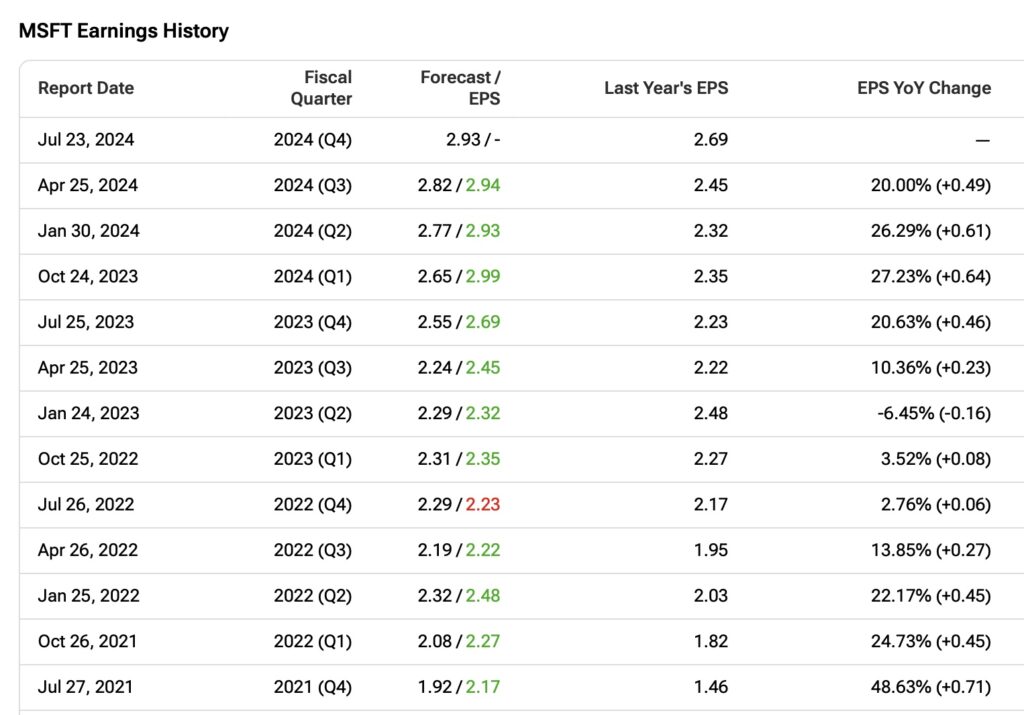

On July 23, the software behemoth Microsoft (MSFT) is expected to report its Fiscal fourth-quarter results. If the big tech company beats Wall Street’s expectations, this will mark the eighth consecutive quarter of surpassing EPS estimates, having missed only once (in Fiscal Q4 2022) in the last five years. I think it’s unlikely we’ll see another miss this quarter, so I believe MSFT stock deserves a bullish stance.

Rather than being a quarter that determines a key turning point for the company’s long-term growth story, I believe investors will primarily focus on the consolidation of AI investments and Microsoft’s trajectory as one of the main drivers of the AI revolution.

All Eyes on AI

Unlike some other tech companies, it’s not within Microsoft’s profile to disclose news or pertinent details on earnings day that deviate from investor expectations, especially given the non-cyclical nature of its software offerings. Analysts expect the company to report revenues of $64.4 billion for the quarter, closely aligned with the high-end guidance of $64.5 billion provided by the company in Fiscal Q3.

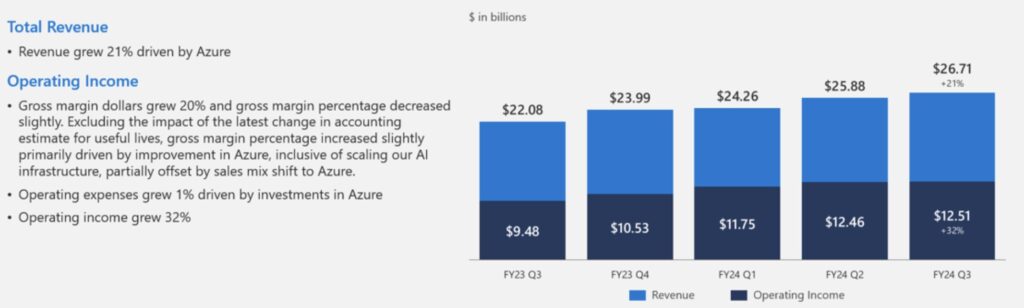

In the previous quarter, Fiscal Q3, Microsoft guided investors to expect another strong performance. The primary segment to monitor is Intelligent Cloud, renowned for its leadership in AI through Azure. This segment is projected to achieve growth between 19% and 20% in Fiscal Q4, factoring in some impact from AI capacity availability.

While this growth forecast isn’t the highest historically for the segment, the more cautious outlook suggests a higher likelihood of meeting expectations. In the last quarter, the segment achieved a 21% revenue increase, with operating income rising by 32% due to Azure’s expansion. In my opinion, this growth trend shows that Microsoft is well-placed in the AI growth story.

According to the Redmond-based company, near-term AI demand is slightly higher than available capacity. This shortfall isn’t attributed to a single component but to the entirety of elements needed to bring capacity online, including land, concrete, energy, and GPUs. As a result, capital expenditures (CapEx) are expected to increase significantly on a sequential basis due to investments in AI.

It will also be interesting to watch the More Personal Computing segment as PC market unit volumes continue at pre-pandemic levels. Microsoft anticipates that there will be a decline in the mid-teens for the Devices segment as the company focuses on higher-margin products rather than volume. In contrast, the Gaming segment is expected to grow. Xbox content and services are projected to rise by the high 50s, driven by approximately 60 points of net impact from the Activision acquisition, despite an anticipated decline in hardware.

What Could Go Wrong with MSFT?

As mentioned earlier, I don’t anticipate anything unusual affecting the market reaction post-Fiscal Q4 earnings. However, this doesn’t discount potential risks that could overshadow MSFT’s performance.

In addition to the risk of reporting numbers closer to the company’s lower-range guidance, which could dampen bullish sentiment, there’s also the potential challenge of increased competition in the AI sector, particularly from OpenAI, which could create headwinds.

Currently, the partnership between Microsoft and OpenAI is a significant strength of the bullish thesis. However, OpenAI has been expanding its reach, such as its recent integration with Apple (AAPL). Microsoft has invested $13 billion in this partnership, with OpenAI utilizing Azure chips for its platform’s training and operation.

As Microsoft starts to directly sell to its enterprise clients, there is now slight competition with OpenAI itself, potentially complicating their partnership. Although this risk can be mitigated by the range of language models being developed, any perception that it affects enterprise deal demand could pose a significant risk.

Microsoft’s Remarkable Stock Performance

Microsoft shares have appreciated approximately 25% this year and 40% over the last 12 months, which is substantial growth for a company known for its steady growth trajectory, historically trading at a P/E ratio multiple of 33x over the past half-decade. Valuation has always been a point of caution with MSFT. However, the current P/E multiple of 39x is seen as justified, given its pivotal role in driving the AI revolution.

To further excite investors, looking at the average returns in July (when Microsoft reports its Fiscal Q4 results) over the past 16 years, the company has returned an average of 3.46%, outperforming the S&P 500’s (SPX) average return of 3.15% over the same period. This highlights not just Microsoft’s historical optimism during Q4 earnings but also positive sentiments in other reporting months. October and April, when Microsoft reports Fiscal Q1 and Q3 earnings, respectively, typically see the company performing best throughout the year, averaging returns of 5% and 4.32%.

Although a blowout earnings report isn’t off the table, I consider it highly unlikely that the company will disappoint investors, given the strong momentum in AI. Indeed, Microsoft’s recent share price increase since June reflects investors’ optimism for another quarterly beat.

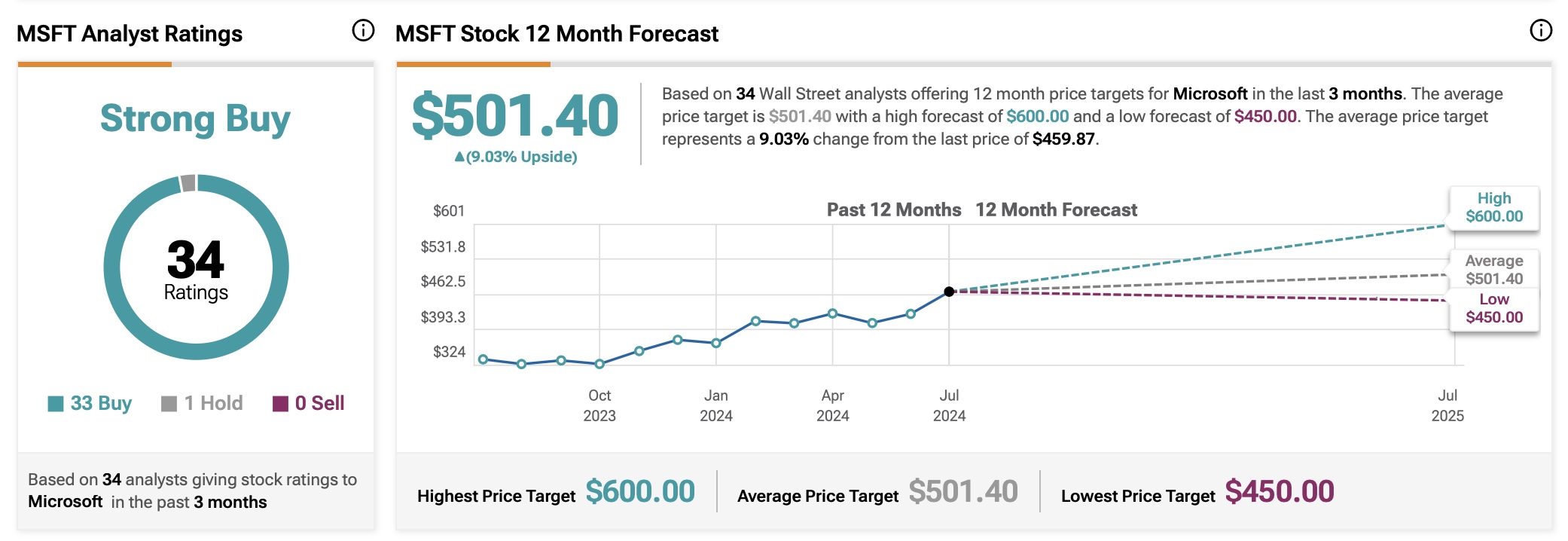

Is MSFT Stock a Buy, According to Analysts?

Reflecting the bullish momentum of MSFT shares, Wall Street consensus strongly favors a “Strong Buy” rating, with only one out of 34 analysts covering the stock having a rating other than “Buy.” The average price target for MSFT stands at $501.40, suggesting an upside potential of 9.03%.

Key Takeaway

All indications suggest another solid earnings beat for Microsoft stock in Fiscal Q4.

Microsoft is well-positioned to continue its growth, driven by strong demand for its AI services and strategic expansion in high-growth markets. Despite short-term pressures on margins and capacity constraints, the company shows the flexibility and financial discipline to adapt to market conditions while maintaining its focus on delivering differentiated value to customers.

Although trading at a historically stretched valuation, I don’t see any immediate risks that could detract from the bullish momentum or jeopardize Microsoft’s Fiscal Q4 performance.