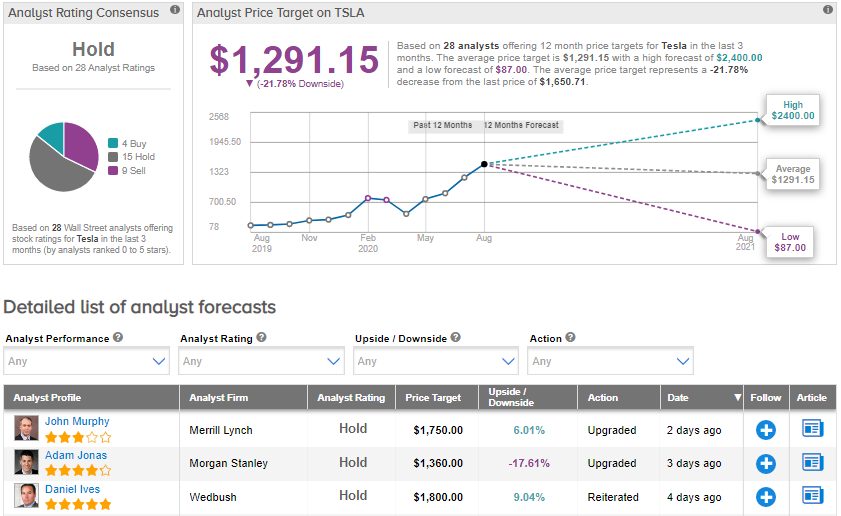

Merrill Lynch upgraded Tesla to Hold from Sell citing the company’s “unlimited” access to low-cost capital. Merrill Lynch analyst John Murphy also ramped up the stocks’s price target to $1,750 (6% upside potential) from $800.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

In a note to investors, Murphy said: “While we remain skeptical that TSLA (TSLA) will be the dominant EV automaker in the long-run, if a big global footprint can be built with no-cost capital, the ‘growth’ story would carry the day for the stock.” The analyst also added that Tesla’s unlimited access to low-cost capital should “accelerate its revenue growth rate to 50% annually over the next five years”.

On Aug. 13, Morgan Stanley analyst Adam Jonas raised TSLA to Hold from Sell citing a bullish outlook for the company’s third-party battery sales and electric-vehicle powertrain business. Jonas lifted the price target to $1,360 (17.6% downside potential) from $1,050.

The rating upgrades come just days after Tesla announced a 5:1 stock split in the form of a stock dividend and stated that shares will begin trading on a split adjusted basis on Aug. 31. The company announced that “Each stockholder of record on Aug. 21 will receive a dividend of four additional shares of common stock for each then-held share, to be distributed after close of trading on Aug. 28.”

Currently, the Street is sidelined on the stock. The Hold analyst consensus is based on 15 Holds, 4 Buys, and 9 Sells. Given the year-to-date stock price rally of 295%, the average price target of $1,291.15 implies downside potential of about 22%. (See TSLA stock analysis on TipRanks).

Related News:

Tesla Rises 6% In After-Hours On 5-for-1 Stock Split

Tesla CEO Elon Musk Sees ‘Strong’ Car Order Demand Despite Covid-19

Tesla’s Elon Musk Is Open To Offering Software And Batteries To Competitors