EV automaker Nio (NIO) has seen its shares fall by over 10% since publishing its Q4 earnings report late last week, despite the company reporting a robust increase in vehicle deliveries and revenue for both the fourth quarter and the full year of 2024. The company delivered 72,689 vehicles in the fourth quarter and 221,970 vehicles for the year, representing a notable increase from previous numbers. However, NIO also reported a widening net loss and provided Q1 guidance that fell below expectations. Analysts hold a mixed outlook on NIO’s future, with projections of positive earnings momentum starting mid-Q2 2025.

Top and Bottom-line Misses

NIO is a Chinese company that specializes in the design, development, manufacture, and sale of electric vehicles, including SUVs and sedans. Beyond vehicles, NIO offers comprehensive power solutions, including home charging, battery swapping, and mobile charging services, all supported by a network of public chargers accessible via its app. The company provides vehicle maintenance, repair services, insurance options, and financial services, including auto financing and leasing.

The company reported a Q4 revenue of $2.7 billion, which fell short of analyst expectations by $70 million. The company delivered 72,689 vehicles in the quarter, representing a 45.2% increase from the previous year, which contributed to vehicle sales revenue of $2.39 billion, a 10.1% year-over-year increase. Other sales increased by 30.2%, resulting in a gross profit of $316.3 million, a 75.5% improvement due to decreased costs. The gross margin improved to 11.7% from 7.5%, and the vehicle margin rose to 13.1%. R&D costs decreased by 10.9%, and SG&A expenses dropped by 19.4%, resulting in a reduction in the loss from operations to $826.5 million and non-GAAP EPS of -$0.43, which missed consensus estimates by $0.10.

As the year drew to a close, NIO had $5.7 billion in cash and $1.57 billion in long-term debt. For Q1 2025, NIO expects to deliver 41,000-43,000 vehicles, with projected revenue between $1.69 billion and $1.76 billion, short of the consensus estimate of $2.31 billion.

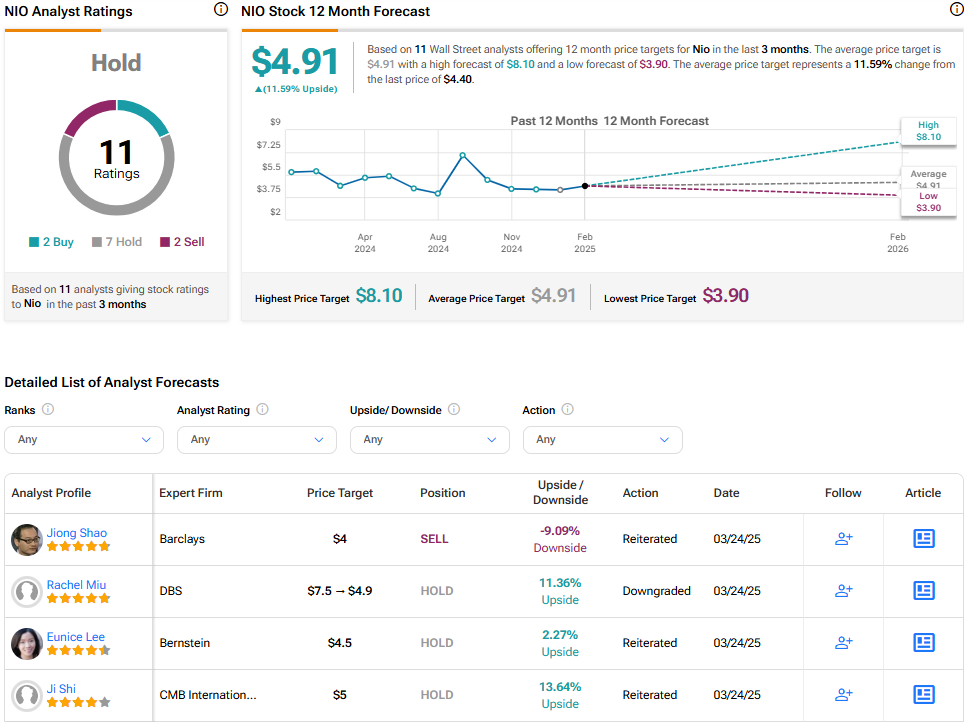

Analysts Hold Mixed Outlook

Analysts have a mixed outlook on the company’s prospects over the next 12 months. Ji Shi at CMB International Securities reiterated a Hold rating on NIO stock with a price target of $5.00, citing financial and operational challenges facing the company. While Nio’s vehicle gross profit margin met expectations for Q4, Shi noted that revenue underperformed due to lower-than-average selling prices, resulting in a wider-than-anticipated net loss due to high administrative costs. Furthermore, the cost reduction potential is limited by Nio’s substantial investments in projects such as in-house chip and battery swap development. Forecasts for 2025, even with optimistic sales volumes and gross profit margins, suggest continued net losses.

Meanwhile, Citi’s Jeff Chung reduced NIO’s price target to $8.10 (from $8.90) while maintaining a Buy rating. Chung cites an expected decline in Q1 vehicle margins due to a seasonal low in car sales and lukewarm demand for Nio vehicles before model upgrades in Q2. He anticipates earnings improvements starting in mid-Q2, driven by extensive model launches and improved margins resulting from better scale effects.

Nio is rated a Hold overall based on the recent recommendations of 11 analysts. The average price target for NIO stock is $4.91, which represents a potential upside of 12.10% from current levels.

Questions or Comments about the article? Write to editor@tipranks.com