Lowe’s (LOW) has reported stellar earnings for the second quarter, easily beating consensus expectations on both the top and bottom line.

Specifically Q2 Non-GAAP EPS of $3.75 beat Street expectations by $0.80 while GAAP EPS of $3.74 also beat by $1.06. Revenue of $27.3B sailed past estimates by $3.06B, and was up an impressive 30.1% year-over-year.

Meanwhile comparable sales of 34.2% came in at more than double the consensus of 16.3%, with comparable sales for the U.S. home improvement business rising by 35.1% from 2Q19. That was with sales for Lowes.com exploding by 135% year-over-year.

“We delivered very strong second quarter results, with all merchandising divisions posting comparable sales growth exceeding 20% and all U.S. geographic regions delivering comparable sales growth of at least 30%” commented Marvin R. Ellison, Lowe’s CEO.

He added that sales were driven by a consumer focus on the home, core repair and maintenance activities, and wallet share shift away from other discretionary spending.

Looking ahead, Ellison stated that LOW’s sales momentum continues into August, and the company is investing in the business to further its omnichannel capabilities.

As of July 31, 2020, Lowe’s operated 1,968 home improvement and hardware stores in the United States and Canada.

On May 20, LOW withdrew its financial guidance for fiscal year 2020 citing limited visibility into future business trends during this unprecedented operating environment, which “results in an unusually wide range of potential outcomes for 2020 financial performance.”

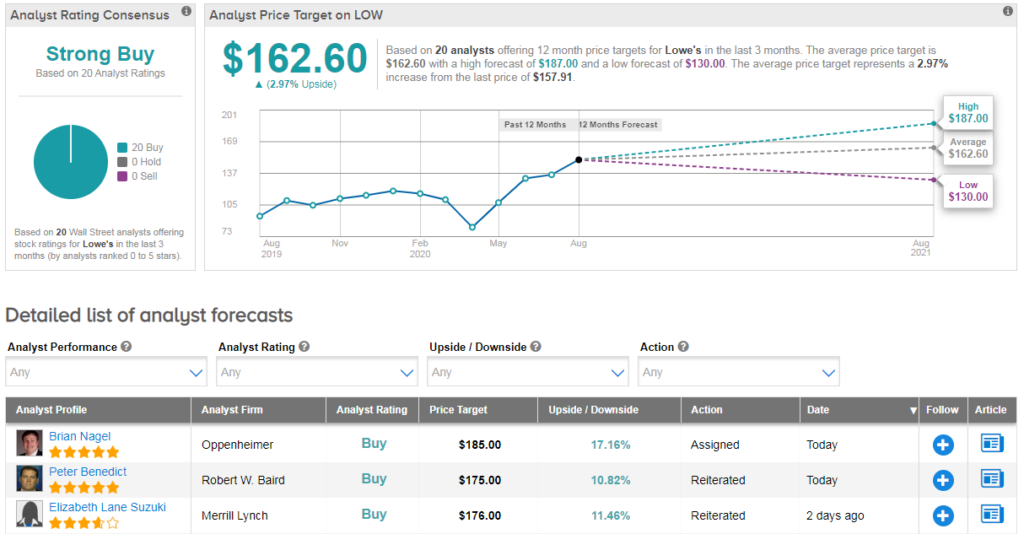

Shares in LOW stock are up 3% in Wednesday’s pre-market trading, and have climbed 32% year-to-date. The stock scores a bullish Strong Buy Street consensus, with no less than 20 back-to-back buy ratings. However, the average analyst price target of $162 indicates limited upside potential from current levels.

Following the earnings report, Wells Fargo’s Zachary Fadem reiterated his LOW buy rating, writing: “In our view, Q2 is one for the record books, and considering the outperformance relative to Home Depot (HD), we’re making the case that valuation should re-rate with LOW’s trading 5x turns below HD and a 9% discount to SPX.”

And while LOW’s outperformance could moderate/reverse in coming quarters as DIY and key category tailwinds wane, Fadem still sees “2H upside from structural-COVID factors, improving sales productivity, e-commerce /Pro initiatives and a new stay-at-home lifestyle that we believe has legs.” (See LOW stock analysis on TipRanks)

Meanwhile Oppenheimer analyst Brian Nagel reiterated his buy rating and $185 price target, writing: “Q2 results at LOW surpassed even the most optimistic forecasts.”

Related News:

Walmart Delivers Earnings Triumph; E-Commerce Sales Double

Home Depot Sales Exceed Estimates As Shoppers Pile On DIY Products

Kohl’s Dips 17% As Covid-19 To Hit Back-to-School Sales