McDonald’s will launch three different versions of its new crispy chicken sandwich in the US on February 24 as the world’s biggest burger chain competes for a share of the growing market, Reuters reported.

The popularity of McDonald’s (MCD) Chicken McNuggets and 2020’s limited time Spicy Chicken McNuggets contributed to the company’s highest US comparative September sales in nearly a decade, according to the report.

Credit Suisse analyst Lauren Silberman told Reuters that as many as 150 sandwiches per day could be sold at an average location if McDonald’s crispy chicken is successful.

McDonald’s has certain comparative advantages compared to its competitors, according to Reuters. One such advantage is its huge scale. There are almost 14,000 McDonald’s restaurants across the US. That’s about as many as all the Chick-fil-A, Popeyes, KFC, Church’s, Wingstop, Zaxby’s, Bojangles and El Pollo Loco locations combined.

Richard Adams, a McDonald’s franchisees consultant told Reuters, “Customers have to drive past two or three McDonald’s to get to a (Chick-fil-A) or a Popeyes…That’s an opportunity to pull in those customers with a comparable product.”

According to the Reuters report, McDonald’s might also encounter some obstacles in achieving its ambitious crispy chicken plans including the lack of specialized poultry equipment, pressure cookers and hand-breading stations inside the stores. The advantage of scale might also be a double-edged sword as providing thick pre-breaded chicken to 14,000 stores could prove difficult. (See MCD stock analysis on TipRanks)

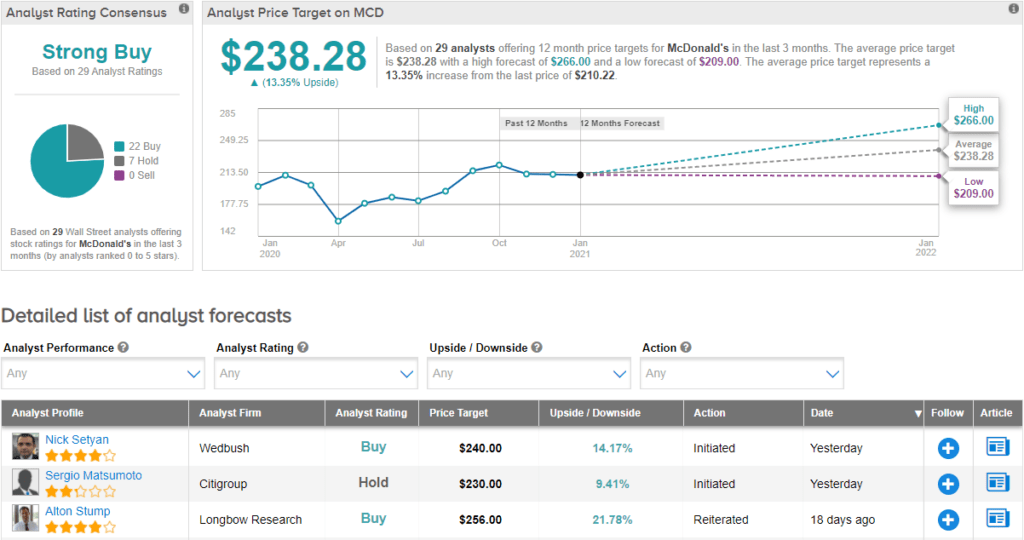

Wedbush analyst Nick Setyan this week initiated a Buy rating on the stock with a price target of $240 (14% upside potential).

Setyan sees mid-single-digit percentage global same-store growth in sales continuing and predicts accelerated free cash flow per share growth in 2022 and EPS growth in 2023 reaching double-digits percentages.

Consensus on the Street is a Strong Buy based on 22 Buys and 7 Holds. The average price target of $238.28 suggests upside potential of around 13% over the next 12 months.

Related News:

ViewRay Prices $50M Public Offering; Shares Drop 13%

Brookfield Asset Management To Take Property Unit Private In $5.9B Deal

T-Mobile To Buy Sprint-Branded Wireless Assets; Street Is Bullish