U.S. chipmaker ON Semiconductor (ON) missed Wall Street estimates for quarterly earnings as it grapples with the financial fallout of the fast-spreading coronavirus pandemic.

Diluted earnings per share in the first quarter plunged 76% to $0.10 year-on-year, missing analysts’ estimates by $0.05. Revenue dropped 8% to $1.28 billion, which came in $9.2 million below market expectations.

“Our first quarter revenue and margins were significantly impacted by the slowdown in global macroeconomic activity, supply constraints and resulting underutilization due to government mandated lockdowns in many parts of the world aimed at containing the spread of COVID-19,” said Keith Jackson, President and CEO of ON Semiconductor. “While current conditions are causing short-term dislocations, our long-term goals and strategy remain unchanged.”

Jackson added that the company is taking both structural and tactical measures to adjust its business to current conditions and to “drive long-term growth in profitability and free cash flow”.

Looking ahead the chipmaker provided guidance for the second quarter with revenues to fall in the range of $1.10 billion to $1.26 billion. Gross margin is expected to be in the range of 29% to 31%.

“Our customers are placing orders in expectation of recovery in the second half of current year, and we are well positioned to show accelerated progress towards our target financial model as global macroeconomic environment recovers,” Jackson said.

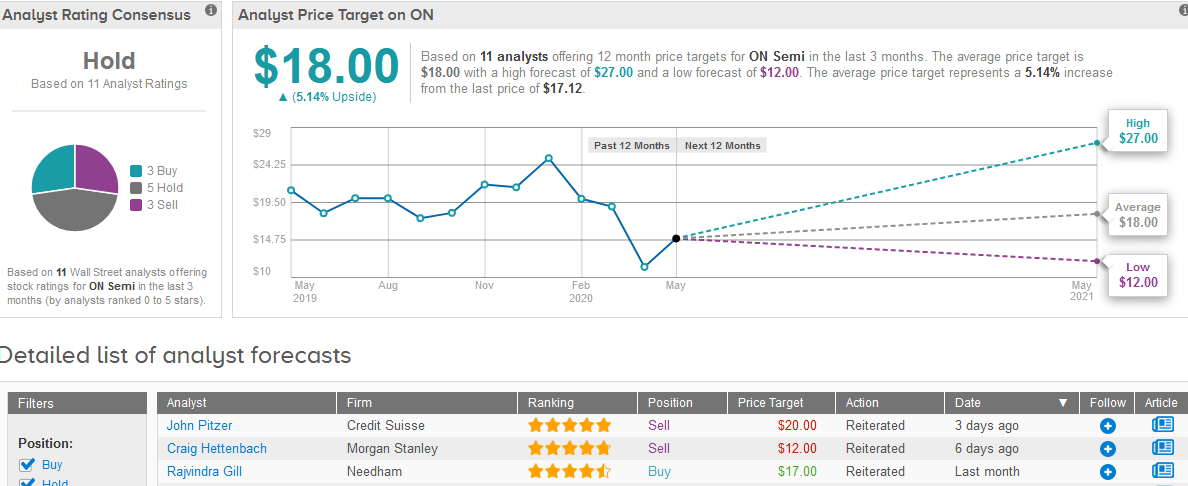

Shares in ON Semiconductor, which nosedived as much as 66% this year, rose 7% to close at $17.12 on Friday.

Five-star analyst John Pitzer at Credit Suisse maintained a Sell rating on the stock with a $20 price target, citing COVID-19 challenges.

“The question we continue to have for ON is whether or not the Company can execute on both revenue growth and margin expansion in the long-term, particularly as the COVID-19 and US/China trade tension risks continue,” Pitzer said in a note to investors. “While the Semi Cycle is in the midst of the bottoming process, and the typical “playbook” would advocate owning ON, we prefer other stocks in our universe, with cheaper valuation and fewer fundamental headwinds.”

Overall, the consensus of Wall Street analysts is more sidelined on the stock with 5 Holds, 3 Sells and 3 Buys. The $18 average price target provide investors with a mere 5% upside potential in the shares in the coming 12 months. (See ON Semiconductor stock analysis on TipRanks).

Related News:

AstraZeneca-Merck Ovarian Cancer Treatment Gets FDA Approval

Eli Lilly Wins FDA Approval For Retevmo Lung, Thyroid Cancer Treatment

Tesla’s Elon Musk Takes Legal Action to Fight Reopening of California Car Plant