On a day marked by a considerable dip in Oracle (NYSE:ORCL) shares, plummeting 12% following a slight miss in first-quarter revenue estimates, Wall Street maintains a reassuring stance on the technology powerhouse. Mizuho remains bullish with its “Buy” recommendation and a price target of $150, emphasizing Oracle’s growth in organic cloud revenue. Though sales figures as a whole missed expectations, the analysts attribute it to a seasonal dip in licenses and hardware revenues.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

On the other hand, analysts at Stifel offer a more tempered outlook with a “Hold” rating and a $120 price target, indicating perceived pressure due to limited advancements in AI. The transition phase experienced by Cerner customers, migrating from recognized license revenue to cloud subscriptions, seems to be creating certain headwinds.

Despite these challenges, Barclays Research holds a favorable “Overweight” rating, albeit with a slightly reduced price target of $147, recognizing the robust cloud and AI backlog growth that underscores a promising long-term narrative for Oracle.

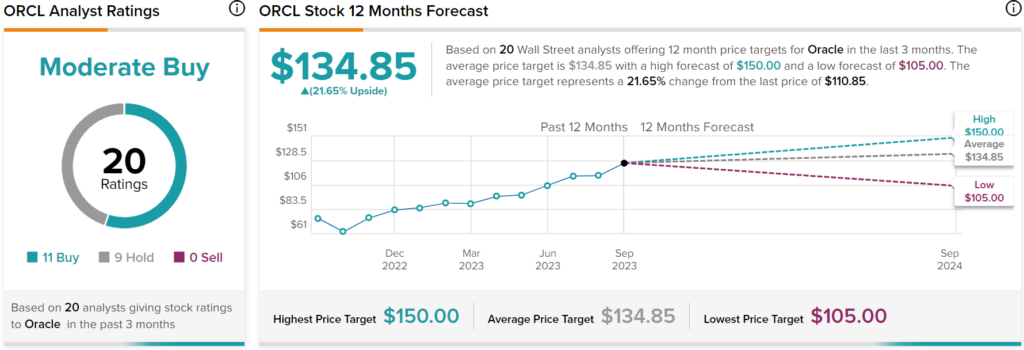

Is Oracle a Buy, Sell, or Hold?

Overall, Wall Street has a Moderate Buy consensus rating on ORCL stock with a price target of $134.85 per share. This implies 21.65% upside potential, as indicated by the graphic above.