Call it the apparel apocalypse, if you will, with shares of Lululemon (NASDAQ:LULU) and Nike (NYSE:NKE) both stretching lower after posting some pretty weak quarterly results last week. As the two downward dogs look to get even cheaper as analysts and investors digest the latest round of ugly results, questions linger as to what could put a bottom in the two apparel kings.

Undoubtedly, Lululemon and Nike boast some of the strongest brands in the apparel retail scene. And though you can point a finger at the state of the consumer, I don’t think consumer health should shoulder all of the blame for recent weakness.

In fact, if you look at other corners of the discretionary retail scene (think luxury goods and beauty retail), it’s more apparent that consumers do, in fact, have cash to spend on nice-to-have goods. With rising competition in the sporty clothing scene (Lululemon, in particular, has a number of hungry rivals targeting its share), one has to wonder how much of the recent quarterly weakness was due to shifts in consumer tastes.

Still, despite LULU and NKE’s recent post-earnings plunges (down 16% and 7%, respectively), I remain bullish on both companies as they look to leverage their brands to orchestrate a comeback in future quarters.

Lululemon (NASDAQ:LULU)

Could it be that Lululemon is more of a Millennial thing as Gen Z and Alphas look to alternatives like Alo Yoga and Athleta to make their own statement? It’s really tough to tell. Though Lululemon yoga wear will always be one of the best-in-class apparel brands (it is a pioneer, after all), I question the company’s ability to maintain enviable margins long-term as younger, less-affluent consumers discover other options that have emerged in the yoga space in recent years.

Just look at e.l.f Beauty (NYSE:ELF), one of the market’s biggest winners and beauty market disruptors in recent years. Its lower prices and crafty social-media-focused marketing were key drivers behind why the firm was able to outdo its larger rivals for the business of younger consumers.

Arguably, Lululemon is the king of social-media-based marketing. However, its prices are anything but affordable, especially for the youth who may come to question the opportunity costs of spending more than $100 on a pair of yoga pants. And for more affluent consumers with money to spend on “premium” yoga wear, there’s also stiffer competition on the higher end nowadays.

Sure, Lululemon’s apparel may be high-quality, with innovative fabrics that warrant higher prices. However, competing athleisure brands—like Athleta on the value end and Alo on the high end—have intriguing designs and “innovations” of their own. Moreover, I think Alo and Athleta are starting to understand how to resonate better with athleisure customers.

For now, I view Alo Yoga as the bigger threat to Lululemon’s dominance. The company hasn’t just done a great job of marketing itself on social media platforms; it’s also been dawned on by massive celebrities, including Kylie Jenner. When such a big-name celebrity endorses a new brand, you can be sure that people will be talking (and buying).

At this juncture, Alo seems to be the fresher brand on the scene. Though I’m sure many will remain loyal to Lululemon, it’s clear it needs to do more to hit the spot with younger consumers who may be inclined to go for Alo. Given the capabilities of Lululemon’s managers, the company can likely strike back as it looks to stay on the offensive.

What Is the Price Target for LULU Stock?

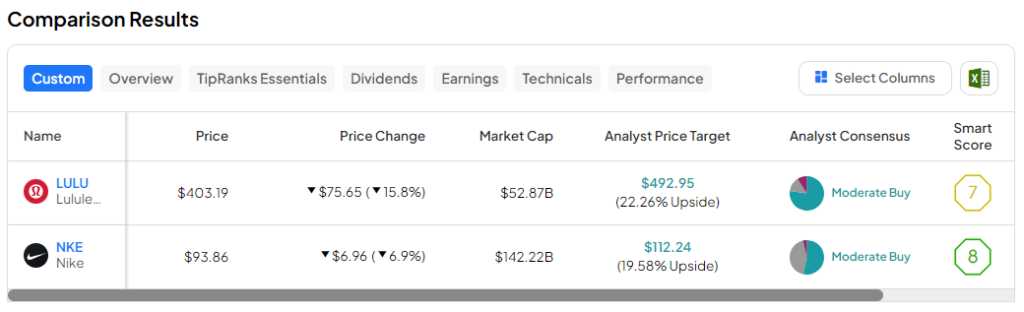

Lululemon stock is a Moderate Buy, according to analysts, with 15 Buys and three Holds assigned in the past three months. The average LULU stock price target of $516.16 implies 28% upside potential.

Nike (NYSE:NKE)

Nike stock is flirting with multi-year lows again after recently sagging below $100 per share on the back of its own quarterly disappointment. Undoubtedly, Nike doesn’t have the same growth expectations as Lululemon. However, the recent results did not show anything for dip-buyers to get excited about. The sneaker giant’s sales have flatlined, and they could stay flat for quite a while as management guided for more of the same for the rest of its fiscal year.

With shares up a mere 19% in the past five years, it’s clear that Nike is stuck in a pretty long-term funk. And it may take more than another pair of dunks to get the stock swooshing higher again. Fortunately, there’s a good amount of support in the low-$90 range for dip-buyers seeking an entry point. Apart from technical support, the stock looks modestly valued at 27.3 times trailing price-to-earnings, well below its historical average.

Though consumers may be getting fatigued from Nike’s current slate, it’s a mistake to doubt its innovative abilities, even as rivals like On Holdings (NASDAQ:ONON) begin to cut further into Nike’s turf. Looking ahead, the company has potential catalysts that could help shares jump higher again.

Most notably, the Air Max DN (featuring sustainable materials and advanced comfort) launch could hold the potential to help Nike pole vault over expectations that I think are a tad on the conservative side. The latest addition to the Air Max line looks incredibly futuristic. And if it’s as comfortable as it looks, Nike may have the product it needs to get running again.

What Is the Price Target for NKE Stock?

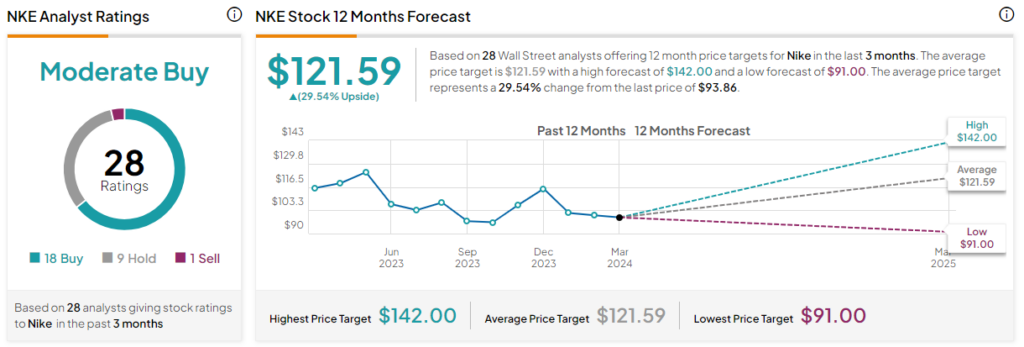

Nike stock is a Moderate Buy, according to analysts, with 18 Buys, nine Holds, and one Sell assigned in the past three months. The average NKE stock price target of $121.59 implies 29.5% upside potential.

Bottom Line

While I still view big-name brands, like Lululemon and Nike, as impressive enough to command higher margins versus most other up-and-coming rivals, I can’t help but wonder if younger generations are more than willing to embrace a new generation of brands.

If I had to choose between the two apparel plays to buy on the dip, I’d have to go with NKE stock. Nike seems more like a timeless brand, with its Jordan sneakers that continue to stand tall through the decades.

Meanwhile, Lululemon may face growth challenges if it can’t continue sprinting at full speed with younger generations (think Gen Z and Gen Alpha). Also, as a much younger brand, we just don’t know how it will evolve as it enters its third decade of existence. Nonetheless, LULU stock is a higher-risk play but one that could also accompany higher rewards.