monday.com (MNDY) gained in regular trading hours after it reported a robust third-quarter earnings report. The company’s revenue hit $251 million, marking a 33% year-over-year increase, surpassing analysts’ forecast of $246 million. More exciting for investors, monday.com has surpassed an important milestone—$1 billion in Annual Recurring Revenue (ARR), a feat it achieved just a decade after its inception.

Confident Investing Starts Here:

- Easily unpack a company's performance with TipRanks' new KPI Data for smart investment decisions

- Receive undervalued, market resilient stocks straight to you inbox with TipRanks' Smart Value Newsletter

MNDY Generates Solid Growth in Q3 Earnings

The company’s third-quarter results clearly reflect its growing influence in the work management space. monday.com reported a GAAP operating loss of $27.4 million for Q3, which is slightly wider than last year’s $2.5 million loss. However, when looking at non-GAAP metrics, monday.com posted an operating income of $32.2 million, which was an improvement from $24.1 million in Q3 2023. As monday.com CFO Eliran Glazer noted, “We are very pleased with our results in Q3, with solid revenue growth and profitability, as well as improving retention trends as we continue to expand to larger customers.”

The company’s EPS (Earnings Per Share) story was mixed. The GAAP net loss per share came in at $0.24, a sharp decline from the $0.15 gain in Q3 2023. However, the non-GAAP EPS showed better performance, with a net income of $0.90 per share, up from $0.68 a year ago, beating analysts’ consensus estimate of $0.64. This signals healthier margins in the company’s core operations.

Monday.com Demonstrates Improving Retention Rates

What stands out in the earnings report is monday.com’s continued focus on customer retention, which is a key metric in the Software as a Service (SaaS) industry. The company’s net dollar retention rate (NDR) climbed to an impressive 111%, signaling that customers are not only staying but expanding their investments. Notably, customers with more than $100,000 in ARR had a retention rate of 115%, which showcases the company’s increasing appeal among large enterprises.

The second-largest customer, an international tech giant, more than doubled its seat count from 25,000 to 60,000, a clear indication of the growing confidence in monday.com’s platform. “Reaching $1 billion in ARR marks a major milestone in our journey as a company,” said Roy Mann, co-founder of monday.com, reflecting on the growth.

MNDAY Expands its Leadership Team

monday.com is also making moves to ensure that its growth continues. Recently, the company appointed Adi Dar as Chief Operating Officer. Dar, who brings over 20 years of experience, is expected to play an important role in expanding the company’s reach.

MNDAY Issues Upbeat Guidance

As for the financial outlook, monday.com expects Q4 revenue to range between $260 million to $262 million, continuing its growth momentum for the year. For the full year, the company anticipates revenue growth of 32% year-over-year, projecting total revenue of about $965 million. Non-GAAP operating income for Fiscal year 2024 is expected to hit $121 million to $123 million, with a free cash flow margin of about 30%.

Monday.com Repurchases Shares

As part of its ongoing efforts to enhance shareholder value, monday.com has announced a share repurchase program, signaling confidence in the company’s future. This program authorizes the repurchase of up to $200 million worth of its own stock. This move reflects the company’s belief that its stock is undervalued, providing an opportunity to buy back shares at a potentially attractive price. Share repurchases are a common strategy for returning value to shareholders, as they can increase earnings per share (EPS) by reducing the total number of outstanding shares.

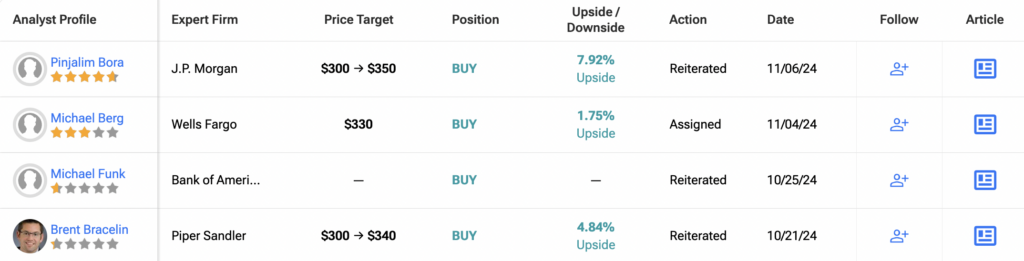

Is MNDY Stock a Good Buy?

Analysts are optimistic about MNDY stock, with a Strong Buy consensus rating based on 14 Buys and four Holds. Over the past year, MNDY has rallied by more than 100%, and the average MNDY price target of $315.44 implies a downside potential of 2.74% from current levels. These analyst ratings are likely to change following MNDY’s results today.