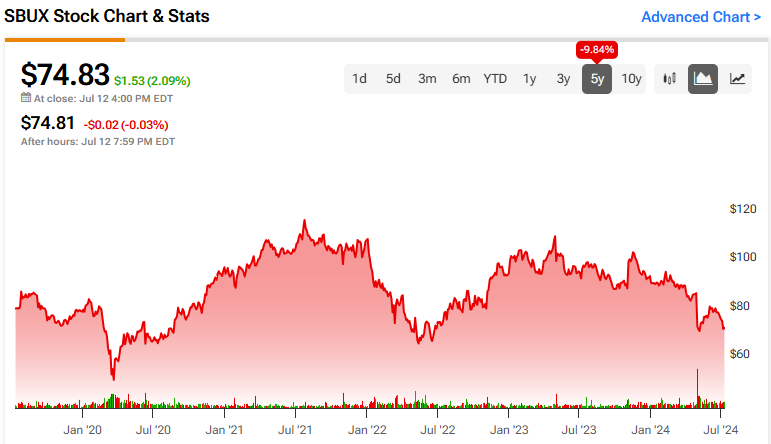

Starbucks stock (NASDAQ:SBUX) has sustained a prolonged decline in recent years, currently trading near its 52-week low. This marks a significant underperformance for the Seattle-based coffee chain, as indices have continued to climb to new highs by the month. The current sell-off is driven by investor worries that the brand is losing its appeal among consumers, as evidenced by declining foot traffic and a recent slump in revenue growth. Despite this narrative, Starbucks stock seems too cheaply priced to continue to ignore. Accordingly, I am bullish on the stock.

Is Starbucks Losing Its Brand Appeal?

Starbucks’ bearish sentiment appears to be driven by increasing investor concerns regarding the brand’s waning appeal among consumers. This narrative has been building for months. Toward the end of 2023, Starbucks faced significant controversy, as employees, former baristas, and Palestinian advocacy groups across the nation united in boycotts. These issues have now been exacerbated by a tangible trend of declining sales growth. To illustrate, Starbucks’ revenue growth in recent quarters has been as follows:

- FQ2-2023: 13.2%

- FQ3-2023: 12.5%

- FQ4-2023: 11.4%

- FQ1-2024: 8.2%

- FQ2-2024: -1.8%

The current trend of falling revenue is undeniable, causing growing concern among investors. Historically, Starbucks has been a strong performer, especially during periods when the consumer discretionary sector is doing well. The slowdown in revenue growth suggests that the company might be struggling to attract and retain customers at the same rate as before, raising red flags about its future profitability and market position.

Starbucks’ latest FQ2 results provided further insights into the ongoing issues. In North America, revenues came in flat at $6.4 billion, as the 5% net new company-operated store growth was offset by a 3% decline in comparable store sales. This decline was, in turn, driven by a 7% drop in transactions that offset the 4% increase in the average ticket (i.e., pricing).

Note that this doesn’t seem to be a domestic trend but one that has spread internationally. In China, for instance, revenues declined by 3% due to an 11% decrease in comparable store sales. Similar to the U.S., this decline, in turn, included 8% and 4% drops in average tickets and transactions, respectively, despite a 14% increase in net new store growth. So, we see Starbucks opening new stores and raising prices, trying to somewhat sustain revenues, yet foot traffic and the average number of items purchased decline. This is certainly a very concerning trend.

How’s Starbucks’ Outlook Looking, Moving Forward?

Despite these challenges, Starbucks’ management believes it can respond to them from a position of enduring strength. They intend to drive compelling product innovation, build great stores, and maintain coffee leadership. In the meantime, the company wants to improve customer experience during peak times. Certain stores have already started utilizing the Siren Craft System to optimize store operations, which is expected to increase throughput and improve product availability.

In any case, it could be some time before Starbucks regains some momentum, as the company’s full-year guidance continues to predict single-digit comparable sales decline in both the U.S. and China (see below). New store openings, strong margin retention, and modest buybacks are expected to help EPS remain flat or record a slight single-digit increase. Consensus estimates seem to agree with this outlook, projecting EPS growth of just about 1% for the full year to $3.58.

Starbucks Valuation Is Too Cheap to Ignore for Bullish Investors

From this point, it’s all about whether you believe in Starbucks’ bullish case or not. If you think the current decline in foot traffic and transaction volumes will persist, Starbucks stock continues to be overvalued at approximately 20 times this year’s projected EPS. Conversely, if you believe this downturn is temporary and that consumer appeal in Starbucks will rebound, the stock is clearly undervalued.

Wall Street analysts seem to favor the latter view, expecting annual EPS growth to return in the double-digits beginning in FY2025. In that case, Starbucks stock seems to be offering a compelling opportunity near its 52-week low.

Is SBUX Stock a Buy, According to Analysts?

Wall Street seems to agree that the stock is attractively priced against consensus estimates. Starbucks has a Moderate Buy consensus rating based on nine Buys and 18 Holds assigned in the past three months. At $88.63, the average SBUX stock prediction implies 18% upside potential.

If you’re unsure which analyst you should follow if you want to buy and sell SBUX stock, the most accurate analyst covering the stock (on a one-year timeframe) is John Ivankoe from JPMorgan (NYSE:JPM), with an average return of 14.75% per rating and a 64% success rate. Click on the image below to learn more.

The Takeaway

Despite recent challenges, including falling foot traffic and revenue growth, Starbucks’ current valuation appears too cheap for bullish investors to ignore. If you believe the downturn is temporary and consumer appeal will rebound, Starbucks stock presents a compelling opportunity at its current lows. This narrative is further supported by optimism among Wall Street analysts, who project outsized EPS growth starting in FY2025.