Shares of New Oriental Education dropped 7.5% on Jan. 22 as its 3Q revenue guidance failed to impress investors. Meanwhile, the China-based educational services provider reported better-than-expected 2Q results.

Maximize Your Portfolio with Data Driven Insights:

- Leverage the power of TipRanks' Smart Score, a data-driven tool to help you uncover top performing stocks and make informed investment decisions.

- Monitor your stock picks and compare them to top Wall Street Analysts' recommendations with Your Smart Portfolio

New Oriental Education (EDU) expects to report sales of between $1.099 billion and $1.145 billion in 3Q, representing year-over-year growth of 19% to 24%. The mid-point sales outlook comes in at $1.122 billion which is below the Street’s expectations of $1.14 billion.

Coming back to the 2Q performance, New Oriental Education’s net revenue of $887.7 million increased 13.1% year-over-year and beat analysts’ estimates of $885.6 billion. Adjusted earnings per ADS (American Depository Share) grew 19.4% to $0.43 and exceeded the consensus estimate of $0.34. (See EDU stock analysis on TipRanks)

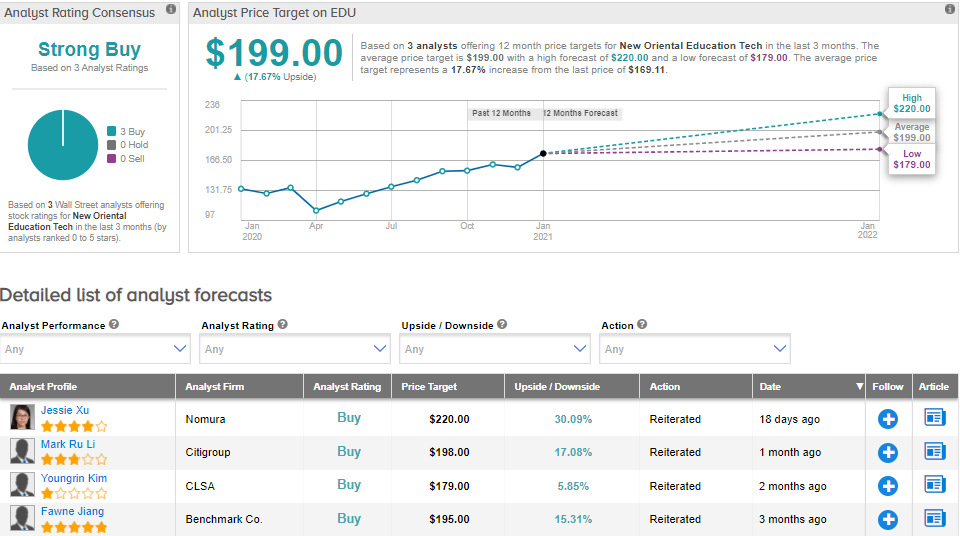

Last month, Citigroup analyst Mark Ru Li reiterated a Buy rating on the stock with a price target of $198 (17.1% upside potential) after conducting industry checks and hosting a call with management. Li is optimistic about the recovery in the company’s offline after-school tutorial segment. The analyst also expects New Oriental Education to gain market share from its online-merge-offline model.

Overall, the rest of the Street is bullish on the stock. The Strong Buy analyst consensus shows unanimous 3 Buys. The average price target of $199 implies upside potential of about 17.7% to current levels. That’s after shares already gained 27% over the past year.

Related News:

Kansas City Sees Double-Digit Sales Growth In 2021

Ally Financial Crushes 4Q Estimates Driven By Lower Provisions

IBM’s 4Q Revenues Of $20.4B Disappoint; Shares Fall 7.3% After Hours