The market has responded favorably to Matador Resources (MTDR) following Q3 results that surpassed analyst expectations and recorded a new high in oil production. This strong performance is credited partly to successfully integrating recently acquired Ameredev assets and operational efficiencies. The company raised the bar by increasing its full-year production and capital spending forecasts. The amped-up financial forecast is backed by Matador’s midstream assets, which report record processing volumes and net income.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

As a cherry on top, Matador increased its dividend, and analysts have revised their price targets and ratings upwardly. Matador’s upside appears promising, making it an intriguing option for investors in oil & gas.

Matador Grows Through Acquisition

Matador is an energy company primarily focused on exploring, developing, producing, and acquiring oil and natural gas resources across America. The company runs midstream operations, including vital services such as natural gas processing, oil transportation, gathering natural gas and oil, and produced water disposal.

The company is focused on unconventional plays like shale. They have concentrated on the oil and liquids-rich section of the Wolfcamp and Bone Spring plays, located in the Delaware Basin (stretching from Southeast New Mexico to West Texas). In addition, Matador operates in South Texas’ Eagle Ford shale play, as well as the Haynesville shale and Cotton Valley plays in Northwest Louisiana.

In the third quarter of 2024, Matador successfully integrated the Ameredev acquisition, a key milestone, offering an additional block of 33,500 net acres. The acquired assets have produced an average of 31,500 barrels of oil equivalent (BOE) per day since the acquisition closed on September 18, 2024. The first seven wells turned to sales since acquisition have exceeded expectations by over 10% and averaged 1,975 BOE per day during initial tests.

Operational efficiencies and synergies from the Ameredev assets are expected to result in approximately $160 million within the next five years. A further monthly synergy of over $1 million could be gained from improved lease operating expenses. The Ameredev acquisition also included a 19% equity interest in the parent company of Piñon Midstream, expected to yield between $110 million and $120 million from its sale to Enterprise Products Partners L.P. This income will be utilized to repay borrowings.

Analysis of Matador’s Recent Financial Results

The company recently reported its Q3 financial results. Revenue reached $899.78 million, marking a 16.5% year-over-year increase and beating analyst expectations by $69.53 million. The company reported record production of 171,480 BOE per day during the quarter, indicating a 5% improvement from their guidance.

The San Mateo joint venture achieved record water handling volumes of 513,000 barrels per day due to increased volumes from third-party participants. This led to a 66% rise in net income of $49.8 million. Another subsidiary, Pronto, plans to expand the Marlan Processing Plant to be operational during the first half of 2025. Improved operational efficiencies helped drive an increase of 32% in net cash from operational activities. Overall, earnings per share (EPS) of $1.89 surpassed analyst estimates by $0.24.

The Board of Directors increased the quarterly dividend by 25% to $0.25, or a dividend yield of 1.54%. This was the fifth dividend increase in four years.

Management has issued forward guidance, predicting steadily improving performance and record outcomes in 2025, anticipating an average total production exceeding 200,000 BOE per day. The company has strategically positioned itself to modify its drilling program in response to significant oil price changes without substantial costs. It has hedged approximately 30-40% of its oil production until June 2025 as a protective measure for its balance sheet.

Is MTDR a Buy?

The stock has been on a bit of a rollercoaster ride, declining 13% over the past year. It trades on the lower end of its 52-week price range of $47.15 – $71.08. The decline in share price has apparently been greeted by Matador’s management team as a buying opportunity, with executive officers and directors acquiring approximately $1,400,000 of Matador stock over the last twelve months.

Analysts following the company have also adopted a positive outlook on the shares. For instance, Stephens analyst Michael Scialla recently reiterated an Overweight rating and raised the price target on the shares to $78. Meanwhile, BMO Capital’s Phillip Jungwirth also maintained an Outperform rating and increased the price target on Matador to $78.

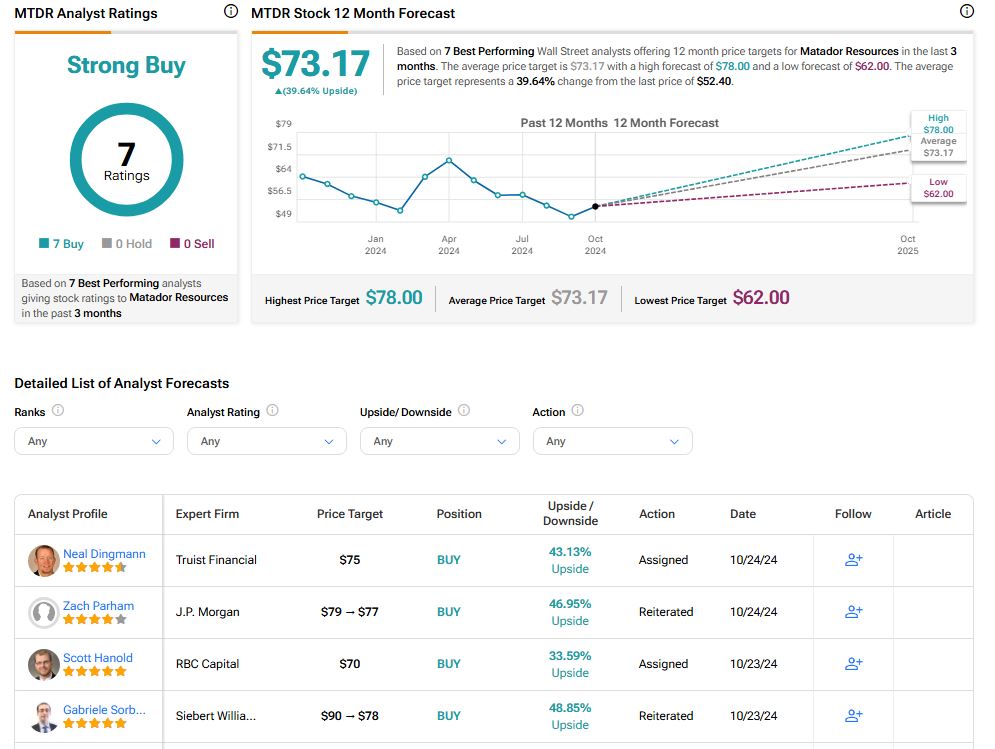

Matador Resources is rated a Strong Buy overall, based on seven analysts’ recent recommendations. The average price target for MTDR stock is $73.17, which represents a potential upside of 39.64% from current levels.

Final Thoughts on MTDR

Matador has made impressive strides recently, with Q3 results surpassing expectations and achieving a new high in oil output. The company looks set to continue this trend after raising its production and capital expenditure forecasts for the full year. Based on recent financial results and forward-looking projections, MTDR offers a potentially promising outlook, making it a compelling investment option.