The investment thesis for MercadoLibre (NASDAQ:MELI), often called the “Amazon (NASDAQ:AMZN) of Latin America,” revolves around its high-growth tech status and complete dominance in the market. That’s why I’m bullish on MELI.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

In a fiercely competitive Latin American landscape, MercadoLibre has distinguished itself over recent years through its deep local market expertise, strategic diversification into both retail and fintech services, and robust logistics infrastructure.

In this article, I will delve into the details of the bullish thesis, highlighting why MercadoLibre stands out, in my opinion.

MercadoLibre’s Recipe for Success

MercadoLibre was founded in Argentina by its current CEO, Marcos Galperin. He saw the potential to create an e-commerce platform for Latin America when the market was just starting out.

The company began as an online marketplace where sellers and buyers could connect securely. They swiftly adapted to local market dynamics and expanded operations across multiple Latin American countries.

Over the past decade, MercadoLibre has marked its presence with significant investments in logistics, ensuring rapid and efficient delivery to regions lacking quality infrastructure. This has earned MercadoLibre the reputation of being the “Amazon of Latin America.” By 2023, MercadoLibre commanded a 21.6% share of total retail e-commerce sales in Latin America.

However, MercadoLibre is more than just an e-commerce giant. It’s more like a mix of Amazon and PayPal (NASDAQ:PYPL) for Latin America.

With the launch of MercadoPago, its fintech arm, MercadoLibre has really stepped up the online buying and selling experience. MercadoPago’s introduction of credit lines for consumers and sellers alike has been pivotal in fueling MercadoLibre’s exponential growth over the last five years.

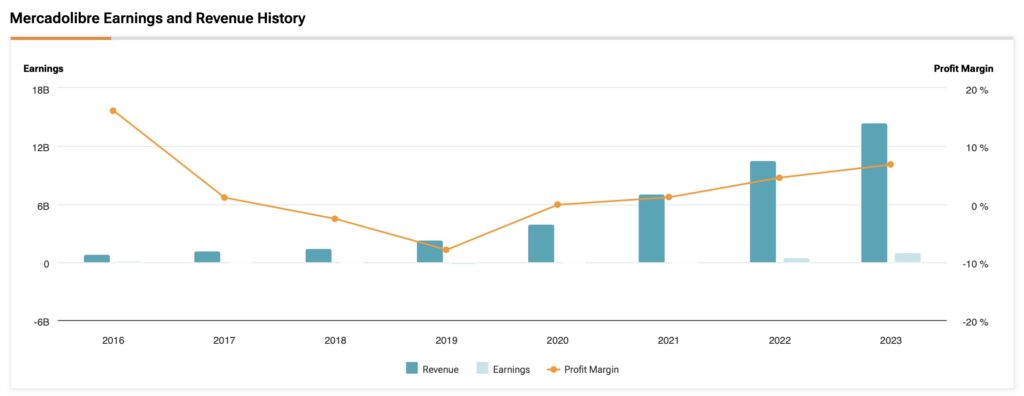

The introduction of an open marketplace empowered sellers of all scales, from large corporations to small entrepreneurs, boosting product sales. As illustrated in the chart below, MercadoLibre’s revenues surged from $2.3 billion in 2019 to $14.47 billion by 2023.

Today, approximately 42% of the company’s revenue is attributed to MercadoPago alone, managing $5.53 billion in assets and serving about 49 million users across Latin America.

This business integration has cemented MercadoLibre’s leadership in Latin American e-commerce, outpacing major competitors like Amazon, which focuses primarily on other regions.

Where MercadoLibre Stands Today

When you look at MercadoLibre’s business fundamentals, the company has really stepped up its position, with profitability and cash flow since hitting a low point in 2019.

Lately, MercadoLibre has been on the upswing, thanks to its investments in logistics and infrastructure. The company has ramped up its capital expenditures (CapEx) nearly four times, going from $136.8 million in 2019 to $573 million in 2021. By 2023, MercadoLibre’s CapEx was still at $509 million and has kept it steady since.

This has helped MercadoLibre keep pace with the rising demand in e-commerce and fintech, especially after the pandemic boom.

In terms of users, MercadoLibre now boasts 53.5 million unique active buyers and 49 million fintech monthly active users, with annual growth rates of 16% and 37.6%, respectively, as of Q1 2024.

On the e-commerce front, MercadoLibre has experienced exponential revenue growth. In the last quarter alone, revenues surged by 36% on a reported basis, with operating margins holding steady at 12.4%, resulting in a net income of $344 million, marking a yearly increase of 7.9%.

This robust performance is noteworthy due to the expansion in key markets like Mexico and Brazil, offsetting declines in gross merchandise volume (GMV) and items sold in Argentina, impacted by its hyperinflationary economy.

In its Fintech arm, MercadoPago saw its credit portfolio expand by 46% compared to the previous year, while assets under management (AUM) skyrocketed by 90% year-over-year, driven primarily by doubling figures in Brazil and Mexico.

This diversified business approach has enabled MercadoLibre to consistently generate solid cash flow from operations, even amid challenges in Argentina. In Q1, cash from operations (CFO) reached $1.5 billion. When we consider the CFO-to-sales ratio, MercadoLibre achieved a peak efficiency of operations with a ratio of 34.6%, reflecting a solid improvement from a few years ago.

Over the trailing 12 months, the CFO-to-sales ratio has hit a record high of 36.7%, indicating exceptional growth trends. For instance, this ratio stood at 35.5% in 2023 and 27.9% in 2022.

Valuation: No Bargain Seen

For growth-oriented companies like MercadoLibre, a valuable approach to valuation involves considering growth trends aligned with the PEG ratio, which combines the P/E ratio with expectations of earnings growth.

Estimates suggest that MELI is expected to achieve a long-term annualized EPS growth rate of 27.1%. Given a forward P/E ratio of 47x, this translates to a PEG ratio of 1.73x, indicating that MercadoLibre shares are not trading at a bargain. This higher multiple reflects the company’s successful execution in sustaining both financial and operational growth.

However, these are the perks of investing in high-quality growth stocks. I believe it would be contradictory for MELI to trade at a low multiple, considering its market leadership, diversified and unique business blend, and robust operating performance.

Is MELI Stock a Buy, According to Analysts?

MercadoLibre’s growth story has also gained traction on Wall Street. The analyst consensus for MELI is a Strong Buy, with 11 out of 13 analysts bullish, while the remaining two are neutral. The average price target for MELI stock stands at $1,920.00, suggesting upside potential of 22.21%.

One bullish analyst, Morgan Stanley’s (NYSE:MS) Andrew R. Ruben, emphasizes MercadoLibre’s investments in logistics. According to him, the company’s commitment to opening new fulfillment centers and loyalty programs is expected to drive growth in gross merchandise volume (GMV) and solidify its market position.

Conclusion

MercadoLibre holds onto its dominant position in a tough competitive landscape across emerging markets. Mixing e-commerce with fintech and heavily investing in logistics has really set MELI apart from the pack.

Recent financial and operational results show that MercadoLibre is still growing and moving in the right direction, reinforcing the bullish thesis. It will be crucial for the company to keep turning its operational strength into cash flow, which ideally will fuel growth investments and justify future valuation metrics.