PDD Holdings (PDD) investors have endured a frustrating year, with the stock languishing despite blockbuster earnings–a disconnect that highlights how China’s macroeconomic headwinds and regulatory ambiguity overshadow the company’s undeniable momentum. While those risks are real for this e-commerce platform provider, I believe they are not more than reflected in the share price. The stock’s valuation, in particular, is jaw-dropping when you consider that PDD boasts a net cash pile of $44 billion and trades at less than 8x its free cash flow. For this reason, I am bullish on PDD stock.

Why the Market Is Still Cautious on PDD Stock

So why hasn’t Wall Street embraced PDD’s success? I see three major challenges upsetting investors. First are China’s domestic headwinds, second are geopolitical tensions, and third is relentless competition. Over the past year, PDD has faced a slowing Chinese economy, friction between the U.S. and China, and a crowded e-commerce battlefield, creating a perfect storm that’s kept investors skittish.

Specifically, sentiment toward Chinese tech stocks remains dim after years of regulatory crackdowns and a spluttering post-pandemic recovery. Unlike fintech and edtech peers, PDD has mostly dodged Beijing’s wrath, yet the memory of abrupt clampdowns lingers. Heavy discounting spurs some consumer demand, but discretionary spending is lukewarm, making policy surprises or another slowdown a real threat. Meanwhile, PDD’s global ambitions face fresh hurdles. Temu’s low prices rely on a U.S. trade loophole lawmakers may close, and broader Sino-U.S. tensions (think tech decoupling or data-privacy clashes) cast a long shadow.

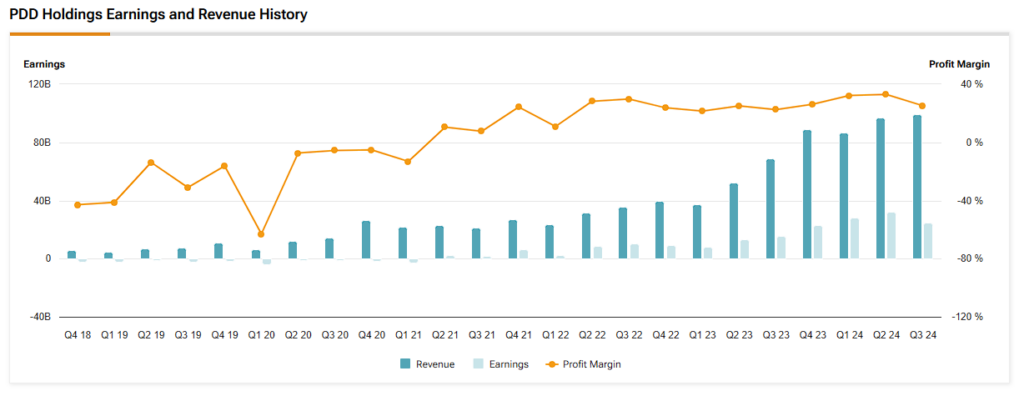

At home, the e-commerce war is bruising. Alibaba, JD.com, Douyin, and Shein all vie for dominance with price cuts and flashy promotions. PDD is fighting back by pouring cash into subsidies, logistics, and merchant perks, a strategy that squeezed margins from 28% to 24% last quarter. Management may have called it an “ecosystem investment” that may jolt profits but is crucial for growth. However, bears will tell you they see a company stretched thin in a brutal market. This is what has imprisoned PDD in limbo. It has been caught between bold ambition and looming uncertainties.

PDD Defies the Skeptics

Yet, for all the caution, PDD keeps defying skeptics. Sales surged 59% last year, fueled by a 29% jump in marketing revenue and a massive 108% increase in transaction fees. The flood of goods passing through its platform is unbelievable. This is paired with booming merchant and advertiser activity. The profits are just as good, with operating income soaring 85% and net income skyrocketing 87%. Scaling up hasn’t diluted profitability; it has amplified it, which shows just how crazy-efficient PDD’s leverage has become.

What’s the secret? PDD calls it “high-quality development,” which is basically just pouring cash into its ecosystem to benefit merchants, consumers, and the platform alike. A RMB 10 billion ($1.38 billion) fee-cut program slashed sellers’ costs, while logistics upgrades and trust enhancements lured more participants. The result? Merchants flood PDD with goods, consumers enjoy better product selection and shipping, and trading volumes soar—a win-win for everyone.

Then, you have PDD’s rural focus, which adds another dimension. They are linking farmers directly to buyers in tapped, underserved markets. Special logistics initiatives and free shipping for nearly 100 million rural users have ignited double-digit order growth in China’s hinterlands. Outside of China, Temu’s meteoric rise (remember when it topped U.S. app charts in under a year) proves PDD can export its magic.

An Absurdly Cheap Stock for What You’re Getting

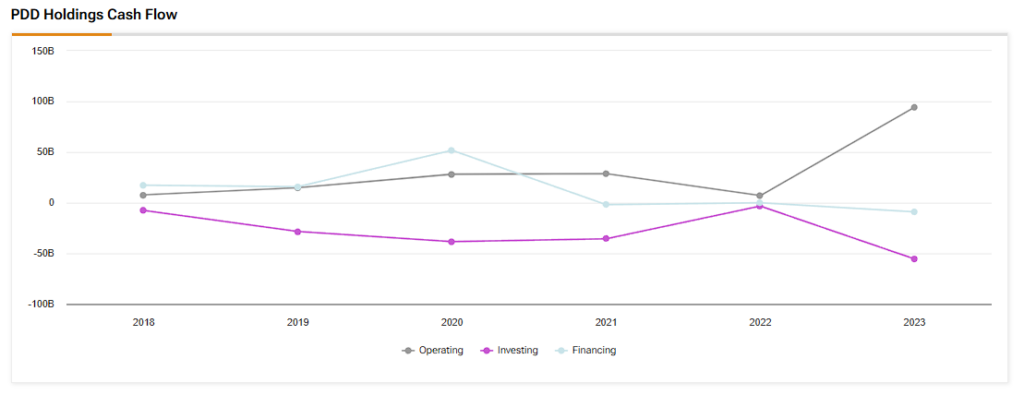

With such momentum, you’d expect PDD to trade at a premium. Instead, it’s a steal. Sitting on a $45 billion net cash position and generating $16.7 billion in free cash flow last year, PDD’s market cap barely exceeds its cash plus a few years’ earnings. Strip out the cash, and it’s valued at under 8x free cash flow, a multiple better fit for a sleepy utility, not an e-commerce growth juggernaut.

In the meantime, PDD’s cash hoard offers a buffer and flexibility few peers can match, while PDD’s breakneck expansion keeps lifting its intrinsic value. This is why I believe that this is growth at a value price for patient investors. A single-digit multiple on a business outpacing nearly every e-commerce rival warrants huge upside potential even if the company slows down significantly.

Is PDD Holdings a Good Stock to Buy?

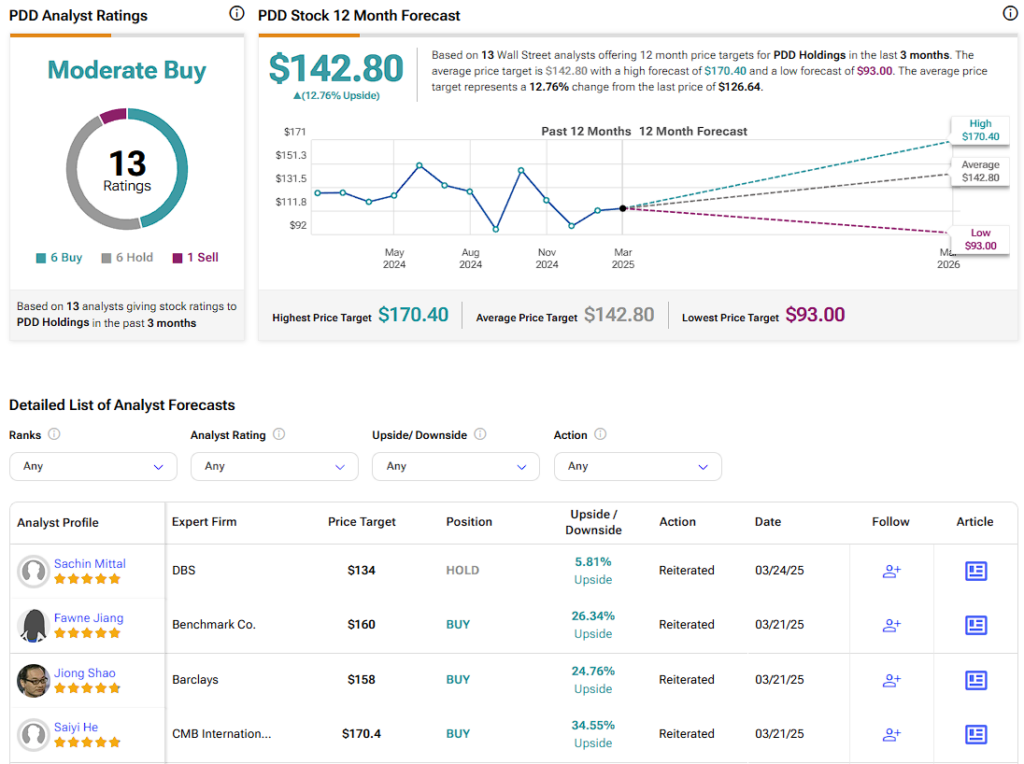

Wall Street is even split but with a bullish bias on the stock, suggesting the potential for a rebound in the near term. In particular, PDD features a Moderate Buy consensus rating based on six Buy, six Hold, and one Sell ratings assigned in the past three months. Today, the average PDD stock price target is $142.80 per share, implying almost 13% upside potential over the coming year.

PDD Serves as a Bargain Basement Pick-Up

PDD Holdings’ stock offers a compelling opportunity for long-term investors. Despite the short-term headwinds like geopolitical risks and competitive pressures, its stellar growth, proven ability to rise above obstacles, and massive cash reserves underscore a steep discount to its potential. At just under 8x free cash flow, PDD blends high growth with a value price, a rarity in today’s market even following the recent sell-off. As fears subside and execution persists, the stock’s upside could finally align with its fundamentals, rewarding patient shareholders.