Shares of Philip Morris plunged 5.8% on Tuesday after its 4Q earnings guidance fell short of analysts’ expectations. The cigarette maker expects to report EPS of $1.16 ($1.20 excluding currency headwinds) in 4Q, while the Street consensus is pegged at $1.25. The lower-than-expected guidance reflects a shift in planned costs to 4Q.

Invest with Confidence:

- Follow TipRanks' Top Wall Street Analysts to uncover their success rate and average return.

- Join thousands of data-driven investors – Build your Smart Portfolio for personalized insights.

Philip Morris (PM) also registered a year-over-year decline in its 3Q top and bottom-line results. The company’s adjusted EPS dipped 0.7% to $1.42 year-on-year, while revenues decreased by 2.6% to $7.45 billion. Quarterly results were negatively impacted by a 7.6% decline in total cigarette and heated tobacco unit shipment, which more than offsets the benefit of favourable pricing variance and lower manufacturing costs.

Nonetheless, Philip Morris’ 3Q revenues and earnings surpassed Wall Street estimates of $7.28 billion and $1.36 per share, respectively. (See PM stock analysis on TipRanks).

The company raised its full-year earnings outlook. It now projects adjusted EPS at constant currency basis between $5.37 and $5.42, up from the earlier guidance range of $5.23-$5.38. Moreover, the company forecasts total cigarette and heated tobacco unit shipment volumes to fall 8%-9% in 2020, compared to its previous anticipation of a 8%-10% decline.

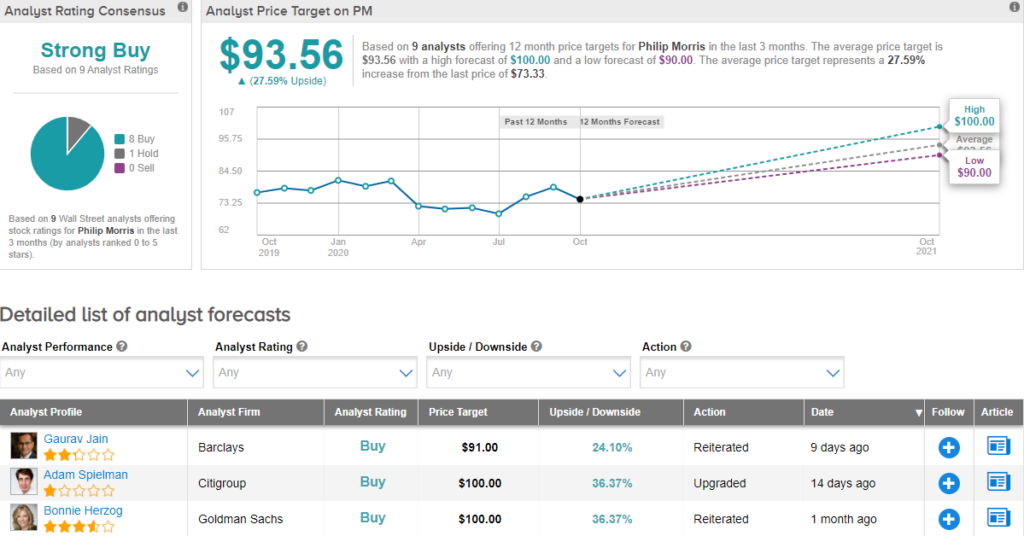

Ahead of the 3Q results, Citigroup analyst Adam Spielman upgraded the stock to Buy from Hold and raised the price target to $100 (36.4% upside potential) from $82. In a note to investors on October 7, Spielman said that Philip Morris is expected to achieve 175 billion sticks of reduced risk products by 2024. The analyst is also optimistic that the company could announce a new multi-year target of achieving 150-200 billion sticks by 2024, which will be way up from the current three-year goal of 90-100 billion sticks by 2021.

Currently, the Street is bullish on the stock. The Strong Buy analyst consensus is based on 8 Buys versus 1 Hold. The average price target of $93.56 implies upside potential of about 27.6% to current levels. Shares have plunged by about 13.8% year-to-date.

Related News:

Agree Realty’s 3Q Sales Soar 33% On Property Acquisitions

Crown Holdings Posts 3Q Profit Win, Initiates Dividend Pay

PPG Slips In After-Market As 3Q Sales Volume Drops