With the earnings season now underway, we’ll soon find out how publicly traded companies finished 2024. So far, analysts have set a high bar, projecting year-over-year growth of 11% or more. If achieved, this would make Q4 2024 the strongest quarter for earnings growth since 2021.

Against that background, we can look at one of the driving themes behind the success of the past few years – artificial intelligence (AI). AI hasn’t just grabbed the headlines and the hype, it has also provided a solid technological base for a fundamental change across a wide array of industries, from the digital world to healthcare to finance to education to entertainment. No matter where you look these days, AI is there.

This wave of innovation hasn’t gone unnoticed by market analysts. Many are keeping a close eye on AI stocks, seeking insights into what lies ahead for investors. Among them is Cowen analyst Joshua Buchalter, who has highlighted two AI giants that deserve particular attention as this earnings season unfolds.

Nvidia (NASDAQ:NVDA) and Advanced Micro Devices (NASDAQ:AMD), Buchalter’s top picks, are key players in the semiconductor space and integral to the AI revolution. Both companies are known for their high-end, AI-capable processors. Nvidia has been the industry leader for several years now, while AMD is making a concerted bid to expand its market share.

As both companies approach their upcoming earnings reports, Buchalter’s analysis sheds light on what investors can expect, focusing on their growth trajectories and competitive positioning. Let’s take a closer look.

Nvidia

First up is Nvidia, the undisputed heavyweight of the semiconductor industry, with a $3.37 trillion market cap that crowns it as Wall Street’s second-most valuable player, just behind Apple. Nvidia has reached that dizzying height after an astounding 450% share price gain over the past three years – a period that coincides with the AI boom.

The company built its reputation on high-speed processors, the GPUs that became so popular in the gaming industry – but those chips also proved adaptable to a wide range of other high-end computing applications, including high-speed computing, data center server stacks, and AI, particularly generative AI. Today, the company’s data center business segment, which is closely tied to AI, accounts for the bulk of Nvidia’s revenues, and the company commands 80% or more of the AI chip market.

Nvidia continues to benefit from continued demand for both its latest Blackwell series accelerators and its existing Hopper series. The Blackwell chips were announced last March but faced delays in production and delivery. Nvidia has begun to ship out Blackwell sample packs, and the company states that demand for the new chips is strong.

Looking ahead, Nvidia is expected to release its fiscal 4Q25 results at the end of next month, with Wall Street anticipating ~$38 billion in revenue and $0.85 in EPS. If these forecasts hold, they’ll mark an 8.4% increase in revenue and a 5% climb in EPS from the $35.08 billion and $0.81 recorded in fiscal 3Q25.

Turning to the Cowen view, we find analyst Buchalter is upbeat on Nvidia, citing the company’s consistent solid earnings and the high demand for its product lines.

“[We] anticipate a solid print & guide with a continuation of the company’s recent trend to come in ~$1-2B above consensus on both. Our checks indicate that the Blackwell (largely B200 at this point with GB200 beginning more materially in AprQ/JulQ) ramp is progressing well, and we are observing some suppliers shifting allocation from Hopper-based platforms to Blackwell (indicating the health of the ramp and demand). With Blackwell demand still well in excess of supply, and the supply chain not yet shifted to Blackwell Ultra, we view NVIDIA revenue as largely on cruise control for F1H26,” Buchalter opined.

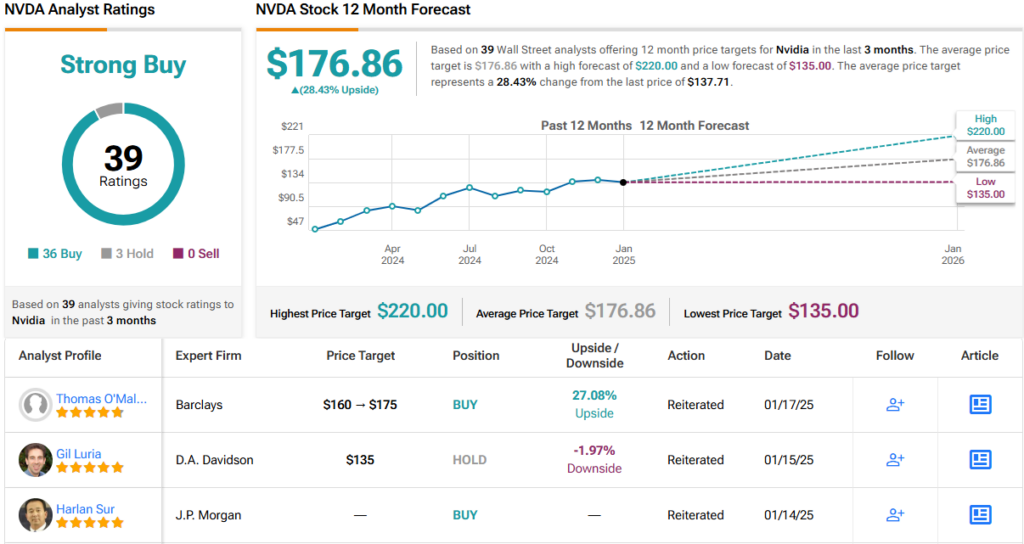

To this end, Buchalter rates Nvidia stock as a Buy, designates it as a Top Pick, and sets a $175 price target, implying a potential one-year upside of 27%. (To watch Buchalter’s track record, click here)

Overall, Nvidia has picked up 39 analyst reviews, with a breakdown of 36 Buys and 3 Holds to give the stock a Strong Buy consensus rating. The shares are currently priced at $137.71 and their $176.86 average target price points toward a 28% upside in the next 12 months. (See NVDA stock forecast)

Advanced Micro Devices

The second stock we’ll look at, AMD, may not be in Nvidia’s league, but it is a solid operator in its own right. AMD has a strong reputation in the chip industry and, over the past year, has been making a concerted effort to erode Nvidia’s market share. The company’s challenge is built on its own lineup of high-quality chipsets, particularly its high-end PC processors and AI-capable accelerator chips.

Earlier this month, AMD announced several new products in line with this challenge. These include several new Ryzen chips for both business and consumer PCs – all of which are designed to power next-generation AI applications. The new chips include the AMD Ryzen AI Max, AMD Ryzen AI 300 Series and AMD Ryzen 200 Series processors on the consumer side, and the AMD Ryzen AI Max PRO, AMD Ryzen AI 300 PRO and AMD Ryzen 200 PRO Series on the commercial side. In addition, the company also announced a stronger partnership with Dell. The Dell agreement will see the PC maker put AMD Ryzen AI PRO processors into new Dell Pro computers. This will mark the first shipment of Dell’s commercial PCs with AMD Ryzen AI PRO processors.

These announcements mark an important expansion in AMD’s push to expand its AI offerings. The company already has support from important customers such as Microsoft, Meta, and Oracle, all of which are major enterprise consumers of high-end AI processors.

We should note that AMD has experienced sequential gains in both revenues and earnings over the last two quarterly results. In late October, when the company released its third-quarter 2024 results, the top line reached $6.82 billion, marking an 18% year-over-year increase and surpassing the forecast by $110 million. At the bottom line, the non-GAAP EPS of 92 cents was in line with expectations.

Looking ahead, AMD is set to release its fourth-quarter 2024 results on Tuesday, February 4. Wall Street expects $7.53 billion in revenue and an EPS of $1.09, reflecting a sequential 10% increase in revenue and an 18% rise in EPS compared to Q3 2024.

Even though AMD’s results have been ticking upwards, and its product lines are finding solid demand, the company’s stock price has been falling. AMD shares are down 23% in the last 12 months.

That, however, leads Cowen analyst Buchalter to see AMD as an opportunity. Noting that the stock has underperformed, the analyst also cites AMD’s success in expanding its market share.

“We expect a sold [sic] in-line print/guide against a very high bar that’s being set by the fervent backdrop surrounding AI and the ‘insatiable’ demand for compute and recent momentum in the ASIC space. The stock has underperformed over the last three months as AMD’s progress has been steady, but not necessarily step-function like its AI-compute peers. Our checks point to continued positive demand for MI300/325 products at AMD’s lead-customers. That said, a more seasonal gen-purpose Server CPU and stubborn softness in Embedded (and typically weak 1Q25 seasonality in Client) are partially muting AMD’s ongoing share gains (eg. AMD’s significant enterprise PC win with Dell). As a result, we take our above-Street estimates down slightly while maintaining our AI accelerator estimate of $5B/$10B/$15B for 2024/2025/2026,” Buchalter stated.

These comments back up Buchalter’s Buy rating on AMD, which he complements with a $150 price target that suggests a share appreciation of 23.5% on the one-year horizon.

All in all, AMD’s consensus rating is a Moderate Buy, based on 32 recent analyst reviews that include 21 Buys, 10 Holds, and a lone Sell. The stock is trading for $121.46 currently, and shows a ~42% one-year upside based on the average price target of $172.24. (See AMD stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.