PayPal Holdings (NASDAQ:PYPL) announced better-than-expected results for the fourth quarter of 2023 on higher payment volume. Despite strong results, PYPL stock fell about 8% in yesterday’s extended trading session as the company provided weak 2024 earnings guidance.

PayPal is a digital payment platform that facilitates secure online transactions and money transfers globally.

Q4 Earnings Snapshot

PYPL’s adjusted earnings of $1.48 per share outpaced the Street’s estimates of $1.36 per share and increased 19% from the prior-year quarter. Similarly, net revenues grew about 9% year-over-year to $8 billion and slightly exceeded analysts’ estimates of $7.88 billion.

Furthermore, the company witnessed a 15% growth in total payment volume and a 14.2% jump in transactions per active account. However, the total active accounts fell 2.1% year-over-year due to the ongoing attrition of inactive accounts within less developed markets.

Looking ahead, PayPal expects first-quarter net revenue to increase by about 6.5% while adjusted earnings per share (EPS) to grow in the mid-single digits. Additionally, the company anticipates that 2024 adjusted EPS will remain flat year-over-year at $5.10 per share, below the consensus estimate of $5.51 per share.

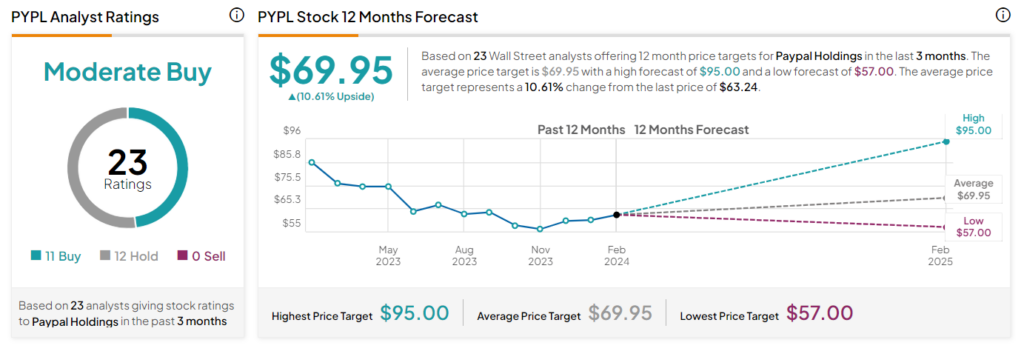

Is PYPL a Buy, Sell, or Hold?

Following the Q4 print, analyst Dan Dolev from Mizuho Securities reiterated a Hold rating on the stock with a price target of $65, implying a 2.8% upside potential.

On TipRanks, PayPal stock commands a Moderate Buy consensus rating based on 11 Buy versus 12 Hold ratings received during the past three months. The average PYPL stock price target of $69.95 implies a 10.61% upside potential from current levels. Shares of the company have gained 14.8% in the past three months.

Questions or Comments about the article? Write to editor@tipranks.com