Newell Brands (NASDAQ:NWL) shares slumped in the early session today after the global consumer goods major’s fourth-quarter sales declined by 9.1% year-over-year to $2.1 billion. Still, the figure came in better than expectations by $30 million. Further, EPS of $0.22 landed ahead of estimates by $0.05.

During the quarter, core sales declined by 9.3%. In the Home & Commercial Solutions segment, core sales declined across the company’s Kitchen, Home Fragrance, and Commercial businesses. Similarly, lower core sales in the Writing and Baby businesses impacted sales in the Learning & Development vertical. Moreover, net sales in the Outdoor & Recreation segment declined by double-digits.

While the macro environment remains challenging, Newell is focusing on brand building, efficiency gains, and driving market leadership in its largest and most profitable markets. This focus on productivity, rightsizing inventory, and lowering SKU (stock keeping unit) count helped the company drive cash flow gains and expand its gross margin by 360 basis points to 29.9%. Notably, Newell pared down its debt by $500 million to $4.9 billion during the year.

For Fiscal Year 2024, Newell anticipates a revenue decline of 8% to 5%. EPS for the year is seen landing between $0.52 and $0.62. For the upcoming quarter, the company foresees EPS in the range of -$0.09 to -$0.05. Net sales are seen declining by 10% to 8%.

Is NWL Stock a Good Buy?

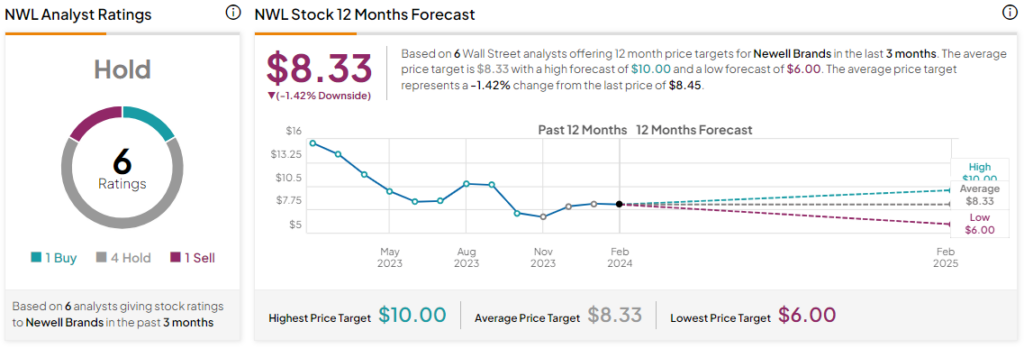

Overall, the Street has a Hold consensus rating on Newell Brands. Following a nearly 27% jump in the company’s share price over the past three months, the average NWL price target of $8.33 points to a potential downside of 1.4% in the stock.

Read full Disclosure