We enter week 2 of peak earnings season with an improving growth rate for the second quarter. According to FactSet, blended earnings growth for Q2 currently stands at -42.4%, including actuals for the 26% of companies that have already reported and estimates for those remaining.

Don't Miss Our New Year's Offers:

- Discover the latest stocks recommended by top Wall Street analysts, all in one place with Analyst Top Stocks

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

Beyond the big tech names that are out this week: Apple, Alphabet, Facebook, Amazon (more on them later) we searched for what we’re calling “quintuple threats” reporting this week. This refers to companies that have seen their estimates trend upward in the last month, are expecting positive growth for Q2, have a history of beating estimates, currently hold a buy consensus from top analysts and carry a high smart score (7+). Only 5 names reporting this week showed up on that list:

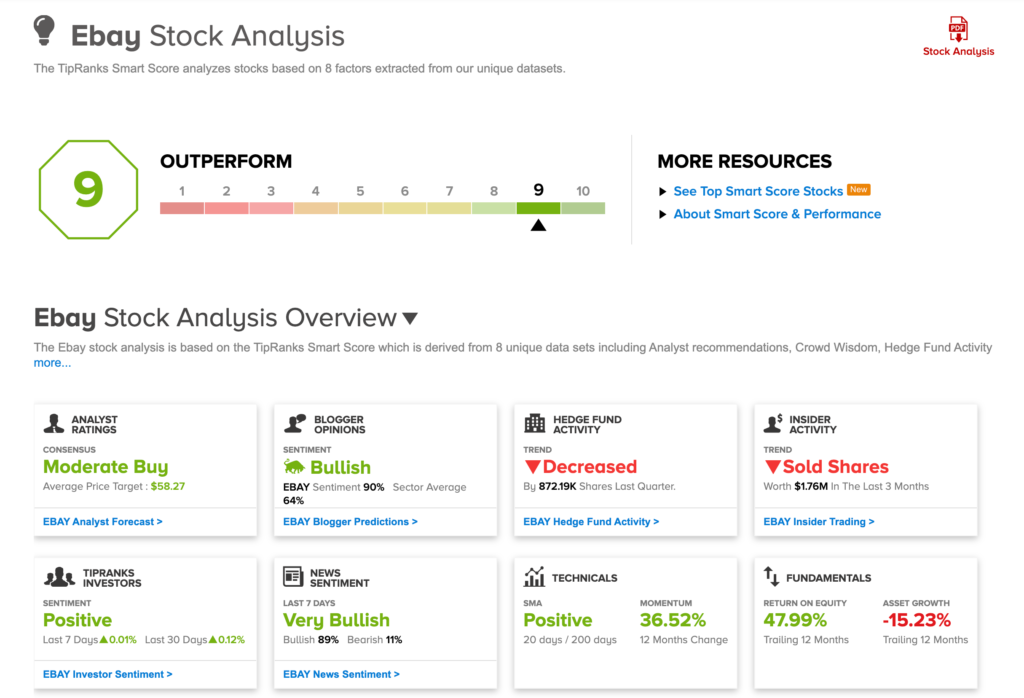

eBay (EBAY)

Reports Tuesday, July 28, after the close

- 6% increase in EPS estimates in the last month

- 54% EPS growth expected

- Beats EPS consensus 93% of the time

- Moderate buy from the 23 best analysts

- Smart Score of 9

With more consumers turning to online shopping during the pandemic and beyond, eBay’s stock surged nearly 110% since March 23rd lows. A focus on it’s core marketplace business seems to have come at the right time, especially as they just recently completed their deal to sell StubHub to Viagogo in February for $4.05B, weeks before lockdowns commenced here in the US, crippling the events business.

Investors will be paying special attention to Active Buyers which totaled 174M in Q1 and Gross Merchandise Value (GMV) which came in at $21.26B. This will also be the first report under new CEO, Jamie Iannone who joined eBay on April 27 from Walmart’s digital business.

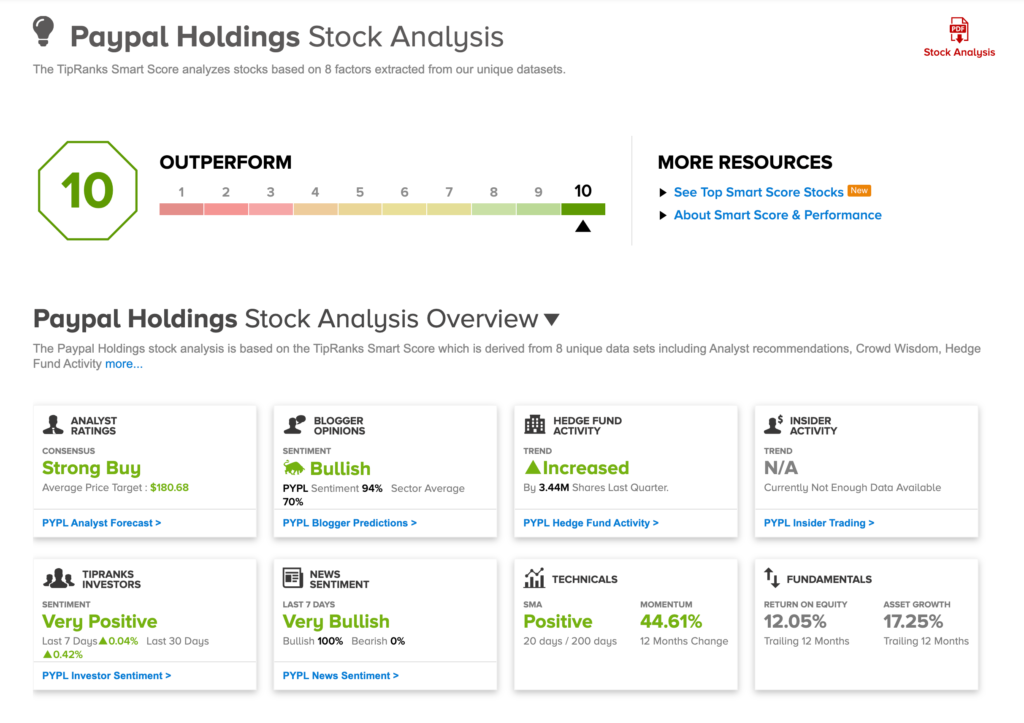

PayPal (PYPL)

Reports Wednesday, July 29, after the close

- 2% increase in EPS estimates in the last month

- 10% EPS growth expected

- Beats EPS consensus 100% of the time (since spin-off from eBay)

- Strong buy from the 33 best analysts

- Smart Score of 10

Hard to talk about eBay without mentioning PayPal, which many analysts believe saw a steep surge in Q2 due to more online buying. 27 of the best analysts on TipRanks have a PayPal as a Buy, 6 have a hold. Heath Terry, the 5-star analyst from Goldman Sachs raised his Price Target to $205 from $170 on Monday, expecting the business may have seen “unprecedented acceleration” in Q2. There will be a sharp focus on total payment volume (TPV) for Q2. Last quarter TPV came in at $190.6B, an 18% increase YoY.

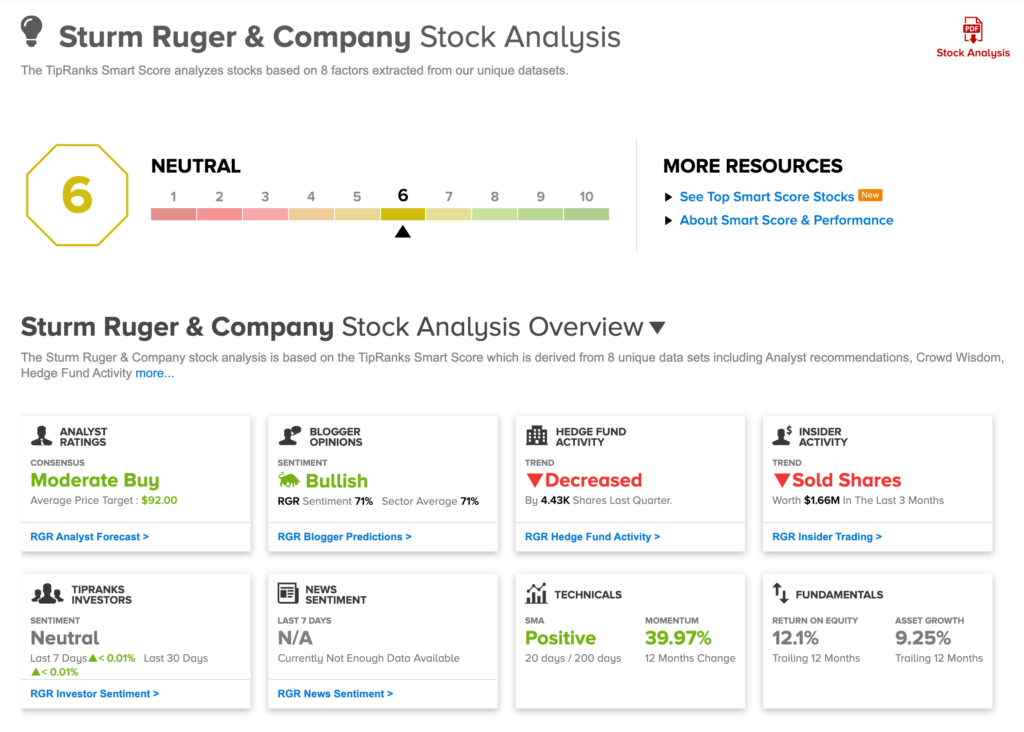

Sturm, Ruger & Co. (RGR)

Reports Wednesday, July 29, after the close

- 4% increase in EPS estimates in the last month

- 251% EPS growth expected

- Beats EPS consensus 70% of the time

- Moderate Buy

- Smart Score of 6

Ok so we made an exception on this one, as RGR only has a Smart Score of 6, and technically only has one top analyst covering it. But along with Smith & Wesson, estimates for firearms are increasing. Firearms tend to do well in election years due to the possibility of increased regulation if a Democrat is elected, and this year is no different. Background checks hit an all time high in June of 3.9M, beating the previous record of 3.7M in March. Analysts expect this surge to continue through the fall.

Lake Street analyst, Mark Smith, who has a 4.5 star rating TipRanks, said in a recent note that the latest run in gun manufacturers stock prices likely has to do with “unfilled demand from Covid, recent buying due to civil unrest and continued and perhaps heightened buying due to the upcoming election and potential for increased regulation following the election.” His RGR Buy rating was reiterated two weeks ago, with a PT of $92.00 (22% upside).

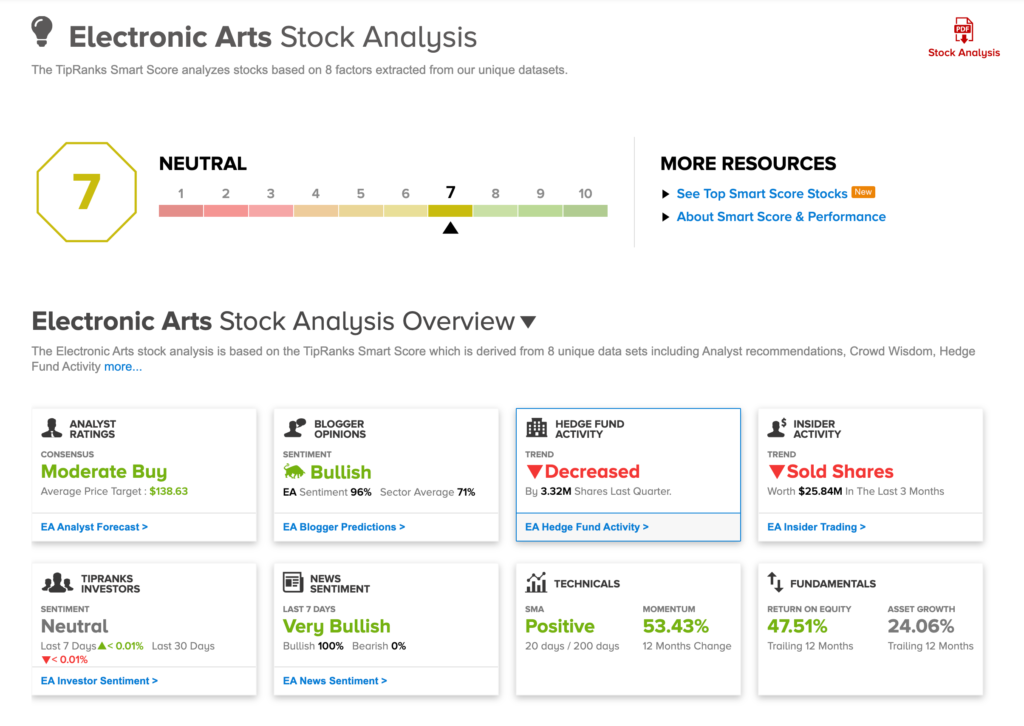

Electronic Arts (EA)

Reports Thursday, July 30, after the bell

- 5% increase in EPS estimates in the last month

- 241% EPS growth expected

- Beats EPS consensus 77% of the time

- Moderate Buy from the 15 best analysts

- Smart Score of 7

Video game makers have done increasingly well throughout the coronavirus pandemic, despite physical game sales falling, digital sales have been more than enough to offset those weaknesses. Electronic Arts biggest game franchise, FIFA, is due out with its next title in October, many analysts are questioning how the cancellation of live sports globally will impact sales of that latest game.

Another best selling franchise of EA is The Sims. Andrew Uerkwitz, the 5-star analyst from Oppenheimer remains bullish on this franchise, raising his price target on EA to $150 from $125 and commenting in a recent note “The Sims game has been a cultural phenomenon since it was first introduced in 2000. A best-selling PC game franchise, the series has sold over 200M copies in 20 years. While EA management has repeatedly highlighted the franchise’s unique market positioning and sustainable strength, we believe investors are generally unaware of the enduring appeal and growth potential of The Sims. This deep dive report attempts to dissect the game’s unique design, business model, and potential.”

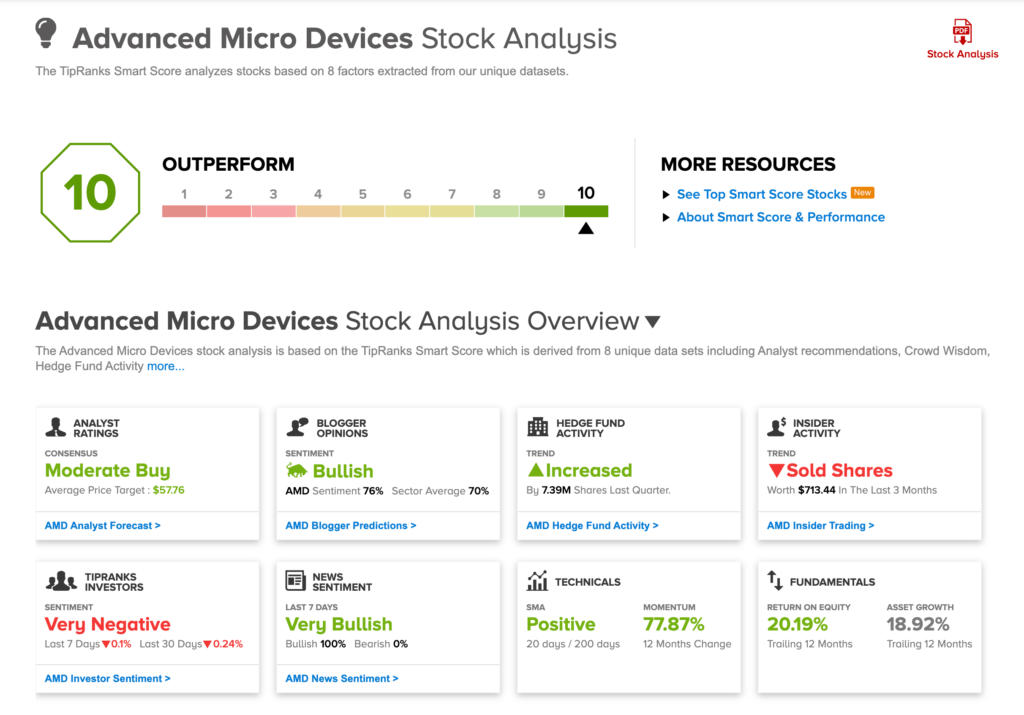

Advanced Micro Devices (AMD)

Reports Tuesday, July 28, after the close

- 2% increase in EPS estimates in the last month

- 135% EPS growth expected

- Beats EPS consensus 59%

- Moderate Buy from the 20 best analysts

- Smart Score of 10

Speaking of video and PC gaming, AMD is up this week. Semiconductors have been having a good earnings season so far, with big names like Texas Instruments and Teradyne both beating Wall Street estimates by 30%, and SkyWorks beating by 10%. Texas Instruments even hit a historic high of $137 after their report.

This week AMD is expected to keep the good times rolling, with EPS growth of 135%. They are expected to get a sizable boost from the increase in gaming activity, and sales of Microsoft Xbox and Sony Playstation, both of which tout AMD’s processor. An increase in notebook demand due to more people working from home should also benefit AMD’s notebook processor sales.

Also this Week: Big Tech Safe Havens

Most attention this week will be paid to big tech reports. Prices and valuations for these companies have seen an unprecedented run-up this year, causing many to question if they are overvalued or if these have become the newest safe havens for investor money during uncertain times. There is also concern about the over-concentration in just a few names.

Amazon (AMZN)

Reports Thursday, July 30, after the bell

- Expected Earnings Growth: -73%

- Expected Rev Growth: 28%

- Consensus Price Target: $3,142 (4.4% upside)

- Consensus Rating: Strong Buy (36 top analysts: 35 buys, 0 hold, 1 sell)

- Smart Score of 10

A stay-at-home favorite as more people opted to order online either out of necessity or out of preference during lockdowns. Amazon’s grocery businesses, Amazon Fresh and Whole Foods, were already surging at the end of last year. The COVID-19 pandemic just accelerated a trend already in motion. Online grocery has hit an inflection point after taking a while to catch on.

AWS will be another bright spot, especially with the move to work-from-home. Analysts expect that revenue to come in close to $11M for Q2.

And while the stock hit a record high of $3,200 on July 10, there are still a couple of concerning metrics heading into Q2 reports. Earnings dispersion is at $6.19, the 9th highest out of all S&P 500 companies. Also, the consensus EPS for Q2 has come down 77% in the last 3 months, never a great sign heading into a report. Analysts have likely brought down their estimates due to increased expenses associated with the COVID-19 pandemic, ie: increased spending on infrastructure, PPE for workers, overtime pay, increased workforce etc.

Facebook (FB)

Reports Wednesday July 29, after the bell

- Expected Earnings Growth: -30%

- Expected Rev Growth: 3%

- Consensus Price Target: $257.30 (2% upside)

- Consensus Rating: Strong Buy (32 top analysts: 28 buys, 4 hold)

- Smart Score of 9

Facebook’s muted response to hate speech and misinformation on its platform has been front page news lately, as has an ad boycott by more than 400 companies. While the impact of that boycott will not be seen in Q2 numbers, investors will likely ask about how it will affect the second half of the year. Daily and Monthly Active Users have been increasing steadily for FB, hitting 1.734B and 2.6M, respectively, last quarter. Analysts expect those will climb higher for Q2.

Analysts have also been focusing on COVID’s impact on ad spend. In a recent note, Credit Suisse suggested that certain industries such as auto, pharma and consumer goods have fared worse during this time, while entertainment, dining and retail budgets were not slashed as much as initially expected. 5-star analyst Steven Ju further remarked that “Overall, as we take stock of industry budget movements, we have left our near-term estimates essentially unchanged for now. And on the move for some marketers to pull spend, we note that in the midst of its previously-announced 8mm advertiser tally, investors are unlikely to see a material impact on revenue, particularly as ad inventory is sold on an auction.”

Apple (AAPL)

Reports Thursday, July 30, after the bell

- Expected Earnings Growth: -7%

- Expected Rev Growth: -4%

- Consensus Price Target: $376.52 (2% upside)

- Consensus Rating: Strong Buy (27 top analysts: 22 buys, 3 hold, 2 sell)

- Smart Score of 10

Despite rallying to all time highs last month, some analysts are still cautious on Apple as they wait to assess the damage done to iPhone sales by coronavirus. Rod Hall, 5 star analyst from Goldman Sachs, is one such analyst, and one of only two of the best analysts on TipRanks to have a sell on the stock and a PT of $299, 20% below where it currently trades. Hall anticipates guidance will not be provided for the rest of the year, both financial guidance and product guidance on launches such as the iPhone 12 (set to launch in September). Goldman believe’s if the iPhone is delayed until October that would result in a 6% hit to earnings for Q4.

Another closely watched number for the iPhone is Average Selling Price which is expected to slip through the rest of the year, along with demand.

Alphabet Inc (GOOGL)

Reports Thursday, July 30, after the bell

- Expected Earnings Growth: -44%

- Expected Rev Growth: -3%

- Consensus Price Target: $1636.40 (8.5% upside)

- Consensus Rating: Strong Buy (26 top analysts: all buys)

- Smart Score of 5

When Alphabet reports on Thursday investors will be looking for updates on ad revenues, Google Cloud and Youtube. Ad weakness is expected to be heaviest in travel, auto, entertainment and retail. Some of that will be offset by strength in Google Cloud and Youtube revenues. Last month, Youtube announced it was raising the price of it’s internet television service to $65/mo, a $15 increase. It’s too early to tell if this was a good decision because consumers are more willing to pay for in-home entertainment right now, or if the high unemployment rate or general job insecurity makes Youtube TV an easy target when consumers are looking to save money. We’ll be looking for updates on churn on Thursday.