Maxar Technologies (MAXR) reported first-quarter revenue and EPS worse than what analysts expected.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

The provider of earth intelligence and space infrastructure solutions’ revenue came in at $392 million for the quarter ended March 31. This represents an increase of 2.9% in revenue from $381 million in the prior-year quarter, but it missed the consensus estimate of $560.3 million.

Meanwhile, Maxar reported a net loss of $84 million in 1Q 2021, a decrease from $78 million in 1Q 2020. Diluted loss per share was $1.30 per share, down from a loss of $0.80 in the prior-year period. Analysts expected a profit of $1.06 per share.

Maxar’s President and CEO Dan Jablonsky said, “We continued this quarter to make progress toward achieving our longer-term targets, including efforts to drive sustainable growth in both our Earth Intelligence and Space Infrastructure segments and to reduce our debt and leverage. In Earth Intelligence, we signed several renewals with commercial and international government customers and booked awards with the US Army and National Geospatial Intelligence Agency to support training, tactical, and intelligence missions. In Space Infrastructure, key wins included a contract modification with NASA and several study contracts supporting national security missions.”

Jablonski added that revenue and profit were impacted by a $28 million charge related to the Sirius-XM7 satellite program. (See Maxar Technologies stock analysis on TipRanks.)

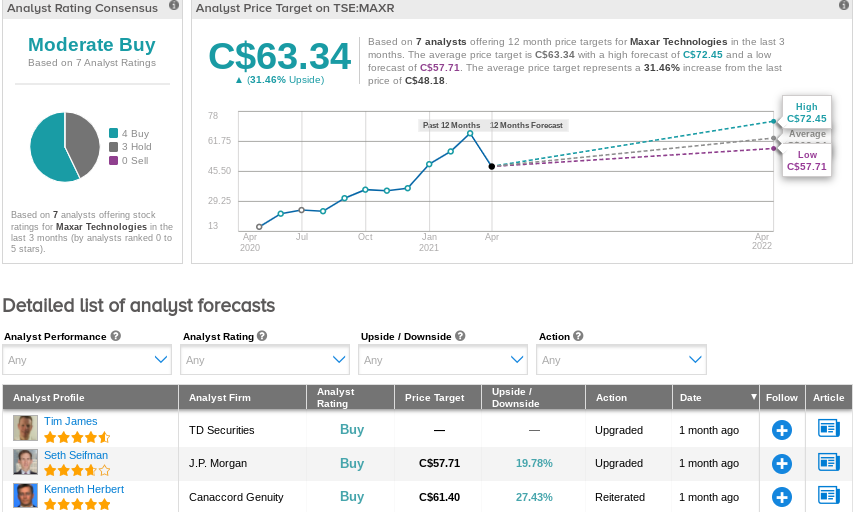

About a month ago, J.P. Morgan analyst Seth Seifman upgraded the stock rating from Hold to Buy, while lowering its price target to $47.00 (C$57.71) for a 19.8% upside potential. Seifman said in a research note that the launching of the WorldView Legion satellites later this year and news about the company’s EnhancedView contract are key catalysts for the stock.

Overall, the consensus on the Street is that MAXR is a Moderate Buy based on 4 Buys and 3 Holds. The average analyst price target of C$63.34 implies 31.5% upside potential to current levels.

Related News:

WELL Health Closes ExecHealth Acquisition

High Tide Buys 80% Stake in U.S. CBD Company FABCBD

Tilray’s Merger With Aphria Closes, Creates Global Cannabis Leader