The stock markets are hovering near record highs, making recent pullbacks an attractive opportunity to invest in some high-priced blue-chip stocks. The attraction here is obvious: the blue-chips are known for their stability and reliability, and they have proven that with long-term performance.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

However, not all blue-chip stocks are equally appealing. They are also subject to market cycles and business challenges, with some handling these better than others. Wall Street analysts recognize this and have been examining these stocks closely to determine which ones are the best buys.

Two companies, in particular, have picked up plenty of attention lately, and for opposite reasons. Meta Platforms (NASDAQ:META) and Boeing (NYSE:BA) are vastly different – one a 21st-century blue-chip newcomer, the other a long-time industrial stalwart. As we approach their earnings releases, let’s explore which of these blue-chip stocks analysts currently favor.

Meta Platforms

The first stock we’re looking at here is Meta Platforms, the social media company founded by Mark Zuckerberg. The company expanded quickly and has forever altered the ways that we engage online – with each other, with businesses, with advertising, with AI. Meta operates through its subsidiaries – Facebook, Instagram, Messenger, and WhatsApp – and through them can reach nearly half of the world’s total population.

The social media business makes up Meta’s core business, and the related digital advertising provides the company’s revenue stream – which in turn underwrites Meta’s ongoing development work in AI.

AI is clearly the coming wave in technology, and in fact, it’s already washing ashore. Meta is building a place for itself as a strong competitor, both in the current field of generative AI and in future applications of the technology. The company is applying AI tech to its metaverse model for social media, and is using it to fine-tune and effectively target its digital advertising efforts. We can see the results of this when we log on to social media sites, and find that the ads, posts, and recommended connections we see are all based on our past actions, or even on our recent web browsing activities.

More importantly, however, Meta is preparing itself to be an AI provider for a much wider base. The company has developed Llama, an open-source AI model that allows users to add to the code, adapt the model to their own situations, and fine-tune the available tools. The point of Llama is that AI is flexible – and that no two customers are identical. It’s an innovative take on AI applications, and one that Meta hopes will pan out profitably going forward.

Meta has the deep pockets and the solid revenue generation needed to back up these initiatives. The company reported $36.46 billion in revenue for the first quarter of this year, surpassing expectations by $240 million and achieving a 27% year-over-year growth. The bottom line came to $4.71 per share for the quarter, beating the forecast by 39 cents.

The company is on track to continue generating solid results, which we’ll see tomorrow in the 2Q24 release. Analysts are expecting to see ~$38.3 billion at the top line, which would represent a year-over-year increase of nearly 20%.

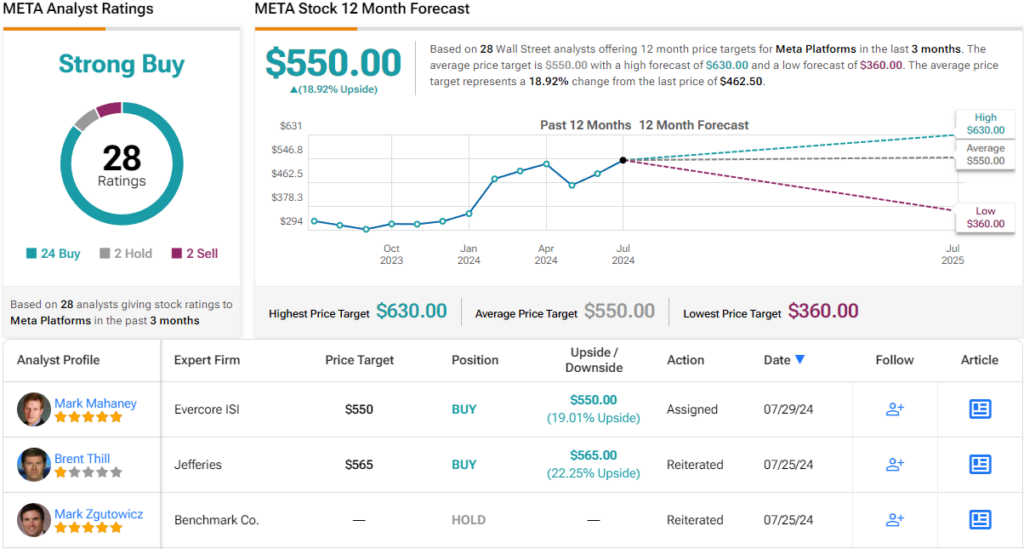

Covering Meta for Jefferies, analyst Brent Thill takes an upbeat outlook, basing his stance on the company’s revenue position and its solid work in AI.

“We are bullish on META’s position as a key pillar of open source AI and believe its investments have provided a free call option, potentially unlocking a whole new business. We see numerous potential rev streams such as releasing enterprise versions of Llama models with better support & security; introducing a Llama platform for custs to customize its models, create AI apps, pretrain models and more ad rev from increased engagement. META = Top Consumer AI Pick… Given the combination of higher engagement from AI investments, and continued advertiser ROI and efficiency, we see the potential for META to deliver low-20’s / high-teens reported revenue growth in FY24,” Brent opined.

Thill goes on to give Meta stock a Buy rating, with a price target of $565 to suggest a one-year upside potential of 21%. (To watch Thill’s track record, click here)

Overall, Meta gets a Strong Buy rating from the analyst consensus, based on 28 recent reviews that include 24 Buys, 2 Holds, and 2 Sells. The shares are trading for $461.97 and their $550 average target price implies a gain of ~19% on the one-year horizon. (See Meta stock forecast)

Boeing Company

Next up is Boeing, one of the world’s legendary industrial companies. Boeing has long been a leader in the aerospace field, and the company’s storied history includes such iconic aircraft as the P-26 fighter, the B-17 bomber, and the famous 707 and 747 airliners. More recently, Boeing has been facing a serious pile-up of headwinds. Crashes in 2018 and 2019 caused groundings in the 737 airliner fleet, the company’s best-selling product, and more recent incidents – when a fuselage panel blew off of an Alaska Airlines 737 during flight – have highlighted problems with Boeing’s production and quality control.

Airliners are not the only source of bad headlines for Boeing. The company is also facing a public relations disaster with the stranding of its Starliner space capsule at the International Space Station. An astronaut crew is stuck on the station, as a helium leak in the capsule prevents it from returning to Earth safely. Boeing says it is working to resolve the problem, but that the crew will be stuck on the ISS for at least several more weeks.

The company is also facing increased costs as it works to improve factory floor quality control, conduct airworthiness inspections, and otherwise convince both regulators and customers that its aircraft are safe.

And in one last headache for the company, earlier this year the CEO David Calhoun announced that he will step down from the top slot by year’s end. Board Chairman Larry Kellner at the same time announced that he will also step down. The company is still in the process of searching for their replacements.

It should come as no surprise, then, that Boeing’s shares are down sharply this year. The stock has fallen more than 28% year-to-date.

In its last reported quarter, 1Q24, Boeing missed on revenue and reported a quarterly net loss. At the top line, the company’s $16.6 billion revenue total was $620 million less than had been expected – and it was down 7.5% year-over-year. The company’s net loss, of $1.13 per share in non-GAAP measures, while negative, did provide a bright spot – it was 30 cents per share better than the forecasts.

Looking ahead, analysts are expecting increased revenue and a deeper net loss in the July 31 Q2 release. Revenues are expected at $17.38 billion, and the non-GAAP EPS loss is predicted at $1.93.

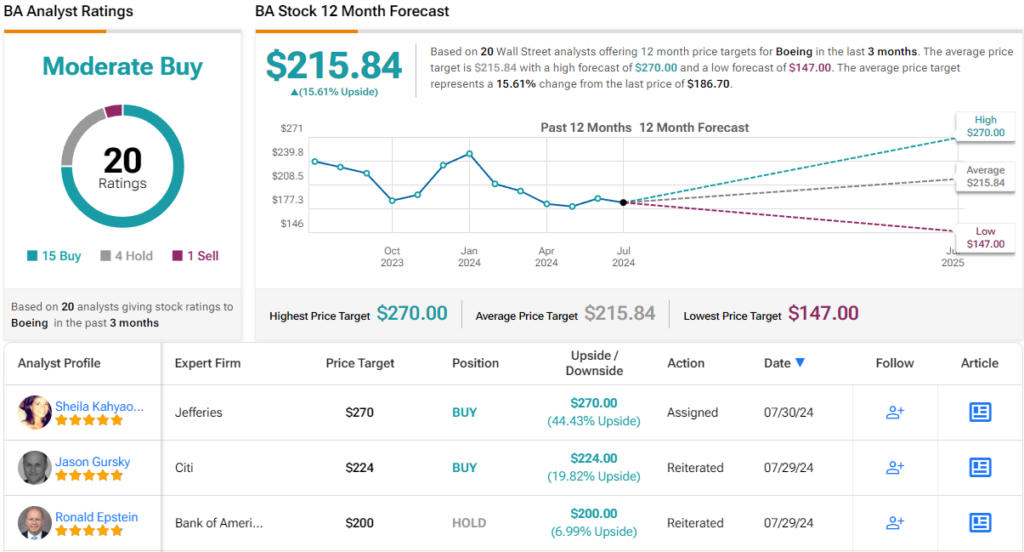

For 5-star analyst Ronald Epstein, who covers Boeing for Bank of America, the picture here is clear: now is not the time to buy BA.

“On one hand, the company has somewhat de-risked 2024e expectations after the late May announcement about burning FCF (vs. prior low single digit billion generation). Boeing remains uniquely positioned to the robust air traffic demand environment, with the moat that the duopoly creates. However, on the other hand, turning around operations could take time and uncertainties remain in the near future (Spirit Aero deal close and financing, CEO search, union negotiation, among others),” Epstein opined.

To this end, Epstein puts a Neutral (i.e. Hold) rating on Boeing shares, although his $200 price target still suggests an upside of ~9% heading into next year. (To watch Epstein’s track record, click here)

All in all, Boeing has a Moderate Buy consensus rating from the Street, based on 20 analyst reviews with a breakdown of 15 Buys, 4 Holds, and 1 Sell. Boeing stock is currently trading at 186.83 and its $215.84 average target price points toward a gain of ~16% over the next 12 months. (See Boeing stock forecast)

Summing up, the analysts’ consensus is clear: if you’re going to buy a blue-chip before the earnings come in, Meta Platforms is the superior choice.

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.