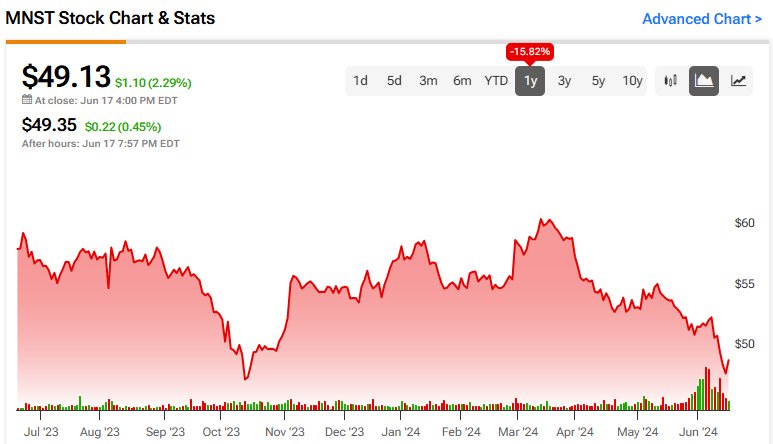

Monster Beverage (NASDAQ:MNST) stock is now trading near its 52-week lows, offering a compelling buying opportunity for investors. The energy drink giant has historically enjoyed premium valuation multiples due to its consistent growth, excellent profitability, and strong balance sheet. The recent price slump stems from concerns regarding rising competition and an industry slowdown, but Monster’s latest results were once again robust. Thus, I am bullish on the stock.

Understanding Monster Stock’s Valuation

To support my argument that Monster Beverage offers a compelling investment opportunity near its 52-week lows, it is essential to provide context to better understand the stock’s valuation. Basically, Monster stock has historically commanded a high valuation due to its growth story, which stands as one of the most impressive among publicly traded companies. Starting at $28.8 million in 1994, sales have not only grown every single year, but last year’s sales of $7.14 billion imply an insane 248-fold increase since then.

Now, combine this unbelievable growth trajectory with Monster managing to achieve incredible margins due to smart distribution agreements over the years, and you get an even more wonderful increase in net income. From losing $1.4 million in 1994 to becoming profitable in 1997 with a net income of $351,700 to posting $1.63 billion in profits last year, Monster’s bottom-line growth is also one for the history books.

Because of this extraordinary top-and-bottom-line growth trajectory, Monster shares have registered unreal returns over the years. Since 1999, which is the year from which I can benchmark all four stocks I am about to mention, Monster’s stock price has achieved a compound annual growth rate (CAGR) of 31%. This figure becomes even more impressive, given that shares are now close to their lowest levels in the past year.

Throughout this period, Monster has consistently outpaced even some of the most successful tech giants like Apple (NASDAQ:AAPL) and Microsoft (NASDAQ:MSFT), which have enjoyed CAGRs of 29.6% and 17.5% in total returns (including dividends), respectively. As far as I can see, only Nvidia (NASDAQ:NVDA) has managed to outperform Monster, registering a total-return CAGR of 37.8% over the same timeframe after its recent surge.

In short, Monster has made many people rich over the years, and its sustained, robust growth continues to attract investors willing to pay a premium for a piece of the company. In fact, over the past decade, Monster’s stock has consistently traded at a forward P/E ratio ranging from 25x to 40x, reflecting its lasting growth trajectory.

Today, the stock trades at a forward P/E of 26.9x, positioning it attractively within its historical valuation range. Coupled with the company’s growth prospects remaining strong, it’s pretty clear to me that the stock forms a compelling opportunity at its current levels.

Competition Worries Remain, But Monster’s Growth Remains Strong

Touching on the bearish case, Monster’s investment prospects have recently been hindered by increasing concerns over competition and the company’s decelerating growth. Particularly concerning for investors is the meteoric rise of Celsius Holdings (NASDAQ:CELH), which substantially threatens Monster’s market share. Celsius’ “functional beverage” products, including caffeine and other stimulants, directly compete with Monster and Red Bull and even target non-caffeinated options, advancing into the soda market.

To underscore Celsius’s explosive growth, its sales surged by 74%, 140%, 108%, and 102% in 2020, 2021, 2022, and 2023, respectively. Last year, its sales totaled $1.32 billion, a figure that is 18% of Monster’s total revenues. At this rate, Celsius should approach Monster’s sales figures in the span of a few years, which explains the ongoing worries Monster investors have regarding the company losing some of its current market share.

Additionally, concerns intensified further recently, with Nielsen data indicating a slowdown in Celsius’ growth and price declines for the week ending May 18. This development has also raised valid concerns among investors about Monster’s future growth trajectory. If the fastest-growing player in the space shows signs of slowing down, the same should be expected for a more mature player like Monster.

Nevertheless, Monster’s underlying growth seems robust thus far, suggesting that the ongoing sell-off is an overreaction. In Q1, Monster’s revenues came in at a record $1.90 billion (see below), growing by 11.8% compared to last year. In the meantime, Wall Street expects Monster’s revenues for FY2024 to rise by 10% to $7.85 billion, sustaining its double-digit growth trajectory. Also, its earnings per share (EPS) is expected to grow by 16% to $1.79, which further bolsters my conviction in the stock at its current valuation.

Is MNST Stock a Buy, According to Analysts?

Regarding Wall Street’s view on the stock, Monster Beverage features a Moderate Buy consensus rating based on eight Buys, five Holds, and one Sell assigned in the past three months. At $61.31, the average MNST stock price prediction suggests 24.8% upside potential.

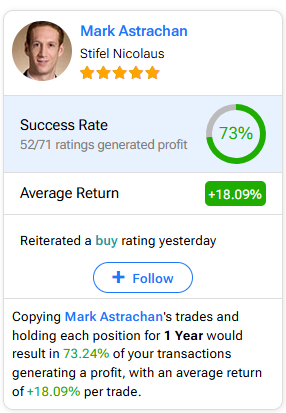

If you’re unsure which analyst you should follow if you want to buy and sell MNST stock, the most profitable analyst covering the stock (on a one-year timeframe) is Mark Astrachan from Stifel Nicolaus, with an average return of 18.09% per rating and a 73% success rate. Click on the image below to learn more.

The Takeaway

To summarize, despite the ongoing concerns, Monster Beverage presents a highly compelling investment case at its current valuation. The company’s consistent track record of strong growth, reaffirmed by its latest quarterly results and optimistic projections from Wall Street, strengthens my confidence in its resilience. Trading near a decade-low valuation level adds additional appeal for long-term investors who had stayed on the sidelines in previous years, citing its premium valuation at the time.