Medtronic Plc. (NYSE: MDT) an American-Irish medical devices company reported mixed results for its third quarter of fiscal 2022, ending January 28, 2022. Following the news, shares gained 3.1% to close at $103.72 on February 22.

Despite the pandemic’s impact on healthcare procedural volumes, Medtronic delivered solid results aided by new product launches. The company even advanced its pipeline and won market share. Revenue across all of its segments, namely Cardiovascular, Medical Surgical, Neuroscience, and Diabetes, also reported mixed growth.

Mixed Q3FY22 Results

Medtronic’s adjusted earnings of $1.37 per share came in-line with the analyst estimates and grew 6% compared to the prior-year quarter.

However, quarterly revenue of $7.76 billion failed to meet analyst estimates of $7.94 billion. Revenue remained flat compared to the prior-year quarter. Medtronic’s U.S. revenue of $3.94 billion generated 51% of total revenue and non-U.S. developed market revenue of $2.44 billion contributed 31%, and Emerging markets revenue of $1.38 billion contributed the remaining 18%.

CEO Comments

Chairman and CEO of Medtronic, Geoff Martha, said, “The impact of the COVID-19 resurgence on healthcare procedure volumes, particularly in the United States, peaked in the final weeks of our quarter in January, causing our revenue to fall short of our expectations… We expect healthcare procedures to reaccelerate post-Omicron, and our commitment to durable and higher growth remains steadfast.”

Q4FY22 Guidance

The company is witnessing improvement in procedural volumes and expects continued recovery through March and April. Further, as the company exits Q4, it expects the procedural volumes to reach pre-COVID levels.

Based on the above, Medtronic forecasts Q4 adjusted earnings to fall between $1.56 and $1.58 per share, while the consensus is pegged at the higher end of the range at $1.58 per share. Notably, the company expects fourth-quarter organic revenue to grow by 5.5% over Q3FY21.

Analysts’ Take

Responding to Medtronic’s quarterly performance, Needham analyst Michael Matson reiterated a Buy rating on the stock but lowered the price target to $124 (19.5% upside potential) from $128.

According to Matson, MDT’s revenue miss was due to COVID-19’s impact on procedural volumes as patients delayed procedures. Commenting on his optimistic view of the stock, Matson said, “Medtronic’s deep product pipeline should drive improving revenue growth and enable margin improvement resulting in high single-digit EPS growth and P/E multiple expansion.”

Overall, the stock has a Moderate Buy consensus rating based on 12 Buys and 7 Holds. The average Medtronic price target of $125.39 implies 20.9% upside potential to current levels. Shares have lost 9.4% over the past year.

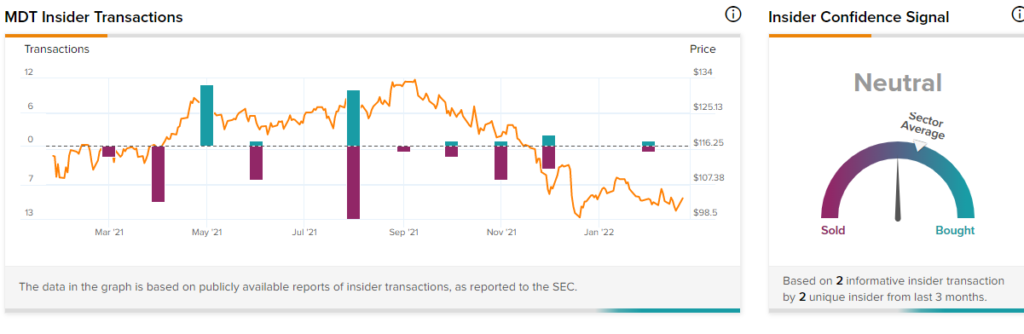

Insider Trading

TipRanks’ Insider Trading Activity shows that Insider Signal is currently Neutral on Medtronic, with corporate insiders selling $219.2K shares in the last quarter.

Download the TipRanks mobile app now

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Read full Disclaimer & Disclosure

Related News:

Dutch Regulator Fines Apple $5.7M – Report

China Warns Consumers Not to Buy Abbott Products Following Recall – Report

Carl Icahn Pursues McDonald’s Pig Sourcing, Nominates 2 Board Members