Popular athleisure retailer Lululemon (LULU) is gearing up to release its earning results today after market close.

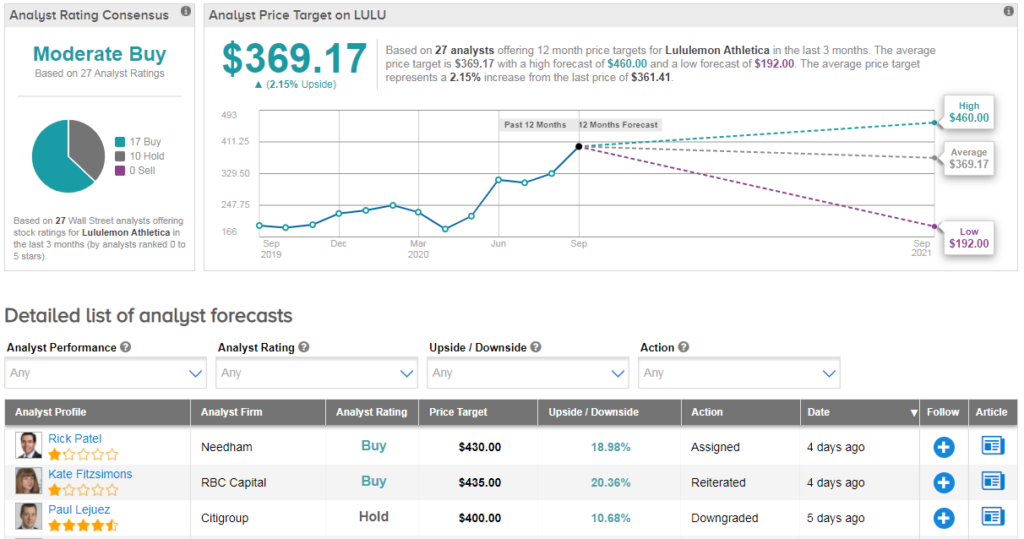

Ahead of this key report, RBC Capital analyst Kate Fitzsimons has reiterated her LULU buy rating, while bumping up the price target from $348 to $435.

She cited the company’s recent acquisition of fitness hardware startup Mirror for $500 million, which closed in July, writing: “While expensive, we believe rightly so given LULU’s sweet spot of category momentum, customer loyalty, and an expanding TAM [total addressable market] now inclusive of MIRROR.”

Into the print, the analyst raised her 2Q EPS estimates on LULU to $0.57, based on total revenues of $840MM (down 5%) with stores revenues -52%, Direct +125% (vs. 68% in 1Q), and Other (including MIRROR) -15%.

Included in the +125% Direct growth estimate is a strong response to LULU’s July online warehouse sale, says Fitzsimons, with search data showing spiking interest online.

“EPS assumes an EBIT margin of 12%, down 700-bps YoY owing to fixed cost deleverage on closed stores (majority messaged to be open by end of June) and reduced productivity on occupancy restrictions and tough compares YoY” the analyst wrote, adding that search data for the athletic category was robust in 2Q.

Looking forward, Fitzsimons now expects 3Q20 updated EPS of $0.93 based on total revenues at $981MM (Street $975MM) based on a 5% total comp, with 4Q20 EPS at $2.43, based on a 12% total comp.

Shares in LULU have surged 56% year-to-date, but the RBC analyst is not deterred, telling investors: “Recent outperformance reflects increasing excitement on expanding market share opportunity ahead with MIRROR as a kicker.” She sees underlying mid-teens top-line growth longer-term, including international expansion.

Overall, Lululemon shows a cautiously optimistic Moderate Buy Street consensus with some analysts sticking to the sidelines on valuation concerns. Meanwhile the average analyst price target of $369 indicates 2% upside potential from current levels. (See LULU stock analysis on TipRanks).

For Citigroup analyst Paul Lejuez enough is enough. He has just downgraded LULU to hold with a $400 PT, saying: “the stock seems to be pricing in perfection (and we should keep in mind with expected strong results for the rest of fiscal 2020, they will have tougher comparisons in fiscal 2021 in a category everyone seems to be chasing after).”

Related News:

American Outdoor Reports Upbeat 1Q On Solid E-Commerce Sales

Amazon Bans Foreign Seeds Sales In US Amid Mystery Packages – Report

US Backs Microsoft’s $10B JEDI Cloud Award; Wedbush Says JEDI ‘Game Changer’