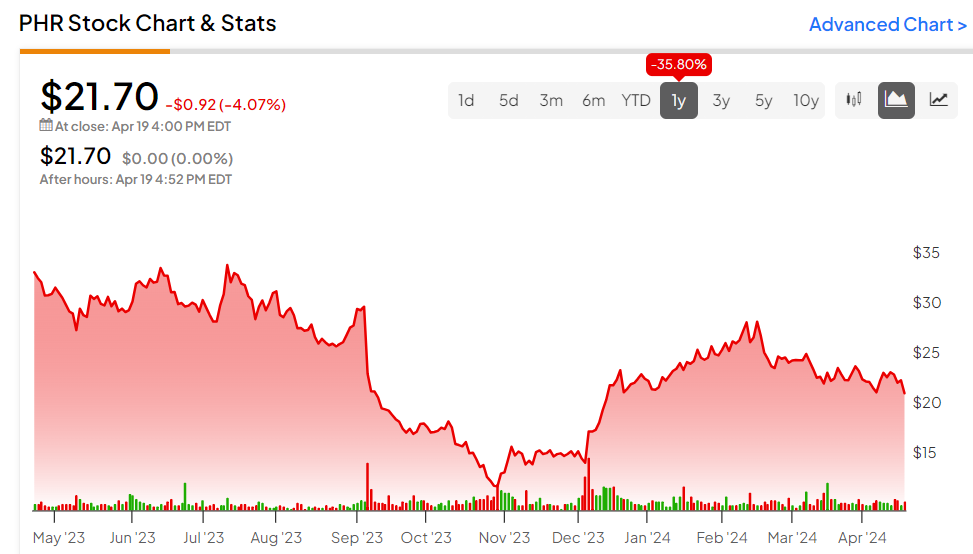

The healthcare system continues to struggle with no shortage of challenges following the global pandemic, including grappling with a severe shortage of qualified labor. Technological solutions, like those provided by Phreesia (NYSE:PHR), are well-positioned for tremendous growth. The stock has shed roughly a third of its value over the past year. Still, revenue continues to grow, and the stock looks cheap based on historical measures, making it an intriguing healthcare tech value play for long-term value investors.

Phreesia Is a Growing Provider to the Healthcare Industry

Phreesia is a technology provider that caters to the healthcare industry, offering solutions that enhance operational and financial performance for medical organizations. It provides a varied suite of services through a SaaS-based platform, which manages critical aspects such as patient access, registration, payments, and clinical support. The suite also entails initial patient contact, appointment scheduling, and post-appointment patient surveys.

Its solutions target health systems, multi-specialty practices, and Federally Qualified Health Centers. The company equips providers with robust tools for patient registration, scheduling, payments, and clinical support to enhance efficiency and improve care delivery. Furthermore, the firm reported facilitating over 150 million patient visits in Fiscal year 2024, about one-tenth of all patient visits in the U.S.

The company has estimated that its total addressable market is valued at $10 billion, representing significant growth potential.

Phreesia’s Financials & Outlook

The company’s fiscal fourth quarter, ending January 31, 2024, demonstrated robust growth. Total revenue reached $95 million, a 24% year-over-year increase, surpassing the consensus estimates of $93.53 million. The net loss for this quarter was $30.6 million, which is noticeably lower than the $38 million loss from the same period in the prior year. Meanwhile, an EPS of -$0.56 was in line with expectations.

For Fiscal year 2024, the company reported total revenue of $356.3 million, a 27% increase year-over-year. The net loss for the year was $136.9 million, an improvement over the net loss of $176.1 million in Fiscal year 2023. Despite this, cash and cash equivalents, as of January 31, 2024, decreased to $87.5 million, plunging from $176.7 million recorded on January 31, 2023. Management believes that together with regular operational earnings, this cash level is sufficient for achieving the projected revenue and Adjusted EBITDA for 2025.

For Fiscal year 2025, management has given guidance for revenue expected in the range of $424 to $434 million, indicating a year-over-year growth rate of 19% to 22%.

Is PHR Stock a Buy, Hold, or Sell?

The stock had a nice run from December to February, though it has been trending downward since, shedding -12% in the past three months. It shows negative price momentum, trading below the 20-day (23.35) and 50-day (23.70) moving averages. However, the slide in price has pushed the stock into value territory, with its current P/S ratio of 3.2x less than half its historical average of 8.0x.

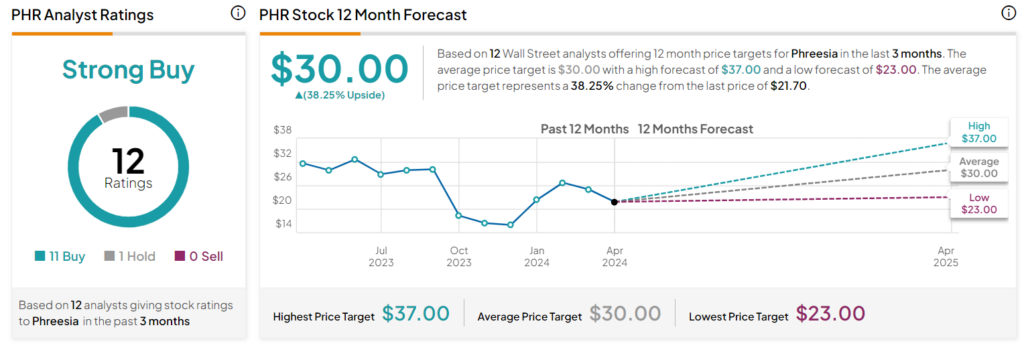

Analysts following the company have been mostly bullish on the stock. For example, JMP Securities analyst Aaron Kimson recently raised the firm’s price target on Phreesia to $30 from $28, keeping an Outperform rating on the shares. He cites the company’s traction with the provider community and strong market position as drivers of growth.

Phreesia is rated a Strong Buy based on the recommendations and 12-month price targets issued by 12 Wall Street analysts in the past three months. The average price target for PHR stock is $30.00, which represents a 38.25% upside from current levels.

Final Thoughts on Phreesia

As the healthcare industry grapples with post-pandemic fallout, technological solutions like those provided by Phreesia could prime the company for remarkable growth. While operating at a net loss is a concern, the company is projecting ongoing revenue growth. The stock’s current value sets up the potential for substantial returns, making it an appealing prospect for savvy investors.

Questions or Comments about the article? Write to editor@tipranks.com