Bull markets are often built on themes, and it’s clear which one has been driving the current one’s gains. It’s all about AI, of course, with the ongoing bull market kicking off toward the end of 2022, fueled by the launch of OpenAI’s ChatGPT and the development of GenAI models.

AI has captured investors’ imaginations – and for good reason. The tech is transforming our lives in numerous ways, shaping not only our digital habits but also healthcare, the workplace, entertainment, education, finance, and much more.

The enthusiasm for all things AI has also resulted in some huge gains for companies operating in the space. However, some are better positioned to benefit than others. With this in mind, Morgan Stanley analyst Joseph Moore has been assessing the prospects of two AI giants, semiconductor firms Nvidia (NASDAQ:NVDA) and Micron (NASDAQ:MU), and sees one as the superior name to lean into right now. Let’s dive in.

Nvidia

Any discussion of AI and the name Nvidia naturally pops up. The Jensen Huang-led semi firm has taken the AI opportunity by the horns and has become synonymous with the tech. So much so, that for a period last year it became the world’s most valuable company, a title that in recent years has only been shared between tech behemoths Apple and Microsoft.

Nvidia got its start focusing on the gaming industry, as the maker of GPUs tailored for the sector. That was the main breadwinner for many years before the company started branching out in other directions, in the process pivoting heavily toward the data center segment. Now it accounts for the majority of revenues, and its success is built on the simple fact Nvidia makes the best AI chips on the market. In fact, it dominates the segment to such an extent, that it commands more than an 80% share of the AI chip industry.

The growth has been evident in a series of estimate-trouncing quarterly results that at first shook Wall Street but have now become almost par for the course. In the most recent readout, for the October quarter (FQ3), the semi giant notched impressive year-over-year revenue growth of 93.6%, setting a new record at $35.08 billion, and beating analyst expectations by $1.95 billion. As has become customary, its data center segment led the charge with $30.8 billion in revenue, amounting to a 112% increase vs. the previous year. Meanwhile, adj. EPS came in at $0.81, topping the consensus estimate by $0.06. Looking ahead to the January quarter (FQ4), the company is forecasting revenue of $37.5 billion, with a 2% margin of error, outpacing Wall Street’s projection of $37.1 billion.

More recently, this week Nvidia presented its latest developments at the CES tech show, providing updates on its GPU lineup and other product introductions.

Morgan Stanley analyst Moore was there to get the lowdown and thinks some investor patience will be rewarded later in the year.

“What ultimately makes or breaks the investment thesis at this stage is still the trajectory of the datacenter business, where management is clearly still excited about the Blackwell ramp but nothing we have not heard coming into the event,” the 5-star analyst said. “It’s our sense that Hopper is a little slow but Blackwell supply is ahead of expectations overall, so while we have a couple of transitional quarters (similar to the last two, good but unspectacular), we would stay the course – we see a very strong 2h25 as Blackwell becomes the driving force for revenue growth and NVDA takes share from ASICS in CY25.”

These comments underpin Moore’s Overweight (i.e., Buy) rating on NVDA, while his $166 price target factors in a 12-month gain of 18.5%. (To watch Moore’s track record, click here)

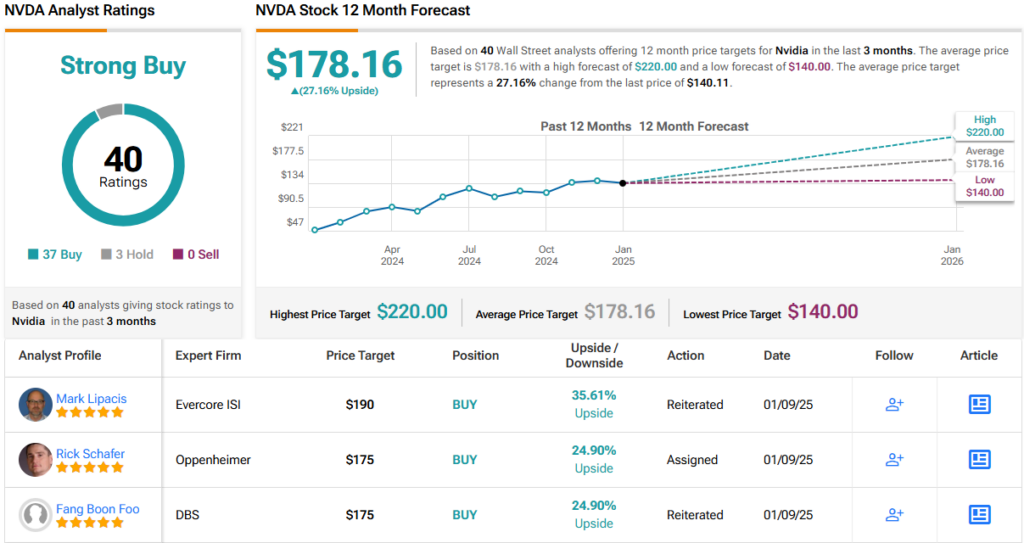

There’s widespread agreement regarding NVDA on Wall Street. The stock claims a Strong Buy consensus rating, based on a mix of 37 Buy recommendations and just 3 Holds. The average target is more bullish than Moore will permit; at $178.16, the figure makes room for one-year returns of 27%. (See Nvidia stock forecast)

Micron

The next AI stock we’ll look at might not have the same star power as Nvidia, but it’s no minnow either. With a market cap of $110.7 billion, Micron is one of the world’s leading producers of memory and storage solutions, with products ranging from DRAM and NAND flash to SSDs and other cutting-edge tech. Micron plays an important role in powering the devices and applications we rely on daily, from smartphones and laptops to data centers and cloud computing platforms.

Micron also stands to gain significantly from the adoption of AI. AI-driven applications, such as large language models, autonomous systems, and advanced analytics, require immense computational power and memory bandwidth. Micron’s high-performance memory solutions are perfectly suited to meet these demanding requirements, leaving the company poised to make the most of the AI opportunity.

That said, while there was plenty of growth on tap in Micron’s latest quarterly readout, there was a spanner in the works that sent shares tumbling in the aftermath.

In the November quarter (F1Q), Micron reported an 84% year-over-year surge in revenue to a record $8.71 billion, aligning with Street expectations. Data center revenue was a standout, soaring by 400% compared to the same period last year, reaching an all-time high and accounting for more than half of total revenue for the first time. On the earnings front, adjusted EPS of $1.79 slightly surpassed analysts’ estimate of $1.77.

Despite these strong figures, investors were concerned about the outlook for the February quarter, which presented a significant disappointment. Micron projected revenue between $7.7 billion and $8.1 billion, with adjusted EPS ranging from $1.33 to $1.53. Both forecasts, at their midpoints, fell well short of Wall Street’s expectations of $8.99 billion in revenue and $1.92 in EPS, raising concerns among analysts and investors about near-term challenges.

Morgan Stanley’s Joseph Moore thinks Micron has tailwinds pushing it ahead but refrains from getting on board right now. Explaining his stance, the analyst writes: “We remain somewhat torn, as our old-school DRAM view is that valuation is too high vs. long-term cash-generation potential – but the stock has clearly rerated around AI enthusiasm, and with the ramps of HBM3e from low levels, low-power DRAM for AI racks, and high-capacity DRAM for servers all contributing billions of incremental revenue the AI narrative remains strong. Our Equal-weight (i.e., Neutral) view reflects that ambiguity, but nearer term we think that the stock can continue to recover lost ground.”

Maybe so, but that Equal-weight rating is accompanied by a $98 price target that implies shares will remain rangebound for the time being.

Moore, however, is amongst a minority on Wall Street. The analyst consensus views Micron stock as a Strong Buy, a rating based on 20 Buy recommendations and just 2 Holds. Going by the $136.43 average target, a year from now, shares will be changing hands for a 37% premium. (See Micron stock forecast)

So with the facts in, it’s clear that Morgan Stanley analyst Joseph Moore rates Nvidia as the superior AI stock right now, a better buy than Micron and a solid choice for investors, even after its remarkable surge.

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.