The Magnificent 7 group of stocks again proved their dominance in 2024. With an average gain of 63% in the year, they accounted for more than half of the S&P 500’s total gains. Now, I do believe that all seven tech giants are well-positioned for sustained growth. However, I think Meta Platforms (META) is the most compelling investment case. It combines exceptional revenue growth prospects with a relatively modest valuation. I believe this setup will likely keep producing superior returns for investors, which is why Meta remains my largest position despite last year’s extended share price gains.

Meta Offers the Best Growth-for-Value Setup

To paint a clearer picture, NVIDIA (NVDA) led the Magnificent 7 in revenue growth over the trailing 12 months, with a tremendous 152.44%. Meta followed with an outstanding 23.06%, outpacing Microsoft’s (MSFT) 16.44%, Alphabet’s (GOOGL) 14.38%, Amazon’s (AMZN) 11.93%, Apple’s (AAPL) 2.02%, and Tesla’s (TSLA) 1.28%.

Now, NVIDIA’s growth is, of course, spectacular. However, it’s fair to say that its current levels are going to be unsustainable due to the inevitable stabilization of demand for its AI chips. Further, at about 47 times its FY2025 EPS, I find NVIDIA notably more expensive than Meta, which trades at just 27 times its FY2024 EPS and 24 times its FY2025 EPS. This is because, unlike NVIDIA, Meta is much more likely to maintain its lofty growth levels. In fact, I would argue that Wall Street analysts underestimate Meta’s medium-term growth potential, suggesting that the stock is even more discounted than it appears.

Wall Street Likely Underestimates Meta’s Growth Prospects

The first reason I believe that Wall Street underestimates Meta’s potential is that its top-line growth is currently experiencing an upward trajectory that is likely to endure. After relaxing in Fiscal 2022, revenue growth accelerated to 15.7% in Fiscal 2023, while revenue growth for Fiscal 2024 should be about 20.8%. What makes little sense to me is that Wall Street estimates suggest a slowdown to 14.6% in Fiscal 2025. I find this estimate overly conservative, as several catalysts, such as Meta’s developments in AI, imply that Meta is well positioned to sustain accelerated top-line growth or, at the minimum, maintain similar levels to last year.

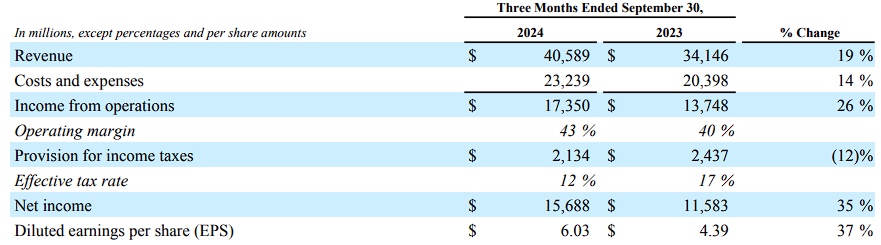

Meta’s most recent Q3 2024 earnings illustrate my point, with AI continuing to transform its operations, offerings, and margins. Specifically, Meta AI now boasts over 500 million monthly active users, while the company’s generative AI tools have significantly boosted ad performance, with businesses reporting a 7% increase in conversions. Then you have Llama, Meta’s open-source AI platform, which is gaining traction industry-wide with the release of Llama 3.2. The highly anticipated Llama 4 is expected to further boost adoption, which, in turn, will unlock new monetization opportunities across advertising, engagement, and enterprise solutions. There is early evidence of this, as advances in AI-driven recommendations increased time spent on Facebook and Instagram by 8% and 6% in the previous quarter.

Underappreciated Earnings Power and Margin Growth

Besides Meta’s top-line growth prospects, there is a strong chance that investors are underappreciating its earnings power. For context, in Q3, Meta’s operating income surged by 26% year-over-year to $17.4 billion, with its operating margin expanding from 40% to 43%. This multiple expansion was driven by cost-cutting measures and economies of scale. For instance, general and administrative expenses fell by 10%, primarily due to lower legal costs, while automation in data center management further reduced operational expenses.

In fact, Meta’s EBITDA margin reached 52.7% for the period, recording its highest level since 2018. Given these elevated margins, it’s easy to see why Meta should be able to convert revenue growth into notably more substantial earnings growth, as was the case in every single quarter throughout Fiscal 2024. So even though analysts fairly project EPS to grow by 52.2% in Fiscal 2024, they anticipate a dramatic slowdown to 12.5% in Fiscal 2025.

While one could argue this is appropriate given a potential “normalization,” I find it an improbable scenario given Meta’s margin expansion trajectory and already muted top-line estimates. For this reason, I would argue that Meta will be notably cheaper than its previously noted forward multiples suggest. Once stronger numbers materialize, the market will likely re-price the stock, driving sustained share price gains.

Is META Stock a Buy, According to Analysts?

Wall Street sentiment toward Meta Platforms remains highly vibrant, with analysts collectively rating the stock as a Strong Buy. Despite the rather conservative growth estimates, Meta has gathered 39 Buys, three Holds, and just one Sell over the past three months. The average META stock forecast of $683.72 implies a potential upside of 11.36% from current levels.

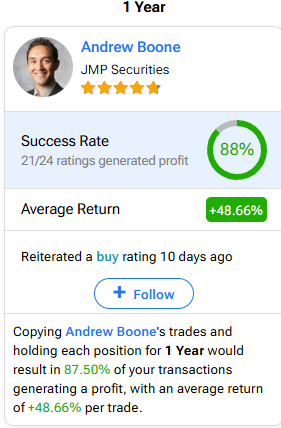

If you’re unsure which analyst to trust for trading META stock, Andrew Boone of JMP Securities stands out as the most accurate over one year. His recommendations have delivered an average return of 48.66% per rating, with an impressive 88% success rate.

Conclusion

In closing, the Magnificent 7 group of stocks delivered big in 2024, but Meta Platforms clearly stands out to me. Its strong revenue growth, rising margins, and ongoing AI developments form a setup that is kind of hard to ignore. I think Wall Street still underestimates its potential, leaving room for more upside. But even if Meta delivers in line with market expectations, the stock still seems considerably cheaper than the rest of the tech giants. I’m confident I will keep META stock as my largest holding.

Questions or Comments about the article? Write to editor@tipranks.com