The COVID-19 pandemic is accelerating digitalization and has led to a spike in online transactions and e-commerce sales. According to PayPal, the penetration of e-commerce as a percentage of retail sales in the first half of 2020 outpaced prior external forecast by 3 to 5 years. Both consumers and merchants are increasingly adopting digital payments as contactless transactions have become increasingly important amid the current crisis.

Don't Miss our Black Friday Offers:

- Unlock your investing potential with TipRanks Premium - Now At 40% OFF!

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

The rapid penetration of digital payments led to double-digital revenue growth in the second quarter for PayPal and Square. Using the TipRanks Stock Comparison tool, we will place these two fintech payment firms alongside each other to assess which stock offers a more compelling investment opportunity.

PayPal Holdings (PYPL)

PayPal, which was spun off from eBay in 2015, has emerged as the digital payment leader. In the second quarter, PayPal added 21.3 million net new active accounts, reflecting a 137% Y/Y rise and marking the strongest growth in the company’s history thanks to a surge in e-commerce and digital payments. As of the end of 2Q, PayPal had 346 million active accounts with over 26 million merchant accounts.

The company’s 2Q revenue surged 22.2% Y/Y to $5.26 billion. And adjusted EPS rose 49% to $1.07 as the adjusted operating margin expanded 504 basis points to 28.2%. Total Payment Volume or TPV, which indicates payments processed through the PayPal platform, grew about 29% to $222 billion. Venmo, Paypal’s mobile payments platform, witnessed a 52% growth in its TPV to $37 billion.

Following the strong 2Q momentum, PayPal reinstated its 2020 guidance and in fact, raised it. The company expects revenue growth of 20% and adjusted EPS growth of about 25%. It anticipates adding 70 million net new active accounts this year.

To boost its top-line further and promote touchless payments, PayPal launched QR Code technology in 28 markets globally in May. CVS Pharmacy will be the first retail chain to offer its customers the option to use PayPal and Venmo QR codes at checkout in its US stores. The company will also launch Venmo credit card this year.

PayPal has also expanded its Visa Direct partnership globally to accelerate real-time access to funds for small businesses, consumers and partners across its platform. This collaboration enables PayPal to extend global white label Visa Direct payout services through PayPal and its Braintree, Hyperwallet and iZettle platforms.

On Sept. 22, Mizuho Securities analyst Dan Dolev reiterated a Buy rating for PayPal with a price target of $285 as the Mizuho E-Commerce Tracker showed that unique views across key PayPal partner sites (like Etsy, Groupon and Wayfair) remained strong in July and August and also pointed to potential signs of life in the beleaguered travel category.

The Tracker also indicated that PayPal’s unique views continued to grow ahead of partner websites in the last two months, reflecting persistent share gains for the checkout button. Overall, the analyst expects strong July and August e-commerce trends coupled with share gains to bode well for the company’s second-half TPV. (See PYPL stock analysis on TipRanks)

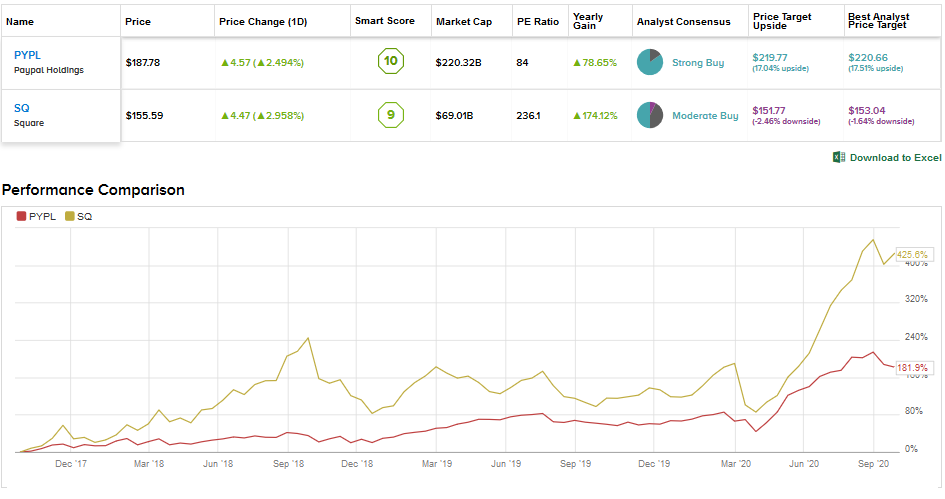

PayPal stock has rallied about 74% year-to-date and could rise further by 17% in the coming months as indicated by the average analyst price target of $219.77. The stock scores a Strong Buy consensus based on 28 Buys, 5 Holds and no Sell ratings.

Square (SQ)

Payment facilitator Square is growing rapidly as consumers and businesses are migrating online at a faster pace amid the pandemic. From February through August 2020, there was a 13.2 percentage point increase in the share of Square sellers accepting online payments and by August, over 40% of all Square sellers were accepting online payments. Also, by August, more than 7 in 10 Square sellers were accepting contactless payments.

The company’s Cash App ecosystem delivered $1.2 billion in revenue in the second quarter, reflecting a whopping 361% Y/Y growth. The Cash App had over 30 million monthly transacting active customers in June. Aside from the accelerated digital migration, Cash App also gained from the impact of Fed stimulus, unemployment checks and tax refunds.

Second-quarter revenue grew about 64% Y/Y to $1.92 billion. But excluding bitcoin revenue, net revenue of $1.05 billion was flat Y/Y. Meanwhile, 2Q adjusted EPS declined 14.3% to $0.18. The strong growth in Cash App revenue was offset by the 17% decline in the company’s core higher-margin Seller business to $723 million. Square’s gross payment volume or GPV fell 15% Y/Y to $22.8 billion.

The Seller segment was impacted by lower volumes as several businesses were forced to close amid the shelter-in-place orders triggered by the pandemic. However, the company stated that the Sellers business improved with each month in the quarter as restrictions eased and more sellers adapted to the contactless platform.

Meanwhile, GPV from online channels grew over 50% and accounted for 25% of the Seller GPV reflecting the rapid adaption of online solutions by the sellers. (See SQ stock analysis on TipRanks)

Recently, the company announced two new features called On-Demand Pay for employees and Instant Payments for employers. These new features will further integrate Square’s Seller and Cash App ecosystems to offer financial services and simplify payroll.

Loop Capital analyst Kenneth Hill has just initiated coverage of Square with a Buy rating and a price target of $169. The analyst sees a great deal of upside ahead in the fintech company, driven by further investment in the business and monetization of the Cash App. Hill also believes that on the Seller side, the SMB network should “hold in well and continue a sustained recovery.”

The Street has a cautious Moderate Buy consensus for Square with 14 Buys, 12 Holds and 2 Sells. Square stock has risen a stellar 149% year-to-date, so the average analyst price target of $151.77 indicates a possible downside of 2.5% ahead.

Bottom line

Both PayPal and Square have strong growth prospects in the digital payments world. If we look at the Street’s consensus and further upside potential, PayPal stock appears to be a better choice than Square currently.

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment