When reporting earnings, companies can often deliver strong quarterly readouts yet fall at the guidance hurdle, and that can often result in muted investor reaction with the shares subsequently tumbling. However, while Palantir’s (NYSE:PLTR) latest results followed that template, investors were in bullish mode in the aftermath of its Q4 print.

Don't Miss our Black Friday Offers:

- Unlock your investing potential with TipRanks Premium - Now At 40% OFF!

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

Shares soared by 31% in Tuesday’s session with the big data company rewarded for its strong positioning in the AI game. The perception of Palantir is that it is too heavily reliant on government contracts, but its commercial business appears to be gaining traction with its Artificial Intelligence Platform (AIP) driving the narrative.

In Q4, revenue climbed by 19.6% year-over-year to $608.35 million, beating the Street’s call by $5.55 million. While government revenue at $324 million (up 11% y/y) claimed the bulk of that, the commercial business is closing the gap. That segment’s revenue posted a 32% year-over-year increase and a 13% sequential improvement to $284 million. Within that, U.S. commercial revenue particularly impressed, rising by 70% from the same period a year ago to $131 million. At the other end of the spectrum, adj. EPS of $0.08 was in-line with expectations.

As mentioned above, the outlook offered something of a disappointment, with Q1 revenue expected in the range between $612 and $616 million, not quite as high as the Street’s projection of $617.44 million. That, however, mattered little for investors and nor did it phase Wedbush’s Daniel Ives, a 5-star analyst rated in the top 4% of the Street’s stock pros.

The analyst compares Palantir to companies such as Nvidia, Microsoft and Palo Alto Networks, in being one where the Street had initially been unappreciative of the opportunity at play.

“A handful of times every decade there are tech companies that are so ahead of the competition and in a sweet spot of the future growth…yet the Street at the time dismisses it by dusting off their long-term stubborn bear thesis and 30 spreadsheets,” the 5-star analyst said. “Palantir went from an off Broadway play to a primetime Broadway theater right off of Times Square under the bright lights. With a US commercial business that grew an eye popping 70% in 4Q (up from mid 20% a few quarters ago) and commercial customer count that grew 44% as the AI Revolution is driving AIP deal flow to a level we did not expect until 2025.”

Ives calls Palantir an “undiscovered gem,” raising his price target from $25 to a new Street-high of $30, suggesting the stock has room for further growth of 25% from current levels. No need to add, Ives’ rating stays an Outperform (i.e., Buy). (To watch Ives’ track record, click here)

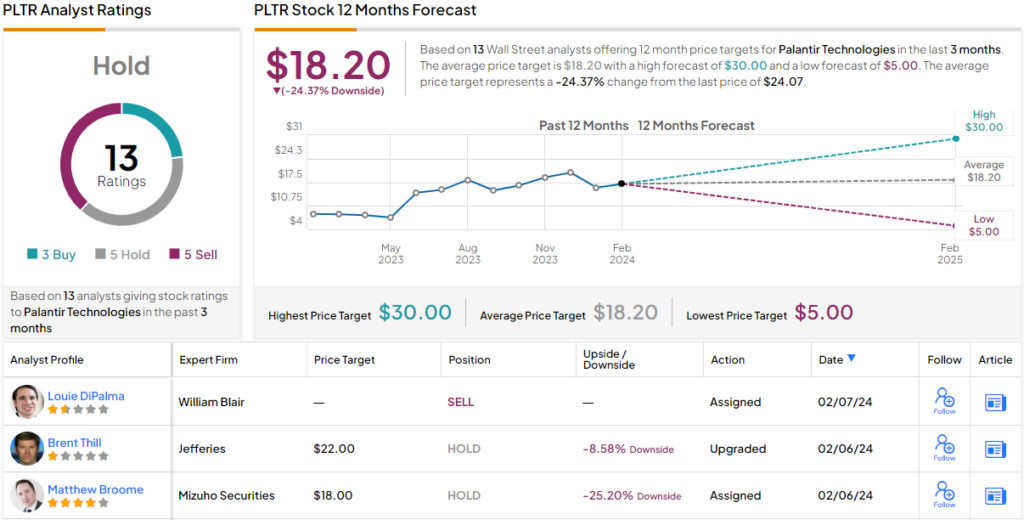

On balance, however, Ives’ take is not a popular one on Wall Street. With an additional 2 Buys only vs. 5 Holds and Sells, each, the analyst consensus rates the stock a Hold. Most seem to think the shares have overshot; the $18.20 average target factors in downside of 24% for the coming year. (See Palantir stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.