Mullen Group Ltd. posted its first-quarter financial results on April 21 after market close. The Canadian supplier of trucking and logistics services revenue fell, but profit increased.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

Mullen Group Ltd. (MTL) total revenue came in at C$290.5 million for the quarter ended March 31, 2021, a decrease of 8.7% from C$318.2 million in 2020 due to the impact of the COVID-19 pandemic.

However, net income increased from C$4.7 million (C$0.04 per share) to C$13.0 million (C$0.13 per share). On an adjusted basis, Mullen earned C$0.12 per share in 1Q 2021, up 33% from C$0.09 last year. Analysts expected adjusted EPS of C$0.09.

Mullen Group’s Chairman and CEO Murray K. Mullen said, “I am both excited and positive about the future of our company for a couple of reasons. It is only a matter of time before a sharp recovery in the Canadian economy takes place because the necessary conditions, including significant capital resources and consumer pent-up demand, are waiting for COVID-19 to be brought under control. And, of course, the opportunities the new acquisitions bring to our company. In addition, I am of the view that the logistics and freight industry are ripe for further consolidation which we will be well-positioned to capture, particularly ‘tuck-in’ purchases.”

Since the start of 2021, Mullen has announced two significant deals that will accelerate the company’s growth. In April, the company bought Bandstra Transportation Group, while APPS Transport Group’s acquisition is expecting to close in the second quarter. (See Mullen Group stock analysis on TipRanks)

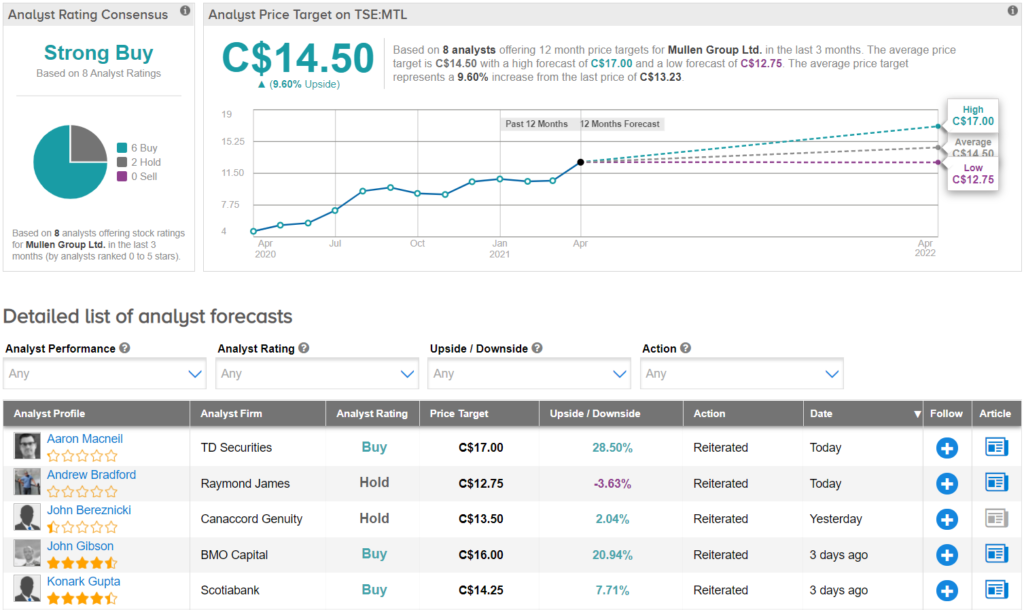

Three days ago, BMO Capital analyst John Gibson maintained a Buy rating on the stock and raised his price target from C$15.00 to C$16.00 (21% upside potential). In a note to investors, Gibson said he appreciates Mullen’s decision to acquire APPS Transport Group. It is part of the company’s vision to expand its network of LTL services in small communities and increase its warehousing capacity in larger centers.

Overall, the consensus on the Street is that Mullen Group is a Strong Buy based on 6 Buys and 2 Holds. The average analyst price target of C$14.50 implies an upside potential of about 9.6% to current levels.

Related News:

Canadian Pacific Misses On Revenue In 1Q

Quisitive Technology Posts 169% Revenue Growth For Full Year 2020

Canopy Growth Partners With Southern Glazer’s Wine & Spirit To Distribute CBD Beverages; Shares Jump 4.5%