Lyft (LYFT) stock dropped about 8% after last Wednesday’s earnings report as the market reacted to what it saw as weak Q4 results and a lackluster 2025 outlook. Investors were unimpressed by soft booking guidance and the company’s price cuts to stay competitive. However, I’m bullish on Lyft due to its shift to profitability, attractive valuation, and newly launched share repurchase program. Wall St. analysts are projecting a nearly 30% upside for the stock throughout 2025, and yet, the majority rate the stock as a Hold.

However, having bounced back strongly since its mixed Q4 earnings report, Lyft is 4% higher since last week. Moreover, this stock offers stiff competition to the current market leader, Uber, and it has a viable strategy to win market share in the medium- and long term.

Throwing the Baby Out with the Bathwater

While the market was pessimistic on Lyft, there is much to like here. Wall St. analysts, as astute as they are, may have thrown the baby out with the bathwater with LYFT. The company achieved record results with all-time highs in the number of rides and riders. Encouragingly, this quarter brought Lyft’s streak of double-digit ride growth to eight straight quarters, so the company is growing in usage and popularity with rideshare users.

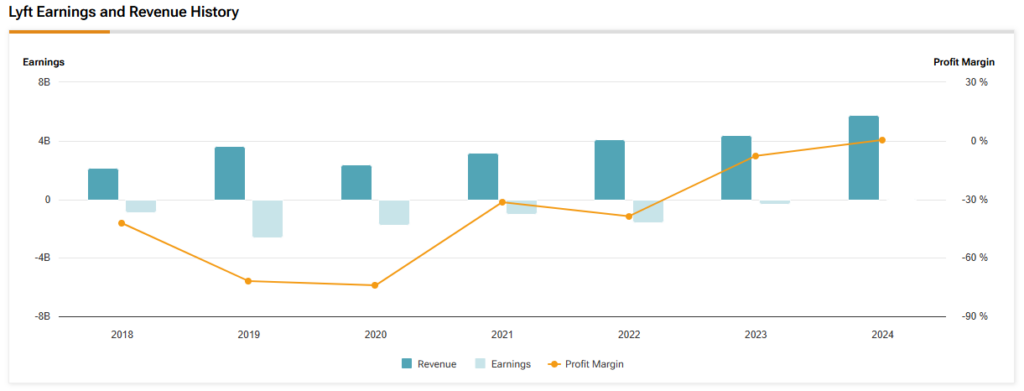

Furthermore, Lyft posted full-year GAAP profitability for the first time since going public in 2019. The company swung from a loss of $340.3 million in 2023 to earning $22.8 million in net income in 2024. For the quarter, Lyft swung from a loss of $0.88 per share last year to earning $0.06 a share this year, beating analyst estimates by $0.07. Lyft also posted its first full year of positive free cash flow, generating a record $766 million in free cash flow for 2024.

While the market didn’t like Lyft’s soft guidance for rides to grow by a mid-teens percentage year-over-year and gross bookings to grow 10-14% for the first quarter of 2025, Lyft’s overall trajectory is healthy.

Lyft’s Bargain Valuation Despite Setting Higher Highs

Lyft is profitable, unlike some of the once-hyped tech and tech-adjacent companies that went public in the late 2010s and early 2020s. Surprisingly, the company remains relatively undervalued compared to its peers. Lyft trades at 12.5x consensus 2025 earnings estimates, which sees Lyft delivering $1.01 per share in earnings. Looking further, the stock is even cheaper—analysts expect Lyft to increase earnings to $1.42 per share in 2026, so the stock is trading at a bargain basement multiple of 9.7x 2026 earnings estimates.

Bargain multiples mean that Lyft is significantly cheaper than the broader market, with the S&P 500 (SPX) currently fetching over 25x earnings. Lyft is also considerably more affordable than its closest competitor, Uber (UBER), which trades for 33.1x 2025 earnings estimates. Uber is undoubtedly the dominant company in the rideshare sector niche, and one can make the case that it deserves a higher multiple, but overall, these are very similar businesses, so there is a potential upside for Lyft if it can narrow even some of this gap with Uber’s valuation.

Lyft Boosts Shareholder Value with $500M Buyback Plan

Lyft is not a dividend stock. However, the company will start returning a significant amount of capital to shareholders through share repurchases. During the fourth quarter earnings call, Lyft announced it will participate in its inaugural share repurchase program. Lyft could repurchase up to $500 million worth of its shares, a significant amount given the company’s market cap of $5.6 billion.

Share repurchases are potentially advantageous to shareholders because they reduce the number of outstanding shares, thus increasing earnings per share and the proportion of ownership each shareholder has. They can also signal that management views its stock as undervalued.

Is Lyft Stock a Good Buy?

Turning to Wall Street, LYFT earns a Hold consensus rating based on seven Buy, 23 Hold, and zero Sell ratings assigned over the past three months. The average LYFT stock price target of $17.50 per share implies a 30% upside potential from current levels. Despite the strong upside expected, Wall St. analysts are in a collective holding pattern on LYFT stock.

Overlooked LYFT Stock Deserves a Second Look

I’m bullish on Lyft due to its newfound profitability and attractive valuation. The stock remains cheap compared to the broader market and its closest competitor, Uber. The company’s sizable share repurchase program is another positive signal. With the number of rides and riders rising, Lyft is moving in the right direction. The market has been overly harsh with Lyft, and the stock has been pushed into oversold territory. Patient investors could be well rewarded in the long term once future results corroborate the view that the ridesharing niche is large and fertile enough to sustain more than just one giant company like Uber.

Questions or Comments about the article? Write to editor@tipranks.com