Palantir stock (PLTR) soared after its Q2 results, reinforcing the narrative of accelerating growth. The data analytics and intelligence leader reported its strongest growth in nine quarters, demonstrating significant momentum and a clear upward trend. The steady pace of new client acquisitions indicates that this growth trajectory is likely to continue. Further, Palantir’s high-margin business model positions the company for exceptional free cash flow growth in the near future. Therefore, I remain bullish on Palantir stock.

Growth Accelerates Across Government and Commercial Segments

As expected, all eyes were on the revenue growth figure when Palantir’s results were announced. The anticipation was well-founded, as the company delivered impressive numbers. Palantir’s revenue surged to $678 million, reflecting a 27% year-over-year increase and a 7% quarter-over-quarter increase.

In fact, this notable increase accelerated both from the previous quarter’s 20.8% growth and Q2-2023’s 12.8% growth, signaling exceptional performance across both Government and Commercial segments. Let’s explore the specifics of what drove this outstanding quarter.

Government Revenue: Strong Demand Across Domestic and International Markets

Palantir’s Government segment experienced a significant boost in revenues, powered by the increasing demand for its mission-critical solutions during a volatile geopolitical landscape. As Palantir’s CEO, Alex Karp, has often emphasized, the company is designed to thrive in uncertain and turbulent conditions—a fact that is clearly evident from this growth in today’s environment.

Specifically, Government revenues reached $371 million, up 23% year-over-year, marking an acceleration from the previous quarter’s growth of 16% and Q2-2023’s growth of 15%.

Domestically, Palantir’s U.S. Government revenue grew by 24% year-over-year to $278 million, benefiting from elevated demand for its software solutions. Notably, the U.S. Government business secured several critical contracts, leading to the strongest bookings quarter since 2022.

This is clearly telling of Palantir’s increasingly entrenched position within key U.S. government agencies, especially in light of the growing need for sophisticated data analytics and AI solutions in defense and intelligence operations in today’s geopolitical landscape.

Internationally, Palantir’s Government revenue rose 21% year-over-year to $93 million, primarily driven by additional funding from a partner nation in Eastern Europe. I think this reflects Palantir’s expanding footprint in global defense markets. The ongoing tensions on the international front, particularly in the Middle East, and the need for state-of-the-art technology solutions in these regions should continue to further fuel demand for the company’s offerings.

Commercial Segment: Unprecedented Growth Fueled by AI

Palantir’s Commercial segment showcased even more impressive growth, with revenues increasing 33% year-over-year to a record $307 million. Excluding strategic commercial contracts, this growth would have been an even more striking 40% year-over-year, clearly stressing the core strength of Palantir’s growth trajectory.

The U.S. Commercial business led the charge, with revenue growing by a staggering 55% year-over-year to $159 million. Palantir’s Artificial Intelligence Platform (AIP) continues to be a significant catalyst, driving new customer acquisitions and increased spending among existing clients. Also, Palantir’s Bootcamps have been instrumental in demonstrating the value of AIP to potential clients. I previously explored Palantir’s Bootcamps in an article I wrote, which you can read here if you’re interested in learning more.

In any case, the effectiveness of Palantir’s strategy is evident in the 83% year-over-year growth in U.S. commercial customer count, which now stands at 295 customers. Palantir’s International Commercial revenue grew at a more modest 15% year-over-year to $148 million, reflecting some headwinds in Europe. However, the company mentioned it is actively pursuing opportunities in Asia, the Middle East, and other regions to mitigate these challenges and sustain its growth trajectory.

Profitability Improvements and Rule of 40 to Sustain Momentum

Besides strong revenue growth, Palantir’s Q2 results showcased notable progress in profitability. Palantir achieved an adjusted operating margin of 37%, celebrating the seventh consecutive quarter of margin expansion and driving adjusted operating income to $254 million, up 88% year-over-year.

GAAP net income was equally impressive, hitting a record $134 million. This marked a 377% year-over-year growth due to the net income margin expanding to 20%. Adjusted free cash flow also hit an impressive $149 million, implying a significant margin of 22%

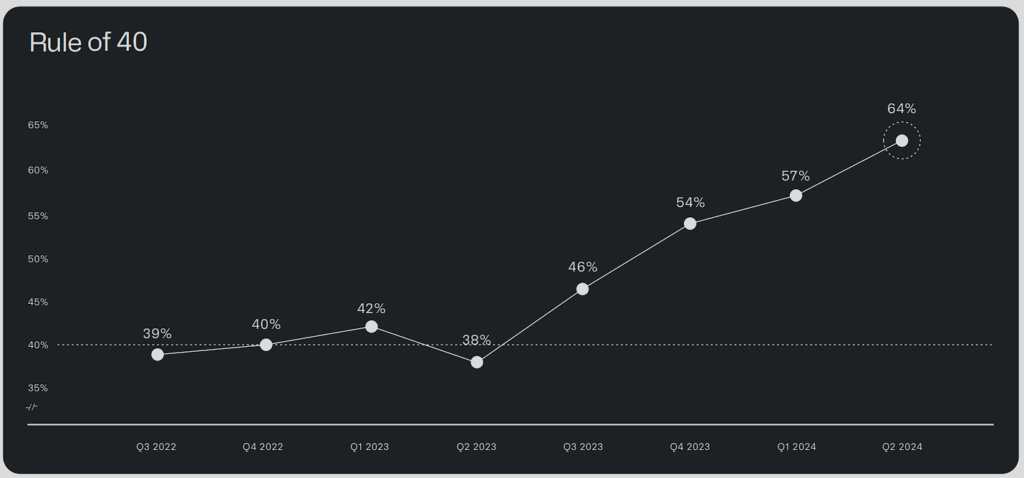

A key highlight that emerges after discussing the company’s revenue and profitability is Palantir’s Rule of 40 score, which climbed to 64% from 57% in Q1. This was achieved by combining 27% year-over-year revenue growth with a 37% adjusted operating margin (27% + 37%), as mentioned earlier. Generally, the Rule of 40 implies a company is financially healthy and efficient if it achieves a score of 40 or more.

With Palantir’s score not only greatly surprising this figure but also reaching new highs by the quarter, it’s likely that Palantir stock will retain its bullish momentum, irrespective of current valuation metrics.

Is PLTR Stock a Buy, According to Analysts?

As far as Wall Street’s view on the stock goes, Palantir features a Hold consensus rating based on three Buys, five Holds, and six Sells assigned in the past three months. At $22.42, the average PLTR stock price target implies the potential for 24.5% downside potential, which may sound rather unsettling.

If you’re wondering which analyst you should follow if you want to buy and sell PLTR stock, the most accurate analyst covering the stock (on a one-year timeframe) is Mariana Perez Mora from Bank of America (BAC) Securities, with an average return of 63.58% per rating and a 93% success rate. Click on the image below to learn more.

The Takeaway

Palantir’s Q2 results revealed continued momentum in growth acceleration, driven by both the Government and Commercial segments. The ongoing geopolitical environment is set to keep fueling the Government business, while the enduring tailwind of companies seeking effective AI solutions should keep powering the Commercial business. In the meantime, with a notable Rule of 40 score of 64%, Palantir’s momentum appears unstoppable, which, in my view, will keep the stock’s bullish sentiment alive.