Philip Morris International announced that it is raising its regular quarterly dividend by 2.6% to an annualized rate of $4.80 per share.

Stay Ahead of the Market:

- Discover outperforming stocks and invest smarter with Top Smart Score Stocks

- Filter, analyze, and streamline your search for investment opportunities using Tipranks' Stock Screener

Shares closed 1.8% higher at $80.47 on Wednesday after Philip Morris (PM) said that its board of directors increased its quarterly dividend to $1.20 per share, up from $1.17 per share. The dividend is payable on October 13, 2020, to shareholders of record as of September 24, 2020. The ex-dividend date is September 23, 2020.

Tobacco giants including Philip Morris have been under pressure as health awareness, a stricter regulatory environment and the emergence of alternatives like e-cigarettes over recent months have led to a decline in cigarette volumes. Yet, some investors prefer these companies for their high dividend yields. Philip Morris has increased its annual dividend every year since becoming a public company in 2008, representing a total increase of 160.9%, or a compound annual growth rate of 8.3%.

Furthermore, the company has been focusing on capturing the demand for heated tobacco products and its IQOS tobacco heating device to offset a decline in cigarette shipments.

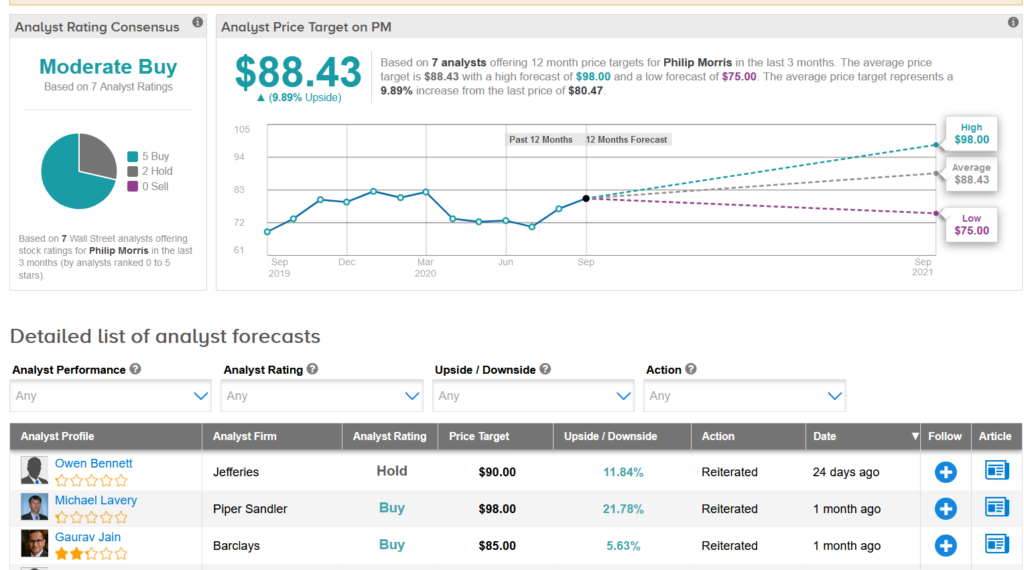

Shares in PM are currently trading down 5.5% year-to-date after recouping a chunk of this year’s earlier losses, and analysts have a cautiously optimistic Moderate Buy consensus on the stock’s outlook. This is with a $88.43 average analyst price target (9.9% upside potential).

Jefferies analyst Owen Bennett last month raised the stock’s price target to $73 from $70 due to FX gains but maintained a Hold rating noting that an expected volume miss and multiple headwinds in 2021 could be overlooked by investors. (See Philip Morris stock analysis on TipRanks).

“The bigger risk for us on PM (vs. cigs), and the reason we remain cautious near term, is possible heated slowdown,” Bennett wrote in a note to investors. “While we increase our estimates for the current year, we do think the pace of growth could slow into FY21.”

Bennett expects heated volumes for FY21 at 86 billion vs the target of 90-100 billion.

“Likely a bigger risk over volumes is to sales, and the threat of heated taxes. We think as we enter a recession, increased taxes are likely. The best indicator of this is Italy, the largest EU heated market, where a widely supported amendment to hike taxes was proposed in July” he said.

Related News:

Tiffany Sues LVMH For Dumping $16B Deal; Analysts Say This Is Not The End

India’s Reliance Scores $1.02B Retail Investment From Silver Lake

KKR Plans To Inject Up To $1.5B In Reliance’s Retail Unit – Report